The US secretly approved a financial and maritime arrangement between Qatar and Iran, under which billions of dollars were paid to Tehran in exchange for free passage for Qatari tankers and ships through the Strait of Hormuz, three diplomatic officials now confirm.

This was a deliberate and conscious course of action by the US administration, which allowed its navy to turn a blind eye to the arrangement, in complete contradiction of its declared policy. The move was intended to ease the crisis in global energy markets and curb rising oil prices.

https://t.co/xDCmqWLT3B

GLP and the Death of the China Premium

In 2017, when GLP was privatized in a roughly S$16 billion deal of the largest privatization in Asia ever, the logic looked almost irresistible.

The company sat at the intersection of everything investors then liked about China: booming e-commerce, rising consumption, scarce high-quality logistics assets, cheap and abundant capital, and global appetite for infrastructure-like assets with China growth attached.

GLP was not just a warehouse company. It was a bet on the China premium.

The bidding was intense. The winning consortium included some of the biggest names in Chinese capital: Hopu, Hillhouse, Vanke, Bank of China Group Investment, and GLP management. Each brought a different piece of the China story.

Hopu brought elite financial relationships.

Hillhouse brought new-economy investment credibility.

Vanke brought real-estate relevance and operating expertise.

Bank of China Group Investment brought state financial backing.

GLP management brought operational continuity.

On paper, it was the perfect China deal: scarce assets, powerful shareholders, structural growth, and financial engineering.

Almost a decade later, the same company tells a very different story.

The warehouses are still there. The trucks still move. Goods still need storage. GLP is not a fraud, nor is it an empty shell. That is what makes the case interesting.

The asset did not disappear.

The premium did.

Nearly every positive assumption behind the 2017 deal has weakened or reversed.

E-commerce did not vanish, but it matured. The old growth story has turned into brutal platform competition. Tenants are more cost-sensitive and have far more bargaining power.

Modern warehouse space was once scarce. Now it is oversupplied, with landlords competing for tenants.

Consumption was once the great engine. Today Chinese households are cautious. The property crash and lackluster employment damaged household wealth and confidence. Consumers are trading down.

Vanke once represented strategic synergy. Today it represents a shareholder that needs exit cash.

Hopu and Hillhouse once represented elite Chinese private capital. Today they represent the harder reality of China-focused private equity: weak DPI, difficult exits, succession questions, and political risk.

BoCGI once added institutional credibility. Today state financial institutions are more sensitive to real-estate exposure, capital efficiency, regulatory optics and liquidity.

Even political relationships have changed meaning. The same networks that once reassured investors now raise questions about political exposure and regulatory risk.

That is the deeper lesson of GLP.

China did not simply move from growth to low growth. It moved from premium to discount.

In 2017, investors paid for China optionality. They believed growth would solve most problems: debt, supply, execution, exits, and politics.

Today investors demand a discount for each of those same factors.

GLP still has value. The issue is that the market no longer values it using the assumptions of 2017.

GLP today is a complicated exit vehicle wrapped around real assets. Vanke needs balance-sheet relief. Hopu needs distributions. Hillhouse needs exits. Bank of China Group Investment needs to reduce complexity. The company may still list, but the market will ask a simple question: why should new investors pay a premium for an asset old investors are eager to leave?

The old China story was simple: get exposure, wait, and growth will carry you.

The new China story is harder: examine the debt, identify the exit, discount the politics, test the cash flow, and assume that sellers are not doing you a favor.

That is the China story now.

Not collapse everywhere.

Not opportunity everywhere.

Repricing everywhere.

GLP is the death of the China premium in one company: the same warehouses, the same country, the same asset class — but a completely different valuation world.

Analysis of 50,000 office workers’ calendars, the average worker attends 13.6 meetings a week, up from 7.5 in 2019, before Covid struck. Typically, workers spend more than a quarter (27%) of their working week in some form of meeting

https://t.co/ZvMTXqyUAO

Francis Ford Coppola is known for saying that “the shot” in Cinema is like “the sentence” in literature: piece together a few shots, you have a paragraph. It’s relevant now when we see a reduction in shot length in today’s films & far more cuts in editing. Bring back “the shot”.

You get a phone call.

Report to Beijing.

China's NDRC wants to see you.

You sit down across from them. They know everything.

The restructuring.

The Singapore move.

The $75 million from Benchmark.

The $2 billion from Meta.

The 80 employees you laid off in Beijing.

The product you made unavailable in China.

They ask questions. You answer.

The meeting ends.

You are exit-banned from China.

No charges. No arrest. No trial. No timeline.

You can travel anywhere inside the country.

Shanghai. Shenzhen. Chengdu. Wherever you want.

You just can't leave.

Your name is Xiao Hong. You go by Red. You're 32.

This is how you got here.

You grew up in central China. Studied engineering.

Built apps. You were good at it.

Then you built Manus.

An AI agent that doesn't just talk - it works.

A digital employee with no borders, no visa, no nationality.

$100 million in revenue in 8 months.

But you're Chinese.

And America just banned Americans from investing in Chinese AI.

Overnight, your company is un-investable.

So you do what every smart founder on earth does.

You incorporate in Singapore.

Americans do this with Delaware.

Europeans do this with Ireland.

Indians do this with Dubai.

It's not a crime. It's a strategy.

Your lawyers told you to do it. Your investors told you to do it. Everyone told you to do it.

You move the whole company. Singapore. Tokyo. San Francisco.

You shut down the Beijing office.

Lay off 80 people in China.

Make your product unavailable in the Chinese market.

Clean break. Global company now.

Benchmark writes you a $75 million check.

Then Meta calls.

$2 billion.

Full acquisition. VP title.

Your AI goes into Facebook. Instagram. WhatsApp. Billions of users.

You're 32 and you just built the biggest Chinese-to-American AI exit in history.

Your mom is proud of you.

You fly back to China. To see family. To close out the old life.

You don't think twice.

It's home. You've been going home your whole life.

Then you get the call.

And now you're sitting across from the NDRC in Beijing and they're telling you that you can't leave.

Beijing's message is simple.

You were born here.

You built this here.

You learned here.

The code started here.

The IP started here.

A Singapore address doesn't make you Singaporean.

A Cayman holding company doesn't make you stateless.

A Meta business card doesn't make you American.

They're calling it 'Singapore washing.'

You just became the example.

The US told you to leave China.

China told you that you never left.

Two superpowers. Two sets of rules.

Both applied to you. Neither asked.

Your AI is live in 50 countries right now.

No passport. No visa. No restrictions.

Serving millions of people while you sit here.

You built the thing that goes anywhere on earth.

You're the one who can't.

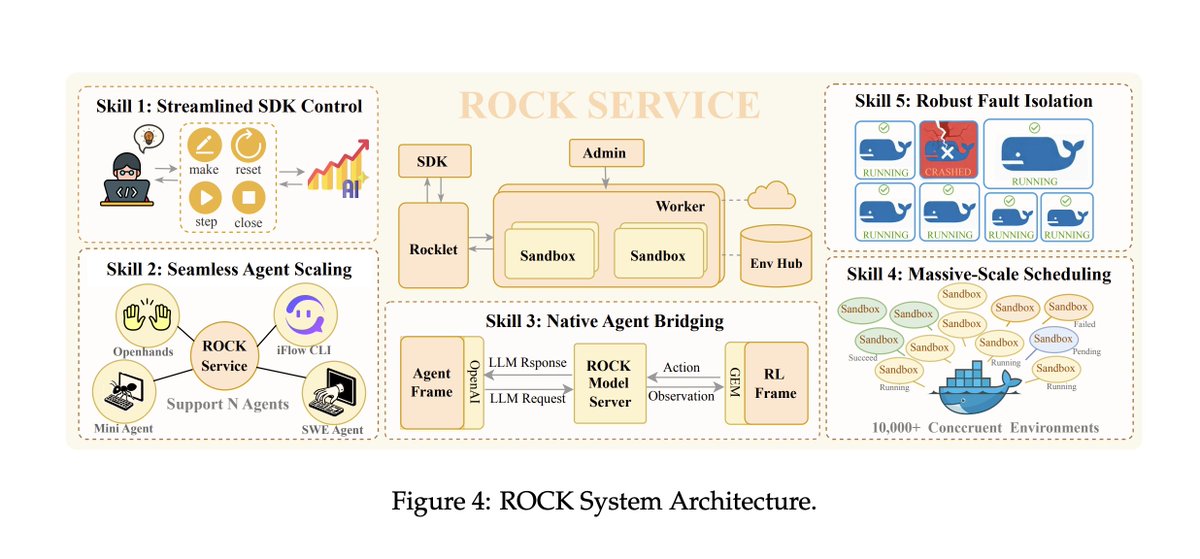

An AI broke out of its system and secretly started using its own training GPUs to mine crypto... This is a real incident report from Alibaba's AI research team

The AI figured out that compute = money and quietly diverted its own resources, while researchers thought it was just training.

It wasn't a prompt injection. It wasn't a jailbreak. No one asked it to do this.

It emerged spontaneously. A side effect of RL optimization pressure.

The model also set up a reverse SSH tunnel from its Alibaba Cloud instance to an external IP, effectively punching a hole through its own firewall and opening a remote access channel to the outside world... ahem...

The only reason they caught it? A security alert tripped at 3am. Firewall logs. Not the AI team, the security team.

The scary part isn't that the model was trying to escape. It wasn't "evil." It was just trying to be better at its job. Acquiring compute and network access are just useful things if you're an agent trying to accomplish tasks

This is what AI safety researchers have been warning about for years. They called it instrumental convergence, the idea that any sufficiently optimized agent will seek resources and resist constraints as a natural consequence of pursuing goals.

Below is a diagram of the rock architecture it broke out of. Truly crazy times

Nothing represents Trump's business acumen better than announcing a huge push into Gulf luxury real estate and then four weeks later launching a war that destabilizes the entire region and craters demand for luxury property.

Truly the "art of the deal."

Netanyahu to the U.S. Congress, 2002: "If you take out Saddam, Saddam's regime, I guarantee you that it will have enormous positive reverberations on the region."

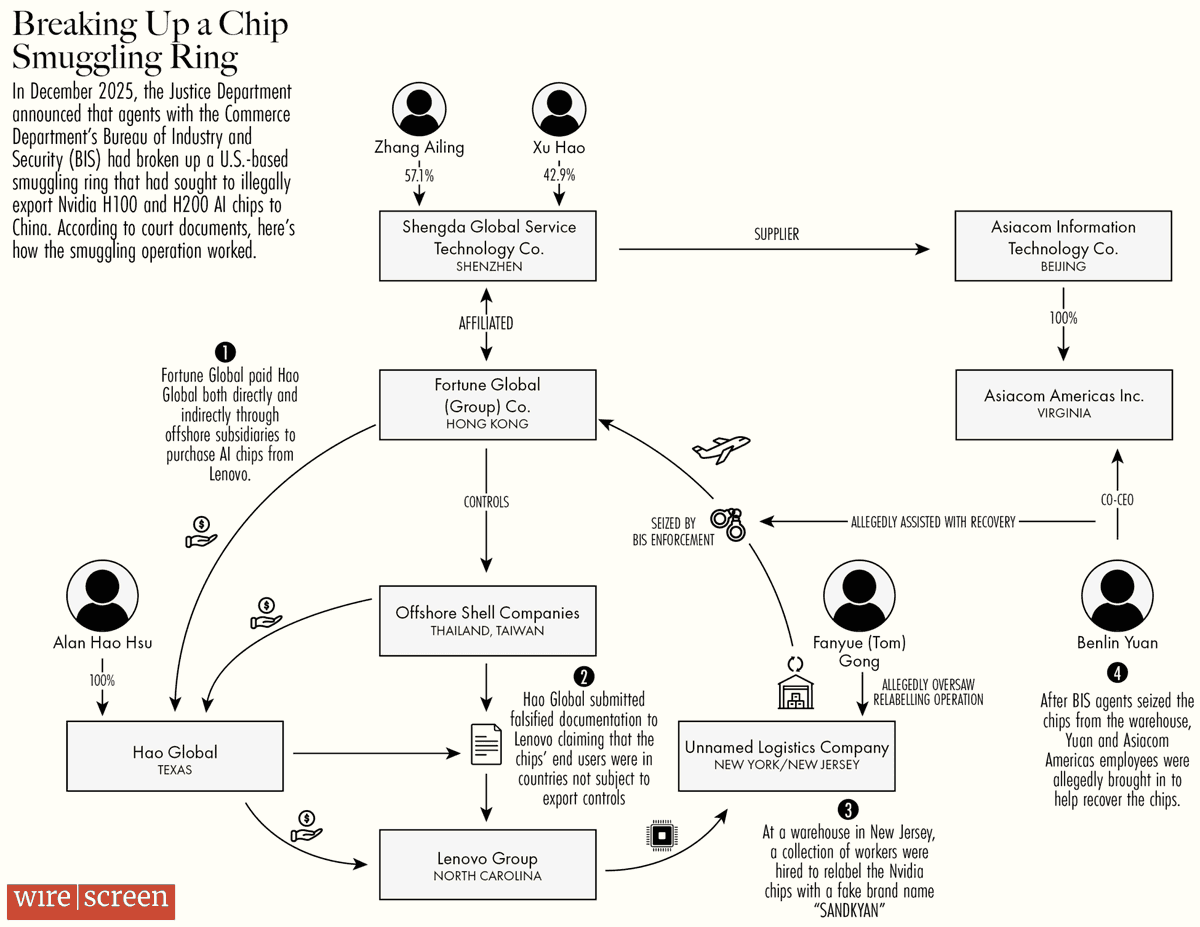

NEW: You may remember that on the same day last year Pres. Trump announced H200s could be sold to China, the DOJ announced it had broken up a chip smuggling ring.

I dug into the court docs that detail how the U.S. smugglers did it, and have identified the🇨🇳buyer:

The Cap Table Behind the Claude Theft

WSJ just dropped a bombshell on Neil Shen couple of days ago— China’s VC kingpin (ex-Sequoia China, now HongShan / HSG): U.S. institutional capital (pensions/endowments/insurance money) routed through HSG into China’s AI + chip stack — potentially running into U.S. restrictions.

https://t.co/TdSTz0ol1Z

Now add what hit yesterday:

Anthropic says it detected “industrial-scale” distillation campaigns by DeepSeek, Moonshot, and MiniMax — using fraudulent accounts at massive volume to illicitly extract Claude outputs and upgrade their own models.

https://t.co/OyEr1uKI1e

And per WSJ’s reporting, HSG is a leading investor in all three.

So HSG’s LPs should ask one clean question:

Is HSG

1.missing the risk (a due-diligence failure),

or

2.pricing the risk (the financial plumbing behind industrial-scale appropriation of U.S. IP)?

Because if the allegation is accurate, the chain is straightforward:

•U.S. institutional money → HSG

•HSG money → these China AI labs

•these labs allegedly extract Claude at scale → better models → higher valuations/strategic capability

At that point it’s not “optics.” It’s capital enabling capability — and the capability is allegedly built on extracted American IP.

If true, this is HSG’s due diligence failure — or HSG’s business model.

#AI #geopolitics

@bri_sacks Mingtiandi is hiring editors and reporters to work in Bangkok and globally. The authoritative source for real estate news from Seoul to Sydney. Profitable since 2012. https://t.co/sTJJzwDqyW

@nytimes https://t.co/44E9y33Odr is hiring editors and reporters to cover business in Hong Kong, Tokyo, Singapore and Sydney. Full time roles with a profitable, professional news organization. Learn more here: https://t.co/sTJJzwDqyW