Quant modeled winning Polymarket strategy using Theta Decay.

Easier than you could imagine.

I asked moltbot to analyze odds volatility as the resolution approaches.

his answer mirrors options structure:

> 30 days before resolution: 2-4% price swing

> 7 days before resolution: 0.5-1% price swing

> 1 day before resolution: prices barely move unless major surprise

Volatility decays as resolution approaches. that's ideal simulated market sentiment flow.

Each period has it's own price-move pattern and preferred direction:

30+ days is the period of price trend. information accumulates in preferred direction. impulse is set, follow it.

~7 days is the period of reverse to mean prices. most info is known. sometimes prices estimated at >90c making you possible to jump in before potential retail overreacting due to noise/rumors.

Professional traders switch strategies as resolution decays, you can check it yourself.

Will be fair to say:

Period gaps may vary, depend on time left when market is only launched, liquidity, retail traction, side noises such as "potential insider".

The information here is an average value based on the analyzed markets. consider it as taken from a perfectly modeled market.

more in the thread ↓

Paper "Nonlinear Time Series Momentum" documents "a persistent nonlinear relationship between price trends and risk-adjusted returns across markets and asset classes that is consistent with asset pricing theory." https://t.co/CkBg3YxLuN

1. Ridge regression is heavily used in systematic investing both in the p << n and in the p >> n cases (last one, less so). I don't think that the use is very deeply motivated, other than the old standard argument in favor (see, e.g., El. Stat. Learning).

This Stanford paper pokes a hole in one of finance’s favorite excuses: “the data is too noisy.”

For decades, quants have argued that raw prices are useless without handcrafted indicators layered on top. This paper asks a cleaner question. What if the signal is already there, and we’ve just been looking at it the wrong way?

The author builds a model that predicts bullish versus bearish moves for S&P 500 stocks using nothing but raw price data. No indicators. No factor libraries. Just daily OHLCV plus adjusted prices that explicitly reflect dividends and splits.

The trick isn’t more data. It’s representation.

Instead of treating time series as sequences, the paper treats rolling price windows as spatial objects. Each window becomes a structured matrix, closer to an image than a chart. That lets convolutional filters detect local patterns like momentum shifts, volatility clustering, and structural breaks from corporate actions.

This borrows intuition from computer vision, not classical econometrics.

The dataset spans up to twenty years per stock with institutional-grade pricing. Ten channels feed the model, and sliding windows create dense training samples without synthetic tricks. Normalization keeps everything scale-invariant across features.

Architecturally, it’s a deep 1D CNN. Early layers focus on short-term structure. Deeper layers pick up longer trends. Compared to recurrent models, the CNN handles volatility spikes and event-driven jumps with more stability.

The task is simple but strict: predict direction, not returns, across horizons from a few days to a month. Training is tuned carefully, and convergence looks clean rather than suspicious.

The results are what make people uncomfortable.

Several large-cap stocks hit validation accuracies in the high 80s and low 90s. JP Morgan reaches around 91 percent on longer horizons. The curves suggest real learning, not a quick overfit.

The author stays cautious. This doesn’t model costs, execution, or slippage. But it does show something important. Deep models can internalize market mechanics directly from raw price tensors, including distortions most pipelines smooth away.

The larger implication cuts deep.

Feature engineering may matter less than how you frame the data. By choosing the right inductive bias, the model learns structure humans usually try to hardcode.

Treating financial time series like image-like objects isn’t a gimmick. It’s a serious alternative to decades of handcrafted assumptions, and it challenges the idea that markets are unreadable without heavy human intervention.

Read the full paper: https://t.co/VcFfAPhjAf

tired on the ai-generated, undergraduate-level kwant textbook slop on your timeline?

you fkin should be

read these @macrocephalopod threads instead

they are written by someone who actually does the thing.

and knows, from experience, what matters and what is circlejerkery.

Statistical Arbitrage

After many hours of debugging, this week, we resumed sharing studies

This is the first article on a statistical arbitrage idea I've been working on over the past weeks. It looks promising.

Paper: "Systematically identifying clusters of similar assets is a critical step in statistical arbitrage strategies... Profitability is influenced more by the selection of feature sets and clustering methods than by the choice of signals." https://t.co/vsVnwtC0F6

Classic example of lying with statistics.

The reason this chart looks this way is that these are overlapping monthly observations. I won't go into too much statistics/econometrics, but it suffices to say that there is indeed a negative relationship but the relationship is not nearly as strong as the chart suggests and most people won't understand that.

10 year horizon observations plotted at overlapping monthly frequency mechanically creates what's called "serial correlation" and overstates the significance of the relationship. Properly accounting for this serial correlation in the standard errors, the relationship has a R^2 about ~10%.

The simplest way to think about it is like snapping pictures of a horse race at minute or even snap shots. Not matter how many shots one takes, one horse race is still just one horse race. Between 1988 to 2024, there only been fewer than four non-overlapping 10 years!

As with most macro stuff, such as a prediction of future long term returns using valuation, there's just not that much data. What happens isn't the small wiggles of the time series but the big turning points and events, of which we don't have that many observations. And snapping multiple pictures of the same event from multiple angles doesn't really help.

And that is why the argument in the quote tweet isn't nearly as smart as it sounds. There's a weakly negative relationship between valuation and future returns, but investing more or less in stocks based on valuation hasn't been a good idea at all.

https://t.co/p7fGO7Iztl

Revenge of the Silent Male Voter

What I learned about Trump's landslide victory from one night in New York City.

On election day, I caught the subway from Brooklyn to Manhattan. Sitting across from me an elderly woman wore a t-shirt with the image of Trump pumping his fist in the air with the words “fight, fight.” A small "I Voted" sticker was pressed onto her lapel.

She sat with an easy confidence. There were no disapproving glances from other passengers. There was no tension. No conflict. It struck me that in 2024 it was now perfectly acceptable to express support for Trump in a deep blue (Democratically held) city. As I travelled to my destination I wondered: if one could support Trump this openly in New York City, what might support look like in the rest of the country?

A few hours later I attended an exclusive well-heeled party. I spoke to various professionals who said that they had never voted Republican in their lives, but had voted for Trump that day due to his support—in their words—“for the Jews”. These Manhattanites told me that Kamala was too sympathetic to the “pro-Hamas contingent” of the far-Left, and at a time of rising antisemitism, they couldn’t bring themselves to support her. This small group of cosmopolitans represented a contingent far-removed from the stereotypical MAGA voter. And yet listening to their views, it again occurred to me: if I could find such support for Trump in the middle of a Democratic heartland—what might it look like in the rest of the country?

When I arrived at my final stop of the evening—a private underground bar in the Lower East side of the city—a celebratory atmosphere had begun to explode. The betting markets tipped a Trump win, and online supporters of Harris started to express acceptance of defeat. The beer here had already run dry. It was so bustling that it was hard to move, with young men in their twenties and early thirties outnumbering women by 2:1. These men were diverse: white, black, Hispanic, Asian. A few wore Trump caps, but the aesthetic was more like a university dorm than a MAGA rally. “This is the counter-culture” one party goer told me. "This isn't just about Trump," another said. "It's about Vance and Musk. It's about American dynamism."

In the coming days, much will be written about working class concerns—issues that have become familiar focal points for those seeking to understand Trump’s support. But while inflation and border policies will have no doubt played a role in the Republicans’ landslide victory, we might also want to look at the sentiments expressed by young male voters—voters who represent a new and emerging contingent in American politics. Nothing about the young men I spoke to appeared particularly conservative or “right-wing”. Yet it was easy for them to explain why they voted for Trump. And if we zoom out and look at broader cultural trends, it should be easy for us to understand too.

If we take a macro perspective, we see that such young men have never known a culture in which males are not routinely described as “problematic,” “toxic,” or “oppressive”. Going to university, and working at modern companies, they live in a world of Diversity Equity and Inclusion policies—many of which promote an insidious and pervasive form of anti-male discrimination. Yet to talk about it in public invites social ostracism. To criticise DEI is to risk being called a Nazi.

These young male voters know about theories of patriarchy and white supremacy, but they have never known a culture which celebrates the Great Man Theory of history. Thomas Carlyle’s nineteenth century framework for understanding the past is seen as an anachronism, not worthy of serious thought. Today we acknowledge historical figures not for their feats, but for their crimes. Whether it is due to slavery, colonisation, racism, or sexism, we tear down the monuments of our past, while building no new heroes for our future.

The problem with this way of viewing the world is that it is alienating and self-defeating. It is also wrong. By any objective standards Elon Musk is a great man of history, who is influencing the course of human civilisation for generations to come. As one party-goer told me “he caught a fucking rocket with mechanical chopsticks.” Yet despite his achievements, Musk is more likely to be scorned than celebrated by the Democratic establishment.

This tension between achievement and resentment explains much about our current moment. The young men I met that night in Manhattan weren't just voting for policies. They were voting for a different view of history and human nature. In their world, individual greatness matters. Male ambition serves a purpose. Risk-taking and defiance create progress.

This is why the Trump victory transcends conventional political analysis. It represents more than a rebuke of border policies or inflation rates. It signals a resurrection of old truths: that civilisation advances through the actions of remarkable individuals, that male traits can build rather than destroy, and that greatness—despite our modern discomfort with the concept—remains a force in human affairs.

The elderly woman on the subway, the Manhattan professionals, and the young men at the underground bar all sensed a shift. They saw in Trump not just a candidate, but a challenge to a psychosocial orthodoxy that has dominated American institutions for a generation. Their votes marked not just a political preference, but a cultural correction.

As the final results came in that night, it became clear that what I witnessed in New York was playing out across the nation. The election wasn't just a victory for Trump. It was a victory for a way of seeing the world that many thought dead: one where individual achievement matters, where male ambition serves a purpose, and where great men still shape the course of history.

Read the full article here-->

https://t.co/rSoptfam9o

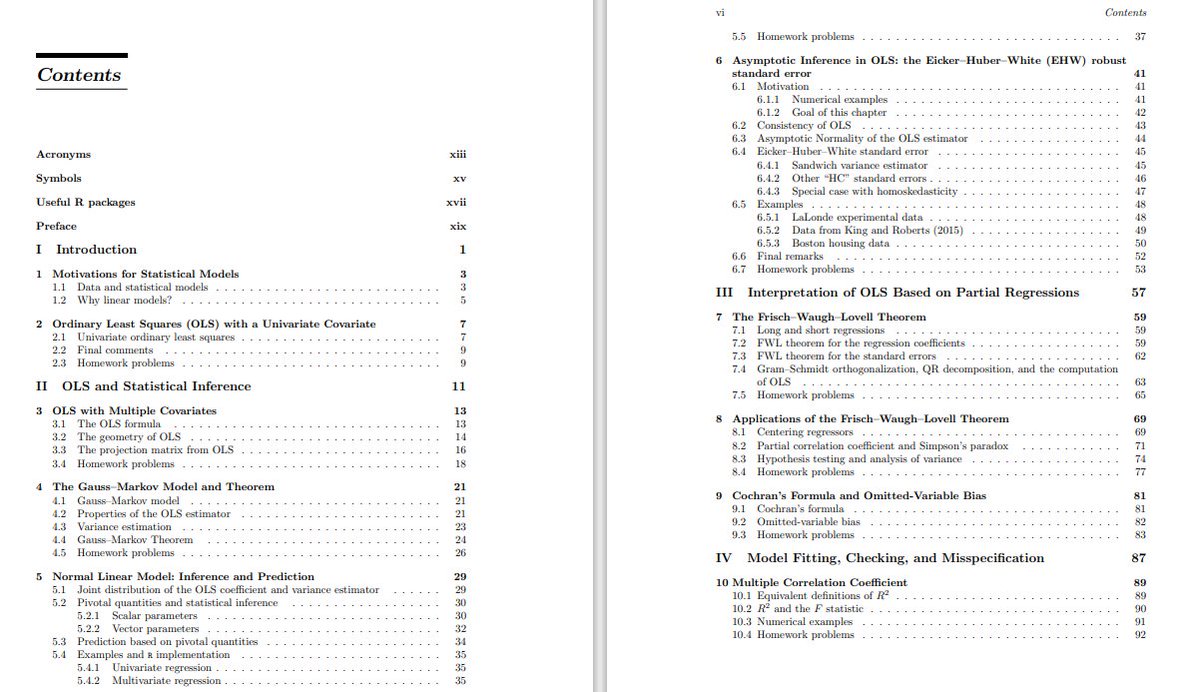

These lecture notes on "Linear models and extensions" by Peng Ding at Berkeley are great.

400 pages(!) on OLS, Ridge, Lasso, WLS, Logistic regressions, Quantile regressions, and much more.

Link: https://t.co/2aNhBTes80

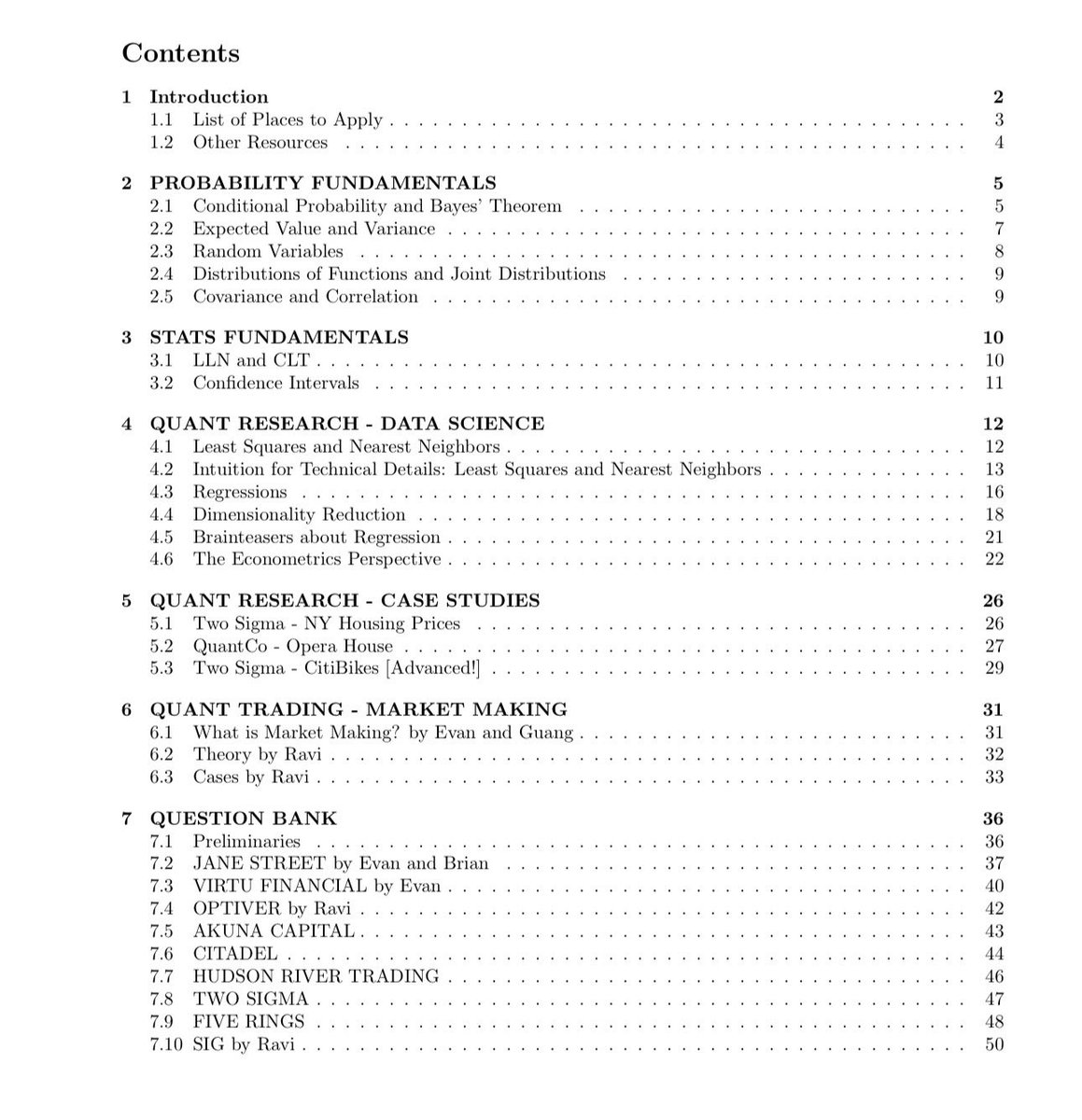

A very good introduction to the field. If you're getting started in quant, this book should be at the top of your list. It's also incredible interview prep for getting familiar with the industry.

Flirting is a way of life. Do you smile at the pretty girls, compliment the older ladies, or wink at the moon? How about the birds, when they sing, do you whistle back in tune?

Or what about when driving, do you have a smooth touch & no fear of pushing your car to its limits? In business, do you dare to demand what you want? Are you bold with your plans? Does risk excite your spirit?

In conversation, do you say what you mean & speak with your chest? Do you deliver the risky joke without qualms who will take offense?

Do you stroll with your head held high - do your steps feel weightless? When you stand, are you relaxed or are you tense?

Do you treat strangers like you’re reacquainting with an old friend? Do you ever dare to divulge your well kept secrets? Are you present, there in the moment, or are you living in your head?

Do you breathe romance into everything you do, see the beauty in the mundane, & leave a trail of unrelenting positivity wherever you venture? You see, flirting isn’t just what you do to have someone fall for you - it’s what a healthy spirit does when they’re in love with life, & I will continue flirting into the afterlife

This is a recent book chapter by Hoffman on Kalman filtering and pairs trading, including extensions such as partial co-integration and the potential use of reinforcement learning.

Link (open access): https://t.co/hwWCvpxDQf

New paper on backtesting by Joubert et al. The paper reviews "... three main types of backtests, namely the walk-forward, resampling, and Monte Carlo methods..."

Link: https://t.co/PBwU99ORKu