SaaS Multiples: Who Deserves the Premium?

SaaS companies* are usually valued on Forward EV/Sales vs. NTM revenue growth, but growth alone does not explain the full picture. Operating margin matters because the market usually rewards companies that combine high growth with a visible path to profitability.

In this chart, I removed $PLTR Palantir, which remains a major outlier with 35.3x Forward EV/Sales and +63.5% estimated NTM revenue growth.

The fastest growers in the group include $APP AppLovin, $ORCL Oracle, $AXON Axon, $DOCN DigitalOcean, $FIG Figma, $ZETA Zeta, $NET Cloudflare, $SNOW Snowflake, $PANW Palo Alto Networks, $TOST Toast, $DDOG Datadog, $FICO Fair Isaac, $CRWD CrowdStrike, and $IOT Samsara.

Companies with positive GAAP operating margins deserve a different valuation framework than companies still operating at a loss. A high-growth company with weak margins may still trade at a premium, but the market usually becomes less forgiving when growth slows.

*-SaaS/software companies with majority subscription revenue, EV above $1B, and gross margin above 70%.

One of the biggest requests I’ve gotten is for more short-form video content so nearly two months ago we relaunched the Futurum Equities YouTube channel.

So far, we’ve covered:

• Why $MELI is one of the best opportunities in market

• How $TE, $NVTS & $IREN fit into AI power bottleneck

• Why Jensen Huang thinks $MRVL can 5x to a $1T valuation

• Everything you need to know about $SPCX IPO & $60B Cursor deal

• Why $ONDS, $KTOS, $MRCY & $AVAV are my 4 favorite drone stocks

• Why I initiated trades in $NFLX & $MSFT at near decade-low valuations

• Earnings reactions for $MU, $PLTR, $DOCN, $AMD, $ARM, $TMDX, $ASTS, $HIMS, $NBIS, $EOSE, $ONDS, $ZETA, $SNOW, $AVGO, $ORCL, $ADBE & $NVDA

We plan to keep posting 4 to 5 videos per week so let us know which companies or topics you want us to cover next!

Tesla just posted its BEST quarter ever. 480,126 deliveries, beating Wall St by ~74,000 cars.

The stock crashed 7.49%. 📉

~$120B wiped out in a single day. Here's why a blowout got punished 👇

$TSLA $SPY $SPX $IWM $QQQ

$NVDA just introduced a new model that “opens up compute access” to startups, enterprises, researchers and regional AI players.

Instead of only selling hardware upfront, Nvidia can now earn a recurring, usage-linked cut of AI cloud revenue.

Sharon AI is deploying up to 40K GB300 GPUs while Firmus is building a 360MW Indonesia AI factory that could scale to 170K Nvidia GPUs.

AI demand remains strong, but semis are starting to price cycle risk

Semiconductor and memory stocks corrected after a record rally, as investors started questioning whether AI capex momentum can keep accelerating.

Pullback: $QCOM -30%, Kioxia -29%, $ARM -25%, $AVGO -25%, $WDC -25%, SK Hynix -25%, $STX -20%, Samsung -20%, $MU -18%, $MRVL -18%, $NVDA -16%, and $SNDK -14% from 52-week highs.

The AI cycle is still powerful. Hyperscalers continue spending heavily on GPUs, HBM, storage, networking, and data center infrastructure.

But semiconductor markets historically turn when capex momentum slows, even if end demand remains strong.

Is this profit-taking or the first sign of a peak in the memory and AI hardware supercycle.

Main pressure points: A new U.S. class-action lawsuit alleges Micron, Samsung, and SK Hynix restricted conventional DRAM output while shifting capacity toward higher-margin HBM, contributing to a sharp increase in memory prices.

OpenAI’s IPO delay also hurt sentiment because investors treat OpenAI as a key signal for AI monetization and infrastructure returns.

Pricing concerns: Google’s TurboQuant raised questions about future memory intensity if compression can reduce RAM needs for AI vector operations.

Broadcom’s more cautious AI forecast added pressure to a crowded trade. Rising memory costs are also flowing into consumer products, with price increases from Apple and Microsoft raising the risk that chip pricing power eventually hurts demand.

Still, bull case has not disappeared: $NVDA continues to guide strongly, $AVGO has major AI semiconductor growth, $MU has HBM fully booked through 2027, SK Hynix remains an HBM leader, and $STX / $WDC benefit from AI data storage demand.

AI infrastructure demand is real, but investors are now testing durability, and next phase will depend less on narrative and more on capex discipline, margins, inventory, customer concentration, and whether AI spending turns into strong returns.

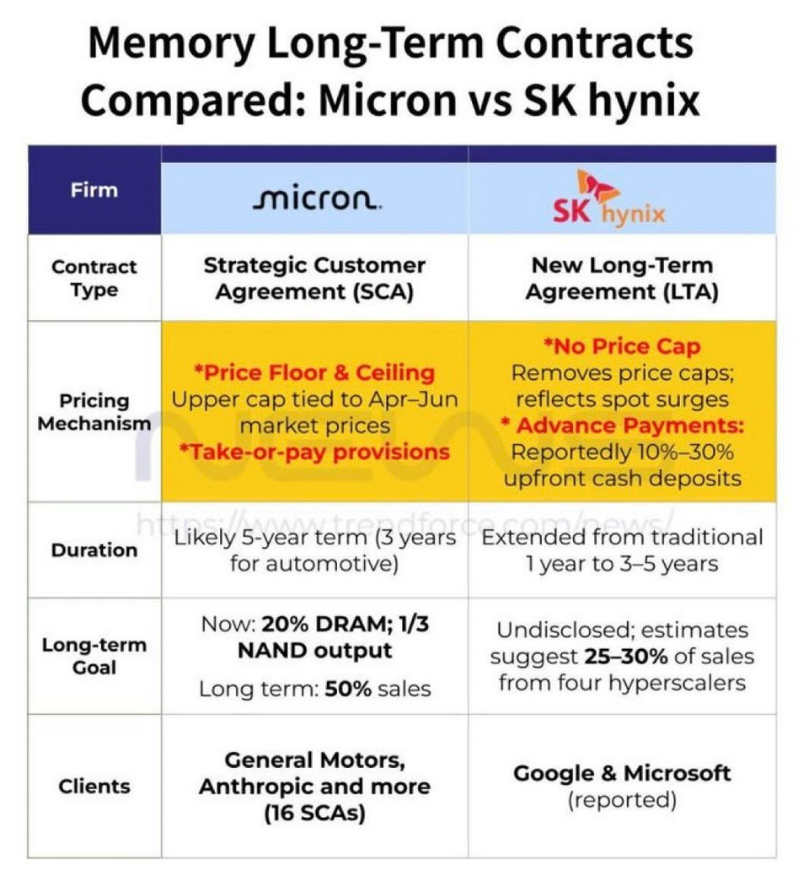

SK hynix is removing price caps from some memory supply deals by letting contract prices fully reflect spot market spikes during shortages.

Memory LTAs are also moving from 1 year terms to 3 to 5 years while $MU model still includes price floors, price ceilings and binding volume commitments.

So... are we still compute constrained? If Meta has excess compute... SpaceX has excess compute to sell...and the neoclouds are selling off on this news...

What exactly is scarce?

$RKLB up over 12% after acquiring $IRDM in an ~$8B deal to become a fully integrated space power delivering critical communications to millions of users worldwide.