Levy is technically already a big rent-regulated MF player in NYC via his relationship with Tanenbaum / Denali. This would be a major expansion, but given his comfort with saddling up with Tanenbaum - given his status as one of the "worst" NYC landlords - it would appear Levy knows exactly what he is getting himself into. Via @AtriumDataAI.

My team and I launched Atrium Data this week, our credit intelligence platform 🚀

We track every loan made in the US and link it to the lender of record, with a special focus on US banks. Please follow @bankingembedded and give our Bank OZK + life science report a read:

This week we published our first research report: The Life Science Reckoning through the lens of Bank OZK. Link in bio.

Here are the key takeaways:

- As a category, life science lab space was untouchable in 2021, most market were completely full and demand was through the roof

- Developers in San Diego, Boston and San Francisco had no problem raising $10b+ for spec lab spaces

- Lenders like Bank OZK took on a meaningful portion these projects, this report covers ~$2.8b of OZK loans

- In 2025 most of those projects have delivered, and many sit completely empty

- We focus on Bank OZK because they make large balance sheet loans, and are unusually transparent in their reporting, releasing property by property appraisal information

- The report goes through 10 emblematic life science loans and evaluates how they are performing, and how they are valued, as a lens to study life science development generally

The methodology is simple. We take a "napkin math" appraisal methodology, with key inputs of sub-market rents, occupancy and cap-rates, and build up as-stabilized and as-market valuations, to show how values have cratered independent of the performance and leasing results of each project. We then estimate what the buildings are likely worth today as life science lab space, and as office - which many of the projects will likely pivot to over time. Finally, we take the perspective of a lender and estimate how they would likely risk grade that loan (1-9 grades from Pass to Loss) using standard methodologies favored by regulators (FDIC, OCC).

Here are a couple notable properties and how they score:

1. IQHQ's Radd - $915m - Risk Grade 5: Criticized Special Mention. As Bank OZK's largest individual credit, this project is tracked closely by analysts. It has signed a couple of retail and small lab leases, but sits mostly vacant in a sub-market that is not a traditional life science cluster. Since origination in August of 2022, market rents are down ~15%, market occupancy is down ~25% and market cap rates are up 175bps - a combination that means the market value of the property has fallen from $1,384/ft at origination to $623/ft today. Despite the >50% value collapse the bank still has a cushion, with LTV sitting at 86% of committed capital and much lower if you isolate the drawn capital. The loan just entered its first extension year and so still has a bit of time to show lease-up momentum. While unlikely to be achieved in that time window, the stabilized value is still nearly $1b. An office conversion in San Diego's decimated downtown office market is also fraught with issues. Flipping to gross rents that would average closer to $50-55/ft means the stabilized value as office is closer to $321/ft, which would put Bank OZK underwater. In the report we go deep on this loan and its sponsor IQHQ. It's worth a read.

2. 1229 W. Concord - $125m - Risk Grade 6: Substandard - Accrual. While a smaller life science credit, this project is in the news now as it was just elevated to substandard-accrual by Bank OZK in their Q3 management comments. The property sits completely empty in a sub-market that is not a life science cluster, and sits adjacent to the failing Lincoln Yards development and shares the same sponsor - Sterling Bay. This loan originated on September 14, 2021 and thus would have entered its final extension year a few weeks back. However, the lack of leasing activity clearly forced Sterling Bay's hand, and the property is now marketed for sale by Eastdil and Savills. The bank has an as-is appraisal showing the value at $74m, and holds the loan on their books just shy of $60m. While that is a reasonable mark if the building is bought as a life science lab, if it is purchased as an office building we think the value could be ~$45m. So while a smaller credit, you can see how the bank - having already taken a $5.1m write-off - could end up with a much larger hole if leasing doesn't improve.

In the report we go deeper on RaDD and 1229 W. Concord and also cover Aperture Del Mar, Pacific Center, Bioterra, Southline, 808 Windsor, Portal 405, Chapter Building II and 777 Industrial. A total of $2.8b of loans, and very minimal leasing across the book.

Betting against George Gleason has been unprofitable historically, and there is no doubt that Bank OZK has no sneaky credit issues - no bank we've covered tracks their loans as closely as OZK. But the life science workouts will be messy over the next 2 years. But, for investors and analysts, the migrations don't need to be a surprise. Using our methodology and our county and property level analytics, we can see and predict which credits are at risk and understand how those credits will hit balance sheets and earnings in advance. Follow the link in our bio to learn more.

the boltons of red bay alabama are sincere, hardworking people fighting for their town and all community banks and they will always have a friend in john maxfield

@BradMBolton 🤝 @MaxfieldOnBanks

@Mr_Neutral_Man When you evaluate REITs do you do any bottoms up - position by position- holdings analysis? Also, are you mostly looking at equity REITs, or do you invest in mortgage REITs as well?

@kevinweil Hey Kevin, two things that would really help us:

1/ ability to spin up docker containers inside the codex environment so we can run tests inside the codex env

2/ have codex read comments on PRs and make corrections

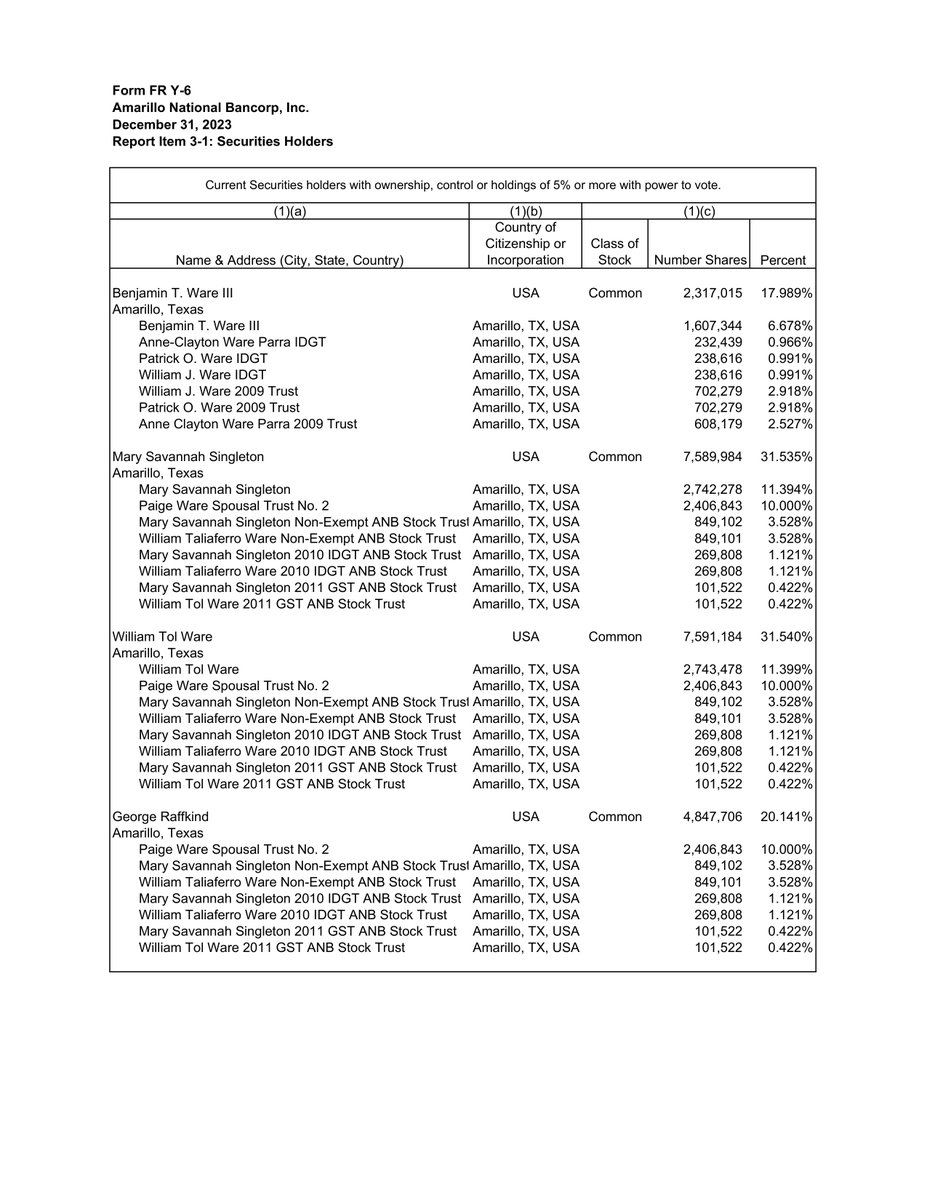

Was asked today about banks in Amarillo, Texas, and it reminded me of an interesting tidbit about Amarillo National Bank...

Namely, Wikipedia claims that Amarillo National Bank ($9 billion in assets) is the largest bank in the United States that is 100% family-owned. It was founded in 1892 by a cattleman and early Amarillo settlor named B.T. Ware, whose family has maintained complete control over it.

Texas Monthly named the Ware family “Bankers of the Century” in 1999. American Banker named its chairman, Richard Ware, its “Banker of the Year” in 2017. Today, it's managed by the fifth generation of Wares, with Richard’s sons at the helm. Amarillo National Banks Vice Chairman Patrick Ware and President William Ware are the great-great-grandsons of B.T. Ware.

(For those curious about how one would go about confirming a bank's ownership structure, you would look at Amarillo National Bank's FR Y-6, which is a form filed with the Federal Reserve Banks that details the ownership structure of bank holding companies. You have to use FOIA to get these forms from some districts, but my good friend @ryanalfred, has collected them from all but one Fed district (and we're getting the last one) in order to map the ownership data of the entire American banking industry. It's sick.)

Another deeply researched piece from @MichaelRoddan . . . and perhaps the very first @bankingembedded reference in @theinformation 🚀:

https://t.co/vigp91qDrp