Fed Decides June 17th:

• Voted 12-0 to hold rates at 3.50%-3.75%

• Economy expanding at a solid pace despite Middle East uncertainty

• Productivity and investment remain strong

• Labor market steady

• Inflation still above 2%

• Fed remains committed to price stability

Gold climbed back to $4,170/oz, gaining 2% for the week after weak U.S. jobs data cut Sept Fed hike odds from 66% to ~45%

=> A softer dollar & steady central bank buying continue to support the bullish case

https://t.co/em76e3E8Zy

#XAUUSD#Gold#Copper#Oil#Silver

Gold climbed back to $4,170/oz, gaining 2% for the week after weak U.S. jobs data cut Sept Fed hike odds from 66% to ~45%

=> A softer dollar & steady central bank buying continue to support the bullish case

https://t.co/em76e3E8Zy

#XAUUSD#Gold#Copper#Oil#Silver

Fed Decides June 17th:

• Voted 12-0 to hold rates at 3.50%-3.75%

• Economy expanding at a solid pace despite Middle East uncertainty

• Productivity and investment remain strong

• Labor market steady

• Inflation still above 2%

• Fed remains committed to price stability

The New York Fed left its U.S. growth outlook largely unchanged, with its Q2 2026 GDP Nowcast at 2.7% and Q3 at 2.4%

=> Stronger unemployment data and model revisions offset weaker payrolls and ADP figures, leaving the overall growth outlook broadly intact

#Fed#FOMC#Powell

Explore the latest GDP insights! Featuring updated data from the BLE, Atlanta Fed's GDPNowcast, the New York Fed Staff Nowcast, Cleveland Fed, and more institutions

#FederalReserve#FOMC#Powell#inflation

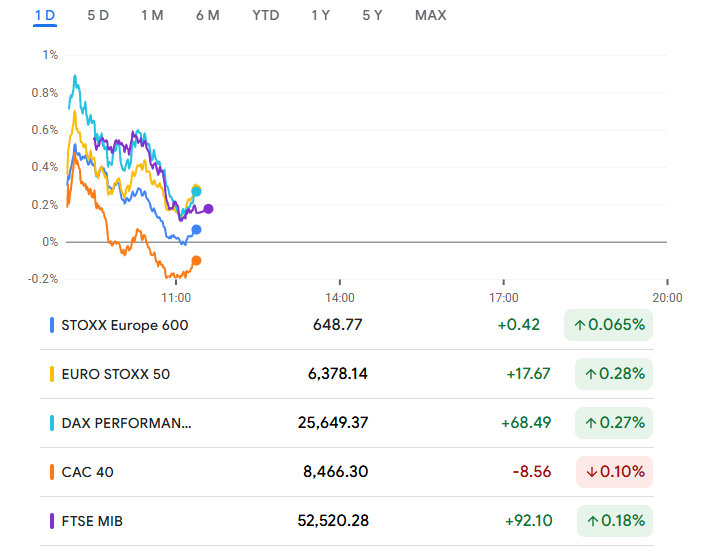

European stocks closed the week at record highs as AI jitters eased

=>The Stoxx 600 notched a fourth straight weekly gain, while a rebound in Samsung and SK Hynix helped lift Asian markets

=>Meanwhile, the U.S. dollar hit a two-week low and gold extended its advance

ECB Decides(11th June): raises all three key interest rates by 25bps:

=> Deposit Facility → 2.25%

=> Main Refinancing → 2.40%

=> Marginal Lending → 2.65%

Inflation forecasts for 2026-27 revised UP on higher energy prices.

Upside risks for inflation. Downside risks for growth

Let's dive into Eurozone stock indices like the STOXX 600, DAX (Germany), CAC 40 (France), FTSE MIB (Italy), and IBEX 35 (Spain). Stay tuned for insights on trends and top performers!

#Eurozone#Stocks#Indices

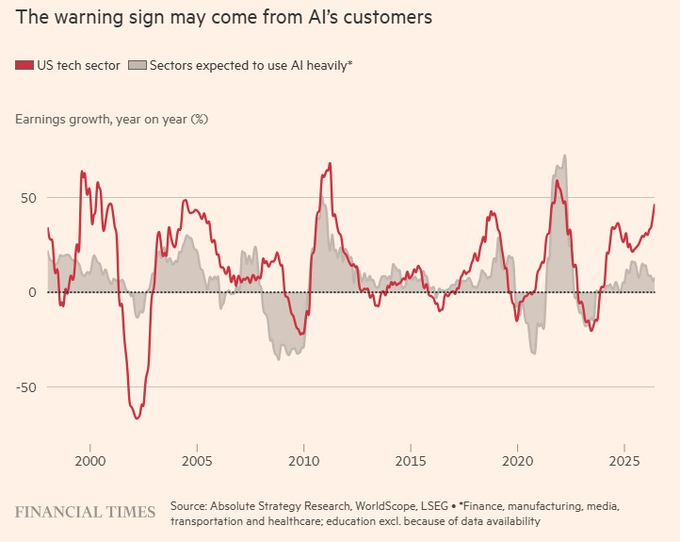

@FT: The real AI test isn't Big Tech—it's their customers. Infrastructure sellers are capturing the gains, but AI users have yet to show a meaningful jump in margins, cash flow, or earnings. Markets will soon demand proof that AI spending is delivering real returns.

BBG: AI pricing is starting to crack. The Silicon Data LLM Token Expenditure Index has fallen nearly 20% from its May peak, raising fresh questions about whether the AI industry's $700B+ capex boom can generate the returns investors are expecting

#SP500#Nasdaq100#Russell2000

Denmark's krone has slipped to record lows against the euro, fueling speculation the central bank is becoming more tolerant of weakness

The currency recently fell to 7.4758 per euro, beyond the level where Nationalbanken has historically intervened to defend its long-standing peg

Let’s talk about the euro’s strength (or lack of it) against other major currencies. From multi-year lows to macro pressures, this thread breaks down what’s weighing on the single currency and where it might go next

#ECB#InterestRates#Eurozone#inflation#Lagarde#TradersKE

Wall Street just posted its strongest first half since 2021, but H2 may be tougher

=>AI spending, stronger business investment, and improving inventories remain tailwinds, while sticky inflation, geopolitics, and U.S. midterm elections could keep volatility elevated

Higher-for-longer interest rates are squeezing the middle market

=> More than 40% of Russell 2000 companies remain unprofitable, leaving many smaller firms vulnerable as rising debt servicing costs consume a growing share of already thin earnings

#SP500#Nasdaq100#Russell2000

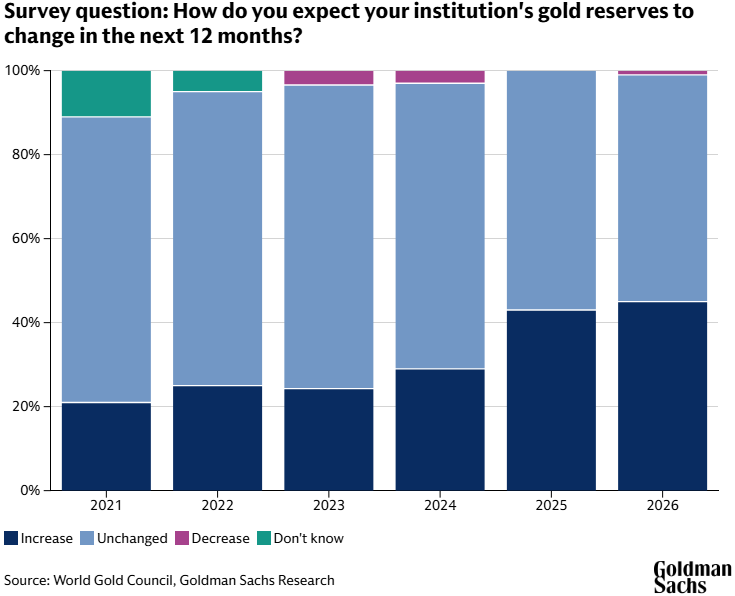

Goldman Sachs Research projects that gold will reach $4,900 by the end of 2026, driven primarily by emerging market central banks diversifying their reserve holdings

#Gold#Copper#Oil#Silver#NaturalGas#Wheat

Happy 250th birthday, America!

=> Two and a half centuries of liberty, innovation, and resilience — here's to the nation that keeps building, growing, and leading forward

#July4th#Semiquincentennial#USA250#Trump

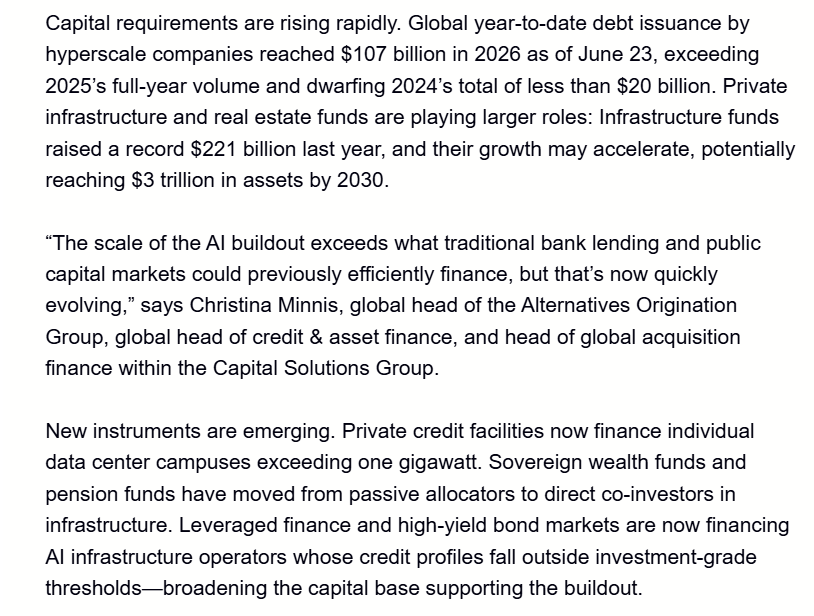

GS: AI's capital needs are accelerating. Hyperscalers have issued $107B in debt so far in 2026, already surpassing all of 2025

=>Private credit, infrastructure funds, sovereign wealth funds, and high-yield markets are becoming key financiers of the AI buildout

GS: AI is driving an industrial reorganization across the global economy.

We estimate the AI buildout will require $7 trillion between 2026 and 2031, funded through equity, debt, sovereign capital, and new financing structures as sectors beyond software embrace AI

#SP500#Fed

Big Tech's Q2 earnings will test whether AI investments are delivering returns

=> Q1 showed improving AI monetization, but investors are increasingly focused on free cash flow, rising capex, debt issuance, and whether hyperscalers can defend their AI leadership

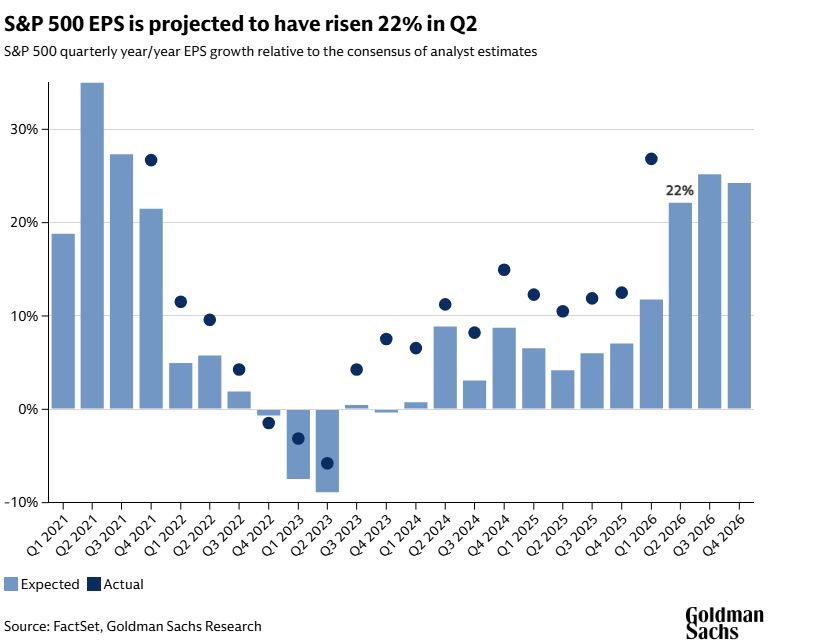

Q2 earnings season, which begins the week of July 13, could set the next direction for U.S. stocks

=> S&P 500 companies are expected to deliver 22% YoY EPS growth after strong Q1 beats, while Goldman Sachs forecasts 24% EPS growth for full-year 2026

#SP500#Nasdaq100#Russell2000

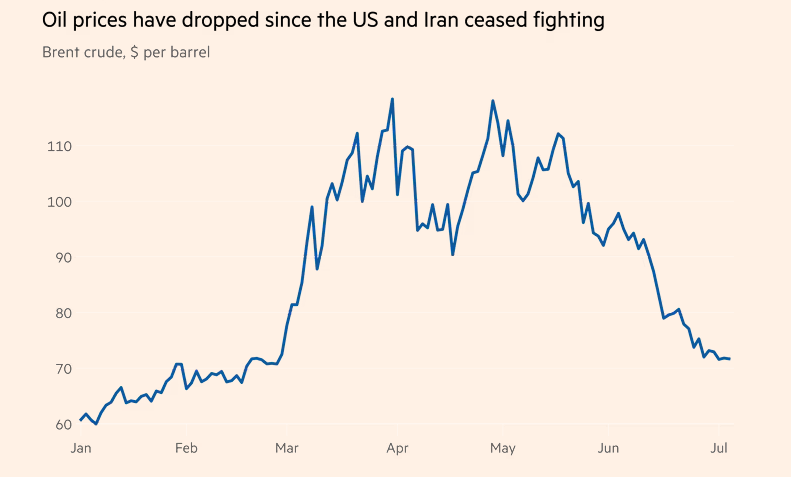

@FT: Citi sees Brent crude falling to $60–65/bbl by year-end, well below the Wall Street consensus of $78

=> The bank expects the U.S.-Iran agreement to hold, easing geopolitical risk, while rising supply could push the global oil market back into surplus

#WTI#Brent

ECB's Moulin:

=>The June rate hike was the right decision

=> The latest inflation data & lower oil prices will make the ECB's job easier

=> Policymakers are in a good position with risks balanced, while cautioning against expecting a sharp pickup in Q2 growth

#ECB

European equities are trading near record highs. The STOXX 600 (+0.09%), Euro Stoxx 50 (+0.30%), DAX (+0.29%), & FTSE MIB (+0.15%) are all higher, while France's CAC 40 (-0.08%) lags

=> Lower oil prices continue to support sentiment by easing concerns over further ECB rate hikes.

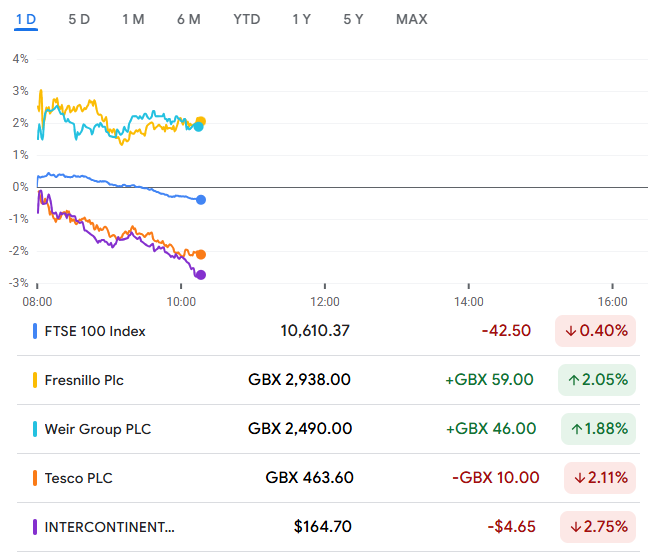

The FTSE 100 opened sharply higher but reversed to trade 0.37% lower

=> Fresnillo (+2.15%) and Weir Group (+1.9%) led the gainers, while InterContinental Hotels Group (-2.72%) and Tesco (-2.0%) weighed on the index as early optimism faded

#UKStocks#FTSE#BoE#UKInflation#Bailey

BoE Decides (June 18th): MPC voted 7–2 to hold Bank Rate at 3.75%, with two members calling for a hike to 4%

=> Energy prices have fallen but remain volatile, CPI is 2.8% and expected to rise later this year

=> Policy stays data-dependent with no change to the stance.

This thread delves into key UK stock market indices, including the FTSE 100, FTSE 250, FTSE 350, FTSE All-Share, FTSE SmallCap, and FTSE AIM All-Share. Stay tuned for insights into what drives UK equities

#UKStocks#FTSE#BoE#InterestRates#UKInflation#Bailey#MPC#UKBudget