Mobikwik has recently made changes to the UI of mobikwik xtra dashboard and its calculation.

Earlier , they were showing Principal repaid and principal outstanding seperately in the dashboard bit recently after lot of people outraged and FIRs and court case against them, they desperately changed their ui to remove the Principal outstanding block from the calculation and instead for this they introduced Lifetime received, Lifetime deposited and concept of Absolute net returns % for which on official production app - they are calculating it as

Absolute net return = (Lifetime received + Lifetime deposited - 1) * 100

literally they just calculateed the ANR % by basic addition, subtraction & multiplication

and there is no division wrto to which they are calculating the return for ANR.

They are hardcore data manipulators and when they say that they have calculated every borrower mapping report, deposits, escrow accounts etc , they are just lying because a company which can't even do basic percentage calculation is surely incompetent to run a fin-tech company.

And interestingly this formula is on Mobikwik xtra dashboard for about a month now so its not placed by mistake.

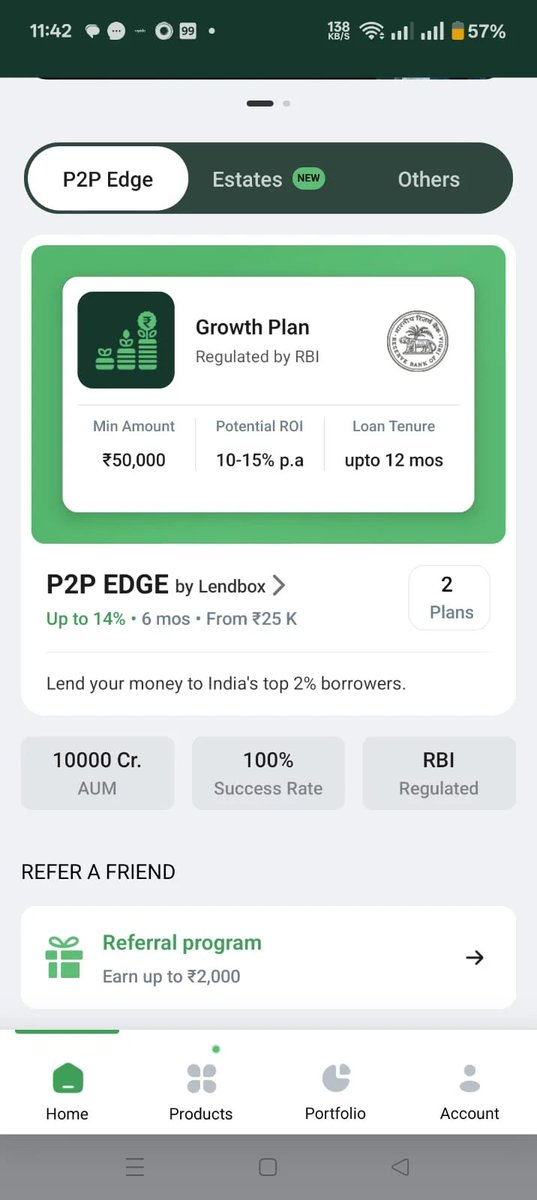

PerAnnum - Lendbox - MobiKwik & RBI's secret conspiratorial relationship for dishonest manipulative purposes to fool middle class investors.

The ongoing crisis of MobiKwik Xtra investors who put their money in the product partnered with Lendbox is a complete betrayal of ordinary Indians. Thousands of retail investors have already lost around 30% of their hard-earned principal. Some are senior citizens who parked their entire life savings in MobiKwik Xtra expecting safety and returns. Many students had saved for higher education. Several middle-class families had plans to buy homes or secure their future. All of that is now in ruins because of this ongoing scam.

PerAnnum, an entity of Lendbox, continues to openly claim 100% success rate and ₹10,000 Cr AUM while pushing P2P lending and other products. This is the same Lendbox that was deeply tied to MobiKwik Xtra.

They are claiming RBI’s regulatory changes of 16 august 2024 but these directions were in place from 2017 RBI guidelines, still they are operating openely under RBI's hood, investors are facing blocked funds, delayed or partial withdrawals, and real losses. The pain is visible — old people struggling to survive, students’ dreams shattered, and middle-class investors watching their home plans collapse.

Here's the link to Rbi master direction 2017: https://t.co/twZaNwFA6B

RBI itself has confirmed that the entire P2P lending sector’s AUM has crashed sharply from around ₹10,000 Cr to just ₹3,000 Cr after its own actions. Here is the clear report: https://t.co/KJn4LdHl8t

Yet PerAnnum keeps marketing up to 15% returns in its P2P Edge product and 40-50% returns in Estates by PerAnnum. RBI has repeatedly clarified that P2P lending must not be treated as an investment product and no returns can be assured or guaranteed. Credit enhancement, buffers that promise “no loss to lender”, and fixed return pitches are all prohibited. Still, these claims are being made openly.

This is high-level misleading marketing designed to fool retail investors. They are selling dream returns while the ground reality is defaults, illiquidity, and stuck money. The same group was fined ₹40 lakh by RBI earlier for violations, yet the misleading pitches continue under the banner of being “RBI regulated”.

Here's the link : https://t.co/oY5TK6vIZq

The full detailed investigation into this risky regulatory dance is here: https://t.co/bMM4VyMoyI

Who exactly is sitting inside RBI and allowing this open looting of common people’s money? These so-called regulators are no less than white-collar terrorists who have destroyed the financial lives of thousands of Indians — senior citizens, students, and middle-class families — while the perpetrators keep operating with bold claims of high AUM and guaranteed success rates. This is not regulation. This is failure at the highest level that has enabled daylight robbery under the garb of licensed platforms.

The suffering is real. The losses are real. The misleading claims are still happening. RBI and the Ministry of Finance cannot keep looking the other way while ordinary citizens lose their life savings in products that were never supposed to promise assured returns in the first place.

Where is the accountability @RBI@RBIsays@FinMinIndia@nsitharaman@nsitharamanoffc ??

A default is not a scandal. Being unable to see your own money is.

Roughly ₹8.85 crore is stuck across 580 lenders in a single P2P lending product, and most of them cannot tell you where that money went.

The product was MobiKwik Xtra, run through Lendbox, an RBI-registered NBFC. The pitch was familiar: returns of up to 12-14%, withdraw anytime, a regulator's tag sitting behind it. For a while it worked. Repayments arrived on schedule, withdrawals cleared.

Then the RBI tightened the rules in 2024. The repayments thinned to a trickle, and for many, to zero.

Defaults are normal in unsecured lending. Anyone who lends to strangers should expect some of them not to pay.

The failure here runs deeper. Lenders were never shown which borrowers they funded, and their money was blocked and redeployed into fresh loans without consent.

DeFi answers this with onchain lending. The record lives on a shared public ledger anyone can read, instead of inside one company's database. Every deposit, loan, and repayment lands there, and no one can rewrite it. A borrower can still default and you can still take the loss. What you do not lose is sight of your own money. You see where it went and what it is doing, every step.

That is the gap MobiKwik Xtra exposed. Not the defaults. The fact that 580 lenders had no way to watch their money move.