@QuantumBullHQ If you wanna talk about undervalued relative to peers, you might wanna check on IQM ($RAAQ, until SPAC goes through in around 1 month or so)

The next evolution of Hermes Agent is here!

Introducing Hermes Desktop: everything you love about Hermes, now native on your machine.

First demoed in Jensen's GTC keynote, it's now in public preview.

Spent the last few days compiling a full historical DD summary on $SHT / Smart High-Tech covering 2022–2026.

17 pages covering:

• customer validation

• AMD track

• Thermal Grizzly / KryoSheet

• Henkel partnership

• production scaling

• AI commercialization / NVIDIA path

• AGM notes & observations

• key milestones, risks and timeline

Built from company communications + own AGM notes.

An attempt to create one structured source for anyone trying to understand where the company actually stands after 3+ years of development.

(N.b. Posted same information in swedish yesterday)

🧵1/2

AGM notes from today’s $SHT meeting.

The AGM was very informative. There were many opinions raised during the meeting itself — in my view, many of them reasonable.

Several different people held their own presentations.

From Gang Wang’s presentation, he stated among other things:

“Massive orders are coming within a few months and we have the capacity.”

Their technology is completely unique, they are first with this, and are therefore pioneering this technology shift.

According to discussions during networking/mingling, the China factory is almost fully automated and development there is moving very fast. They will likely need either a larger factory or an additional factory in China as they scale significantly in order to meet demand.

According to Michael Quail’s presentation, no other company is doing what SHT is doing — no one has a comparable product. Because of this, the company can, according to him, price its products at a substantial premium since this is a “diamond product”, which should result in high profitability.

In his entire career at Henkel, he has never seen a company like SHT. He has enormous respect for Johan Liu and his knowledge.

During his presentation it was also confirmed that NVIDIA is the customer they are working toward and are approved by.

He believes SHT is heading toward commercial success:

“They are climbing Mount Everest and they are on the last push to the top.”

According to him, it is important to focus on one major customer at this stage rather than starting with several.

Beyond semiconductors / AI, there is also strong demand from automotive and electronics.

From Johan Liu’s presentation:

He stated that he has been in China for five weeks. He felt that a lot is happening and that the product has a very strong future, which is why he remained there.

Liquid metal does not work for NVIDIA — this has been tested.

All competing solutions also show weaknesses/problems, while classical solutions age far too quickly.

NVIDIA is not satisfied if SHT can only produce for CPUs — they also want solutions for entire modules including GPUs.

If they succeed in delivering, there is “nothing that can stop them”, according to Liu.

The TIM market is growing very rapidly. TAM for this market alone is tens of billions USD.

TIM 1.5 is the new technology replacing the traditional TIM 1 & TIM 2 setup — this is what they are targeting and what they believe will become the new standard.

The new chips are very large.

There are no previous solutions for these new large GPUs/CPUs.

Production is done through machines capable of producing 100,000 units per machine. They currently have 2 such machines, and achieving this would become “a gold mine”, according to Liu.

Today they have 35,000 units/month approved by NVIDIA, but capacity is higher than that.

Large shareholders were dissatisfied with how the latest directed share issue was conducted and wanted auditors and other parties to review how it was handled.

Items 12 and 13 were removed from the agenda.

As a result, they have not expanded the articles of association and do not currently have issuance mandates in that respect.

CFO:

USD 5M in prepayments from Henkel are expected during this year, but this depends on progress in commercial orders and ramping production capacity.

“This company will grow — that is one thing that is very certain.”

According to the CFO, they will become a globally leading listed company.

The goal is that customers should pay for development, not investors through equity raises.

Lemonade’s Q1 results are 🔥. So much to share, where do I start?

First, get into the AI mood, click this, + volume ⏫

https://t.co/IDPCvrTHge (by @kidfrancescoli)

🚀10th consecutive quarter of accelerating IFP growth

🔥 Topline at $1.33 Billion (IFP +32%)

🔥 Revenue grew 71% to $258M

🔥 Gross Profit increased 159% to $100M

🔥 3.14M Customers

🔥 Adj. Free Cash Flow $17M

Lemonade Pet exploding!

✅ Surpassed $500M top line early in Q2

✅ #1 most searched pet insurance brand in the U.S.

✅ @lemonade_inc is now the 4th largest pet carrier in the U.S.

✅ AI-powered automation drives record claim handling efficiency (LAE: ~4%)

✅ Our data + tech edge lets us lower prices while boosting profitability

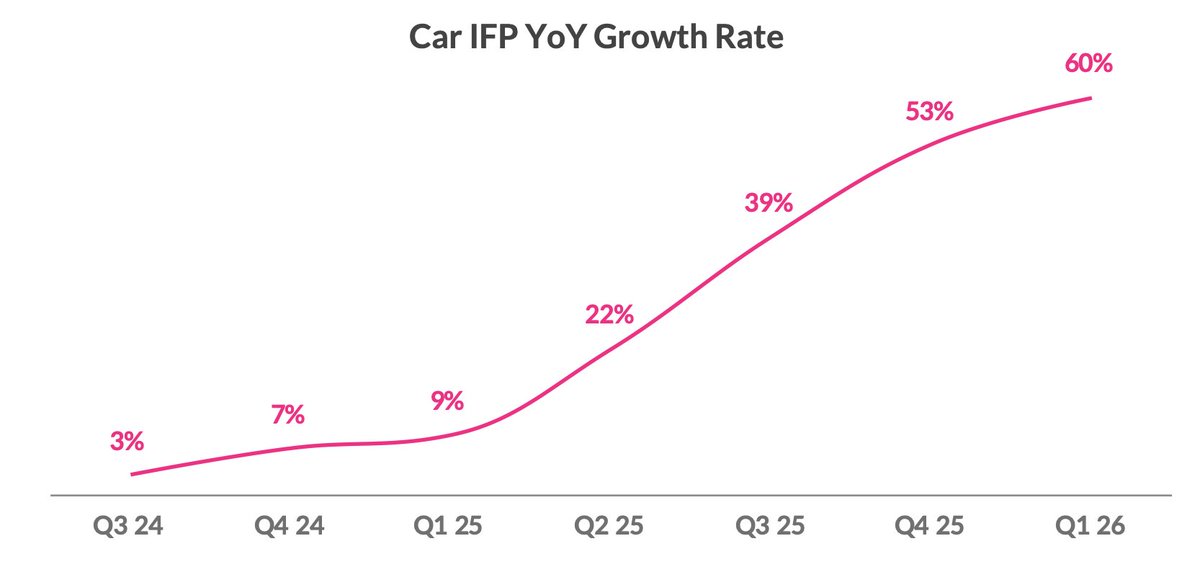

Car picking up speed

✅ Now at 60% YoY growth, $214M IFP

✅ Loss ratio improved to 74% (14 pts better YoY)

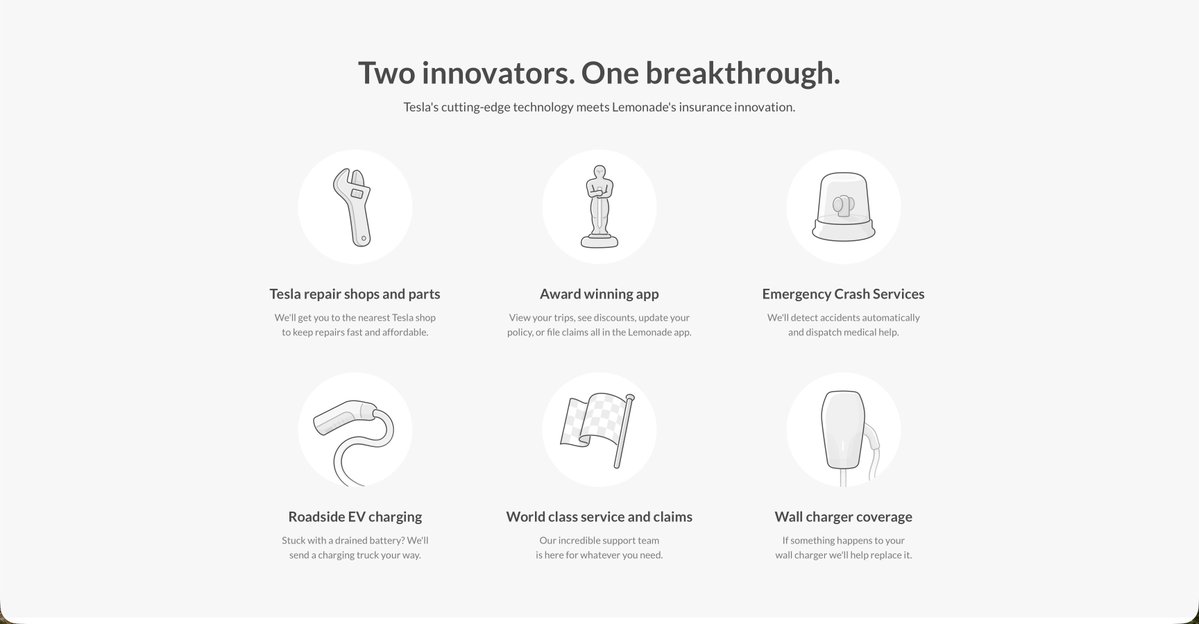

✅ Autonomous Car for @Tesla FSD conversion rate 70% higher than standard

And more...

↗️ Raising 2026 top & bottom line guidance

↗️ IFP per employee > $1M (3x improvement in 4 years)

↗️ Positive Adj. EBITDA in Q4

↗️ Investor Day in NYC November 17

Together with RDW, we have officially completed the final vehicle testing phase for Full Self-Driving (Supervised) and have submitted all documentation required for the UN R-171 approval + Article 39 exemptions. The RDW team is now reviewing the documentation and test results package internally. They have communicated the expected approval for Netherlands date of 4/10, shifting from 3/20 previously and we look forward to successful completion of this cooperation.

Following the Netherlands’ approval, European countries will be able to recognize this approval nationally. We are anticipating a possible EU-wide approval during the summer.

Over the past 18 months, this approval has involved a series of intense documentation, development, testing, research & audits. Including but certainly not limited to:

– 1,600,000+ km of FSD (Supervised) testing on EU roads

– 13,000+ customer sales ride-alongs

– 4,500+ track test scenario executions

– Thousands of pages of written documentation for 400+ compliance requirements

– Dozens of research studies into safety performance/results

We're extremely proud of the work conducted with the RDW team up until this point.

We very much look forward to the approval in April, and sharing FSD (Supervised) with our patient EU customers!

Many insurers are issuing AI press releases. It's all very exciting.

So at @lemonade_inc we built an AI BS detector: three KPIs, public data, no spin.

It won't boost our popularity. It might boost your returns.

https://t.co/Ua8vWxkObh

Presenting @Lemonade_Inc’s Q4 2025: our strongest quarter ever!

Recommended: Play this while reading- https://t.co/jHFp0vsNcn

Highlights (Y/Y)

🚀 9th consecutive quarter of accelerating growth

💵 $1.24 billion top line (+31%)

🔥 Revenue: up 53%

🔥 Gross profit: up 73%

🔥 Cash flow: generated $37m (adj. FCF)

🔥 ~3m customers

🔥 Adj. EBITDA loss improved 81%, now just -$5m

Car and Autonomous

✅ Lemonade Car grew 53%, now at $187m

✅ Loss ratio: 70% (TTM, down 23 points)

✅ Launched Autonomous Car Insurance for @tesla FSD (Supervised)

Europe

✅ Grew 150%

✅ 10th consecutive quarter of triple digit growth

✅ Loss ratio: 64%

AI Spotlight

✅ In the last 13 quarters- headcount shrunk 6%, while adding 1.2m customers

✅ 68% reduction in Pet cost-per-claim: from $44 in 2021, to $14 now

✅ Claims LAE at a record 6% (vs. 9% industry avg.)

More...

✅ Record breaking LMND gross loss ratio: now at 52%

✅ Growing cash (and investments) in the bank: $1.12B

Up next

⬆️ Guiding to 32% IFP growth in 2026

⬆️ 60%+ revenue growth

⬆️ Q4 2026 first positive adj. EBITDA quarter, 2027 - full positive year

⬆️ Announcing our upcoming investor day @ NYC, Nov ‘26.

Full details + financials: https://t.co/gDgJGSVuac

And... we're ON.

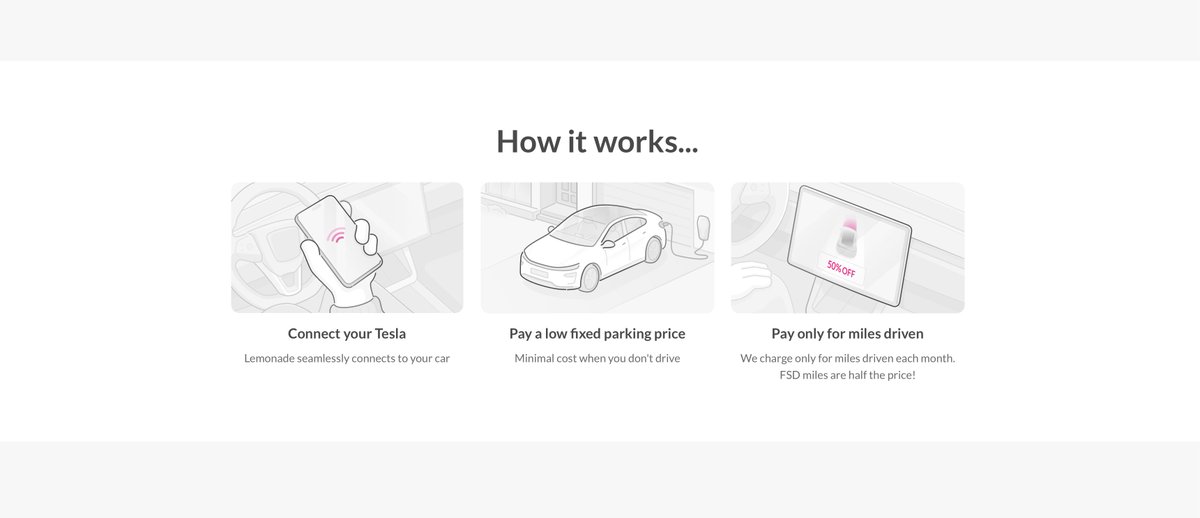

@Lemonade_Inc's Autonomous Car for @Tesla FSD is now live in Oregon.

Tesla drivers in Oregon can now get ~50% off their Tesla FSD-driven miles + the best car insurance experience in the US, bar none.

https://t.co/vimFfgeXDj

In the 3 years since ChatGPT launched, Lemonade’s revenue ~3×, gross profit ~10×, +1.25M customers — with fewer employees.

As a CEO, I love that. As a father, I can’t leave it there.

That’s why I founded MOSAIC — and why we’re publishing the MOSAIC Model today: a blueprint for universal high income, funded by AI abundance.

👉 https://t.co/55HoJCjFBe

NEWS: Lemonade’s 50% insurance discount for drivers using @Tesla FSD (Supervised) is now live in Arizona.

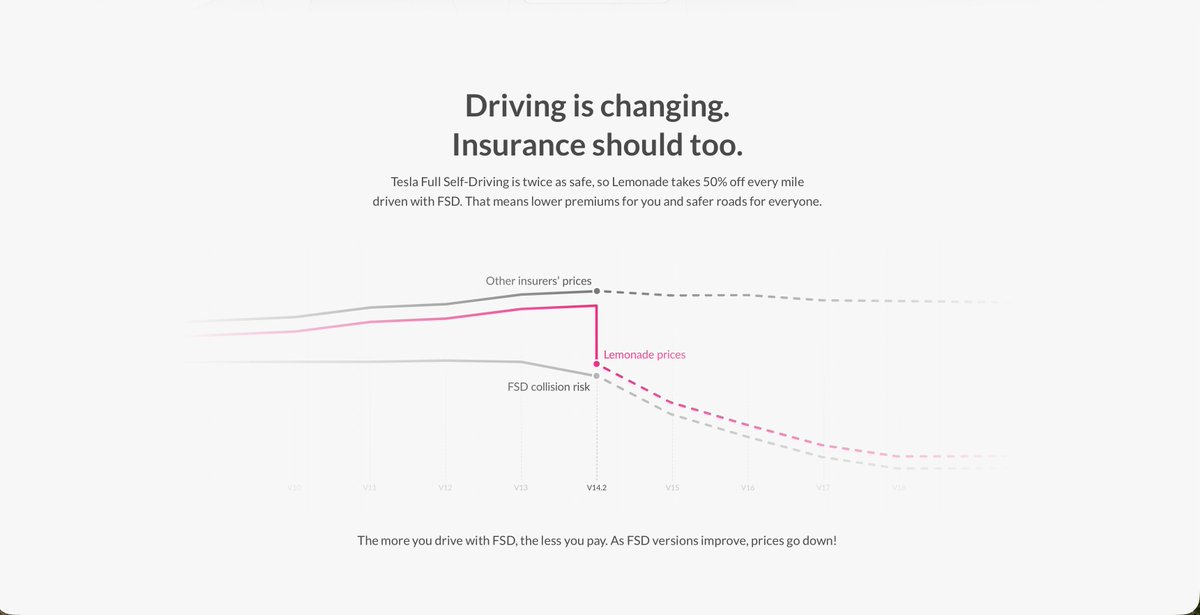

"Tesla FSD is twice as safe, so Lemonade takes 50% off every mile driven with FSD. The more you drive with FSD, the less you pay. As FSD versions improve, prices go down."

Expansion to other states is expected in the coming weeks/months.