Transparency is a of the upmost importance for us at Sorla. We want to build a community with a foundation in trust and this is one good step in the right direction.

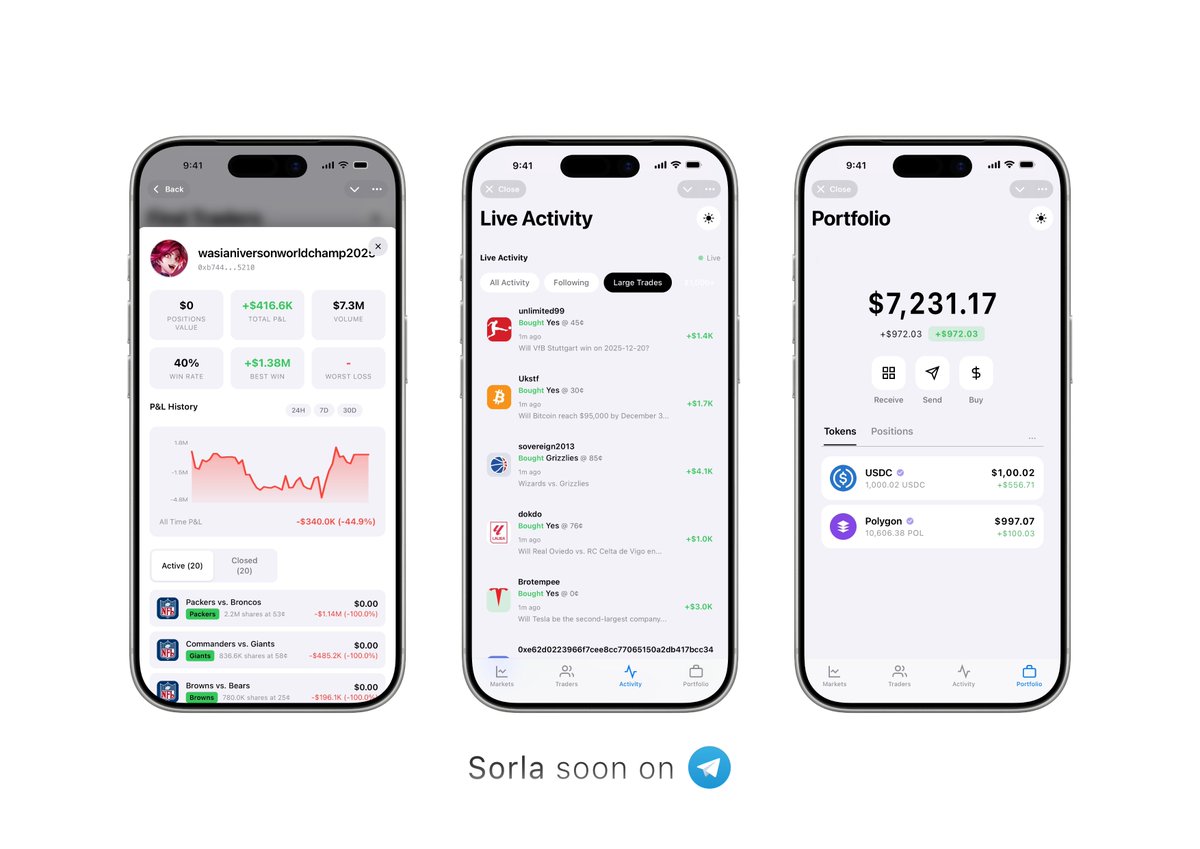

Prediction markets are coming to Telegram.

Alongside our iOS app, we’re launching a Telegram mini-app that makes prediction markets instantly accessible and fully cross-platform.

Coming soon.

Catch @AdamLastak on here January 2026!

He will be talking a little about Sorla and the direction we’re headed +will be taking about prediction markets as a whole.

$ZETA: 17 straight beat-and-raise quarters, but the stock is still stuck around the high teens - exactly the kind of quiet compounder the market only recognizes late.

Zeta is building the brain of modern marketing: an identity-first AI platform that stitches fragmented customer data, orchestration, and media into one system, fixing what $ADBE and $CRM struggle to unify through bolt-on tools. Enterprises are voting with their budgets, with dozens of Fortune 100 customers and rising platform usage as AI agents like Athena move from slideware to daily workflow. Leadership is a real edge: founder-CEO David Steinberg has steered Zeta since 2007, while executive chairman John Sculley brings the scale-it-playbook from his $AAPL CEO era.

Despite this execution, Zeta still trades on a modest forward multiple versus high-flying software peers, even as guidance and long-term targets keep stepping up through 2026 and beyond. The core idea: if marketing is moving from “channel tools” to “AI operating systems,” Zeta is one of the few vendors architected from day one for that world, not retrofitted into it

$NFLX isn’t a rocket ship anymore. With the Warner Bros deal, it looks more like a big, debt-heavy media company that has to prove it can execute. The Warner Bros deal isn’t a flex – it’s an ~$83B admission that organic growth is slowing, and Wall Street is already cutting targets toward where the stock trades today.

The buy gives Netflix huge franchises and more content, but also a huge debt load and big merger risk. Growth is now mid-teens, not explosive, and future returns depend on cost cuts, higher prices, and paying debt down over years – a value-style path, not a classic growth story. Bulls now own a levered, slow‑growth media roll‑up at ~40x earnings, with leverage moving toward roughly 4x EBITDA and turning this into a balance‑sheet story, not a pure growth compounding story.

Prolonged antitrust review freezes buybacks and adds headline risk, while any slip from the promised $2–3B cost synergies pressures the multiple, regulators could still block the deal and trigger a ~$5.8B breakup fee.

Rosenblatt and others have already slashed targets toward ~$105 as the “overpay + leverage” narrative spreads, even as a few holdouts still talk up upside into the $140s. Net‑net, $NFLX now trades on deal risk, leverage and multiple compression, not surprise growth beats – making shorts/puts not only an alpha bet but also a way to hedge left‑tail shock in growth-heavy portfolios.