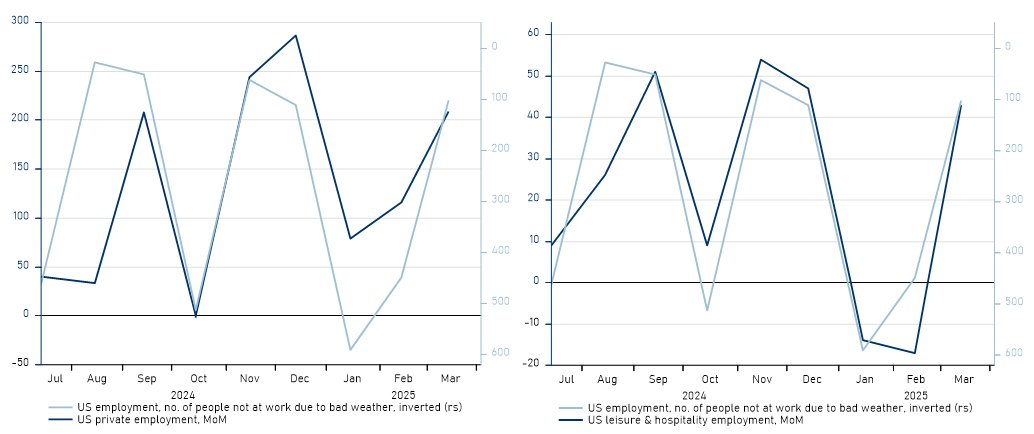

Nonfarm payrolls strength very much driven by normalization of negative weather impacts during Jan/Feb. Absence due to bad weather, which remained elevated in Feb, signals broader weather impacts on employment. Especially visible in sectors like leisure/hospitality.

Temporary boost, and old news.

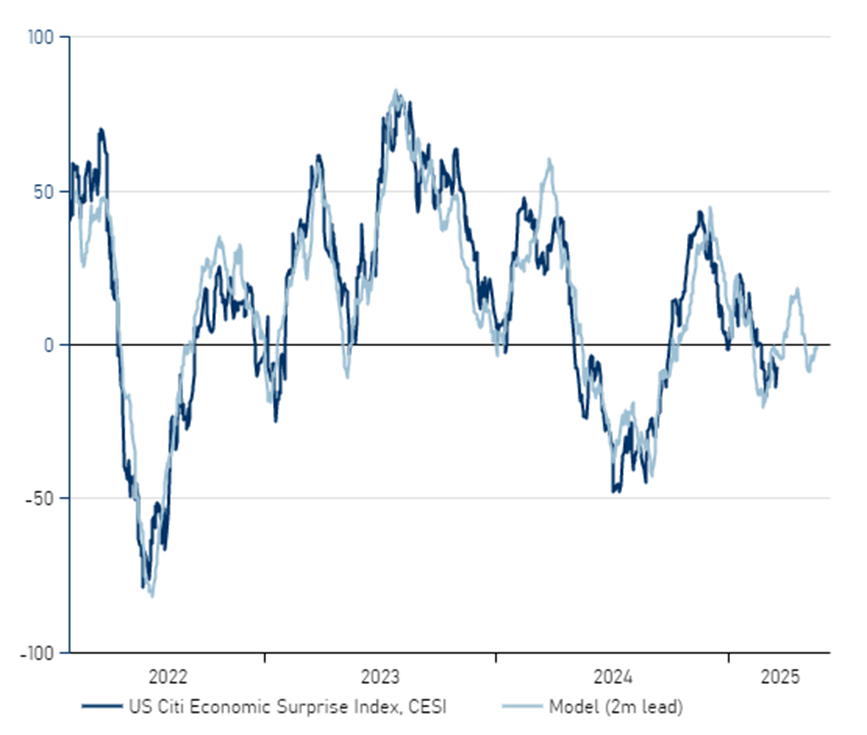

US fiscal dominance continues, with fiscal again compensating for tight monetary policy. Fiscal was key to both the Q2/Q3 growth scare and the macro improvement that followed. Not yet rolling over.

Weaker October NFP indicated by US employment proxies after predicting last month's positive surprise. Hurricane impacts make markets more likely to look past it but if proxies don't improve from here we should start topping process in US rates in November

@CavaggioniMario Slightly perhaps, but I don't think infra spending will roll out quick enough to time the Chinese slowdown, and it's spread out over several years.

China will gradually start to weigh on the global industrial cycle. Shouldn't hamper the global (services) recovery in the end, but can affect macro surprises more given the tilt towards manufacturing in popular macro figures (incl. ISM, which is quite internationally exposed).

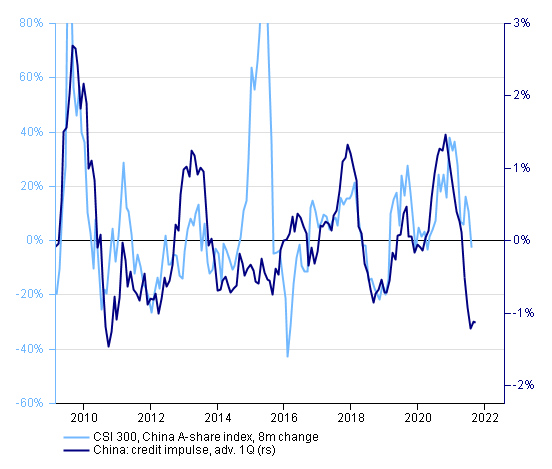

🇨🇳 Another weak credit figure. Credit impulse bottoming out, but still deeply negative. Easy to blame regulation for all the woes in Chinese equities, but a weak backdrop is most likely exacerbating market moves.

@shehzadhqazi In my experience imports components are generally quite good at capturing domestic demand (e.g. ISM imports components tend to capture GDP growth better than others). Imports are ofc also a key way in which Chinese macro affects RoW.

🇨🇳 Weak trend in Chinese money/credit data persists. Probably contributes to the loss of momentum in inflation expectations, but given US macro strength it will have less impact on real yields (and not be the death of the value trade).