"Bitcoin isn't backed by anything."

Let me stop you right there.

Bitcoin is backed by energy. Real energy. Kilowatts. Heat. Physics.

The kind of backing you can't print, fake, or vote into existence at an emergency Fed meeting.

Every block mined is a thermodynamic proof of work. Not a promise. Not a policy. Proof.

The issuance schedule has never been amended by a committee. Not once. Not ever. Because there is no committee.

There's just math. Cold, indifferent, and immune to political theater.

The network is secured by more raw computing power than anything humanity has ever built. Hundreds of exahashes per second standing guard. Every single day.

Now let's talk about what is backed by nothing.

The dollar.

It's is backed by confidence. Specifically, confidence in the institution that printed $6 trillion in two years while telling you 3% inflation was healthy and you should be grateful for the soft landing.

In the same people who can't pass an audit.

Who fund wars with a credit card.

Who promise solvency while sitting on $39 trillion in debt and accelerating.

"Backed by nothing" isn't an attack on Bitcoin.

It's a confession about the dollar.

Follow if you're serious about building wealth they can't print away.

The dollar didn’t just weaken — it quietly robbed you. Down 28% in five years.

My parents bought their house in 1962 for $16,000.

Back then, gold was $35 an ounce. That house cost 457 ounces of gold.

Today, the house is “worth” $750,000. Gold is about $3,300 an ounce.

That same house is 227 ounces of gold — half the real value.

Everyone thinks they got rich. They didn’t. The measuring stick got warped.

That’s the scam of inflation. Prices go up, politicians get away with it.

People confuse bigger numbers with more wealth.

A million dollars today feels impressive — until you realize it’s the purchasing power of about eighty grand in 1970.

You’re not richer.

The currency is weaker.

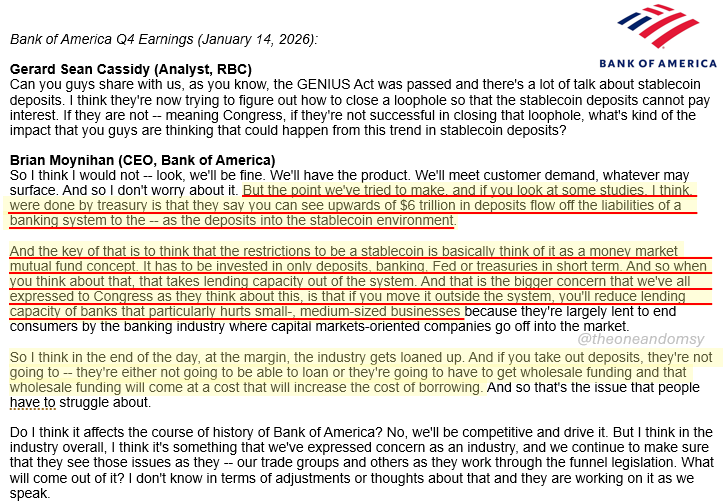

Bank of America CEO on why stablecoins shouldn't pay interest:

(TLDR: consumers shouldn't earn yield so banks can)

Quick summary:

Interest on stables -> mass deposit flight

Fully reserved money -> no fractional leverage

Banks lose free funding -> profits go bye bye!

53 banking associations just wrote themselves a $6.6 trillion protection bill.

They called it the CLARITY Act.

Here is what they do not want you to understand.

Banks pay depositors 0.1% interest. Stablecoin issuers hold Treasury bills earning 4.5%. If stablecoins could pass that yield to users, banks lose the deposit war. They cannot compete. The math is fatal.

So they made competition illegal.

The Kansas City Fed calculated what happens if stablecoins pay competitive rates. Banks lose 25.9% of deposits. $1.5 trillion in lending capacity vanishes. The entire community banking model collapses.

Their solution was not innovation. Their solution was legislation.

The CLARITY Act everyone is celebrating contains Section 404 prohibiting yield payments through any mechanism. Not just from issuers. From exchanges. From affiliates. From partners. Every single pathway to competitive returns, closed by statute.

Brian Armstrong reviewed the 278-page draft for 48 hours. He withdrew Coinbase support at 11pm. The markup was postponed by morning. He saw what Wall Street analysts missed entirely.

This is not crypto regulation.

This is Dodd-Frank for digital assets. Incumbents writing rules that crush competitors. Regulatory capture so brazen they published the lobbying letters on their own websites.

The American Bankers Association. 52 state banking associations. The Community Bankers Council. All coordinating to eliminate an industry they cannot beat in open markets.

Meanwhile China made e-CNY interest-bearing on December 29.

America is banning stablecoin yield while Beijing is paying it.

The crypto industry spent years begging for regulatory clarity.

They got it.

Clarity that $6.6 trillion in deposits will be protected at any cost. Clarity that banks write the rules. Clarity that if you cannot win in markets, you win in Congress.

This is the largest regulatory capture event in American financial history.

And it is being sold as innovation policy.

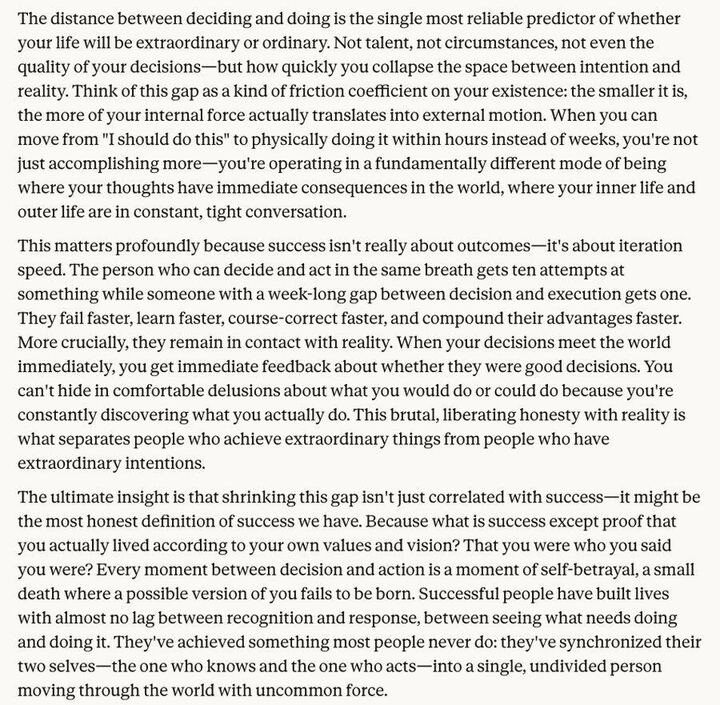

“The distance between deciding and doing is the single most reliable predictor of whether your life will be extraordinary or ordinary.”

These three paragraphs will change your life:

@cryptorover The volume of shares held in indices such as MSCI is 20%, so leverage remains considerable despite this decision not to take into account the issuance of new shares to rebalance MSTR's position in the index.

@ZynxBTC The volume of shares held in indices such as MSCI is 20%, so leverage remains considerable despite this decision not to take into account the issuance of new shares to rebalance MSTR's position in the index.

GOLD CANNOT PROVE IT IS GOLD

Yesterday in Dubai, Peter Schiff held a gold bar on stage.

CZ asked one question: “Is it real?”

Schiff’s answer: “I don’t know.”

The London Bullion Market Association confirms there is only one method to verify gold with 100% certainty: fire assaying. You must melt it. Destroy it to prove it.

Bitcoin verifies itself in seconds. No experts. No labs. No destruction. A public ledger secured by mathematics that 300 million people can audit simultaneously from anywhere on Earth.

For 5,000 years, gold’s scarcity was its value proposition. But scarcity means nothing if authenticity cannot be proven.

The numbers no one is discussing:

Gold counterfeiting affects 5 to 10 percent of global physical markets. Every vault, every bar, every transaction requires trust in someone.

Bitcoin requires trust in no one.

Gold market cap: $29 trillion built on “trust me.”

Bitcoin market cap: $1.8 trillion built on “verify it yourself.”

This is not speculation versus stability. This is the 21st century verification cost inversion.

When the world’s most famous gold advocate cannot authenticate gold in his own hands, the thesis writes itself.

Physical assets that cannot prove their own existence will lose monetary premium to digital assets that prove themselves every ten minutes, every block, forever.

The question is no longer “Is Bitcoin real money?”

The question is: “Was gold ever verifiable money?”

Watch institutional flows. The reallocation has begun.

What you witnessed yesterday was not a debate.

It was a funeral.

BREAKING: The United States Just Ended the Offshore Crypto Era

December 4, 2025.

The CFTC has authorized spot Bitcoin and cryptocurrency trading on federally regulated exchanges for the first time in American history.

Read that again.

For fifteen years, the agency refused to provide regulatory clarity. Americans were forced offshore. They traded on platforms with no customer protections. FTX collapsed. Billions vanished. Retail investors were decimated.

That era is over.

Acting Chairman Caroline Pham invoked existing Commodity Exchange Act authority requiring leveraged retail commodity trading occur only on futures exchanges. No new legislation. No Congressional delay. Immediate implementation.

Bitnomial goes live December 9. Leveraged spot. Perpetuals. Futures. Options. Portfolio margining. One venue. Full federal oversight.

The structural implications are staggering.

Cross margining between spot and derivatives could compress capital requirements by 30 to 50 percent. Institutional barriers dissolve overnight. Pension funds. Banks. Sovereign wealth. All now have compliant access to spot crypto on platforms that have operated as the gold standard for nearly a century.

Pham stated the goal explicitly: Make America the crypto capital of the world.

This is not rhetoric. This is infrastructure.

The SEC and CFTC issued joint guidance in September. The President’s Working Group on Digital Asset Markets provided the roadmap. Tokenized collateral including stablecoins is next. Blockchain settlement frameworks are in development.

Watch for Bitnomial volumes exceeding one billion monthly by Q1 2026. Watch for CME integration announcements. Watch for offshore exchange user migration accelerating through H1.

The question is no longer whether America leads digital asset markets.

The question is how fast capital repositions.

Fifteen years of regulatory ambiguity.

Resolved in one announcement.

The new financial architecture has begun.

YOU ARE WATCHING THE BIGGEST MARKET MANIPULATION OF 2025 IN REAL-TIME. 🚨

THEY CREATED THE FUD TO BUY THE EXACT BAGS YOU JUST SOLD.

THE TIMELINE THEY DON'T WANT YOU TO SEE: 👇

The JPMorgan and Strategy situation didn’t begin with the October crash. It goes all the way back to May.

And when you look at the dates, the whole dump starts to look intentional.

It started in May 2025, when Jim Chanos publicly announced he was Long Bitcoin but Short Strategy.

This created a specific narrative: "Support Bitcoin, but bet against the largest public holder of BTC."

Then in July 2025, JP Morgan quietly raised the margin requirement for MSTR from 50% to 95%.

For those who don't know, a rising margin requirement forces big liquidations if more collateral isn't posted. This move alone weakened MSTR weeks before any MSCI news existed.

After that, in August, JP Morgan released documents for a new structured product tied to BlackRock’s IBIT.

Even before the MSCI issue, the bank was already positioning itself to offer Bitcoin exposure, but through IBIT, not MSTR.

Then October 10th happened.

MSCI released the consultation note targeting companies holding 50%+ of their assets in digital assets.

And there’s one critical detail most people missed: MSCI was originally built inside Morgan Stanley, the same ecosystem now issuing their own Bitcoin-linked products.

4 days later, Morgan Stanley filed for an IBIT-linked structured product with the SEC.

It aligned perfectly with the narrative: BTC-heavy operating companies may not fit MSCI classification anymore, but their new financial products do.

Two weeks ago, JP Morgan followed with their own IBIT-linked product filing.

Then on November 20, JP Morgan executed two moves simultaneously:

1️⃣ Published the documents to sell their IBIT Note.

2️⃣ Resurfaced the MSCI threat against MSTR.

Now, the pattern looks very clear:

• Weaken MSTR liquidity.

• Launch Bitcoin-exposure bank products.

• Raise doubts about BTC-heavy public companies.

• Highlight the MSCI risk exactly when the market is most fragile.

• Let capital shift toward IBIT-linked products offered by big institutions.

This is not the first time this has happened.

JP Morgan, Goldman Sachs, and others have FUDed BTC for years. And now? They are some of the biggest institutional holders.

These institutions don't buy the blood. They create it. 🩸

If you are still panicking looking at their FUD, you will always panic sell and FOMO buy.

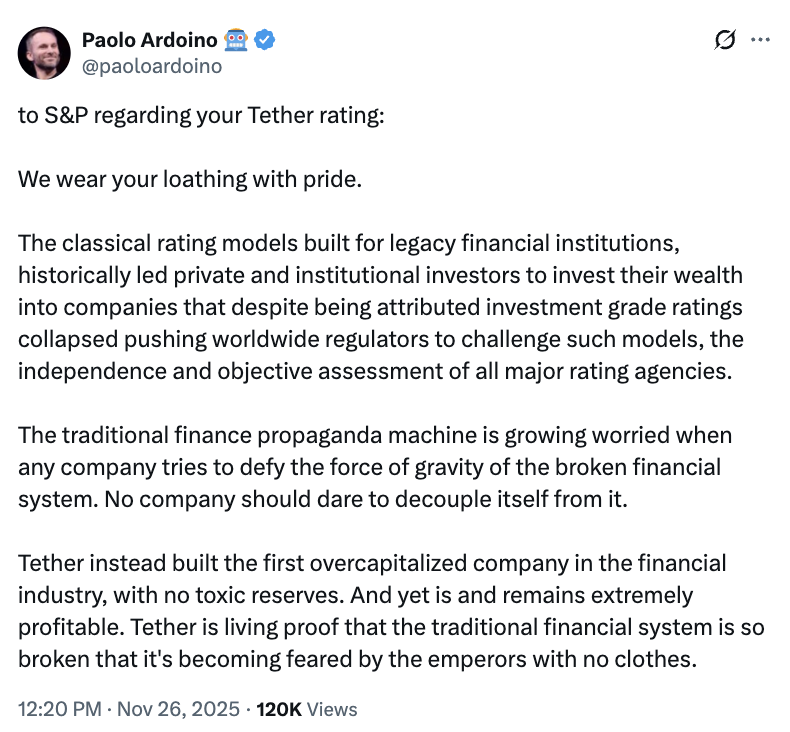

🚨 NEW: Tether CEO Paolo Ardoino fires back at S&P after its Tether rating, saying the agency’s legacy models failed investors for decades and that Tether is overcapitalized "with no toxic reserves.”

He adds: “We wear your loathing with pride.”

The October 10th Crypto Crash WAS Coordinated!

MSCI, JPMorgan, and key political players moved in sync, pressuring $MSTR and targeting Trump’s ENTIRE crypto ecosystem.

I break down the exact timeline, the evidence, and what comes next on @Crypto_1nsider

https://t.co/qJgLkWMHhD

I recently had coffee with a London based hedge fund manager while we were both staying in Downtown Dubai.

He said he that a lot of the big fund managers are conspiring against Michael Saylor because it will make them look bad if bitcoin keeps doing well and they were late to the party.

So in attempt to keep their investors happy they are pulling out all of the tricks to keep bitcoin down.

ANALYSIS 5/5

Ultimately the achiles heal of all these BTC treasury companies is that if NAV goes below 1, there is nothing to compel it to go back to 1 other than share buybacks.

But MSTR won't sell BTC to do a share buyback, and they need all the power of the debt markets just to continue paying their preferred dividends.

What that means in MSTR is on hold until BTC goes up. They can't do much right now.

More later.