$AAJ took a while but a great acquisition (Vale the partner in the project)

Drill hits 80-100m Cu @ 1.6% - 2% Cu

Shallow

Good jurisdiction

Resource not constrained

MC ~13M Undiluted ~23M diluted

$AAJ still has other projects

Short summary on HC here

https://t.co/qOuSo52BDG

Been chipping away at a Aus micro cap gold/copper play.

$AAJ

-2.5M MC with ~1.6M cash. Raise just done. 1M EV

-Drilling commence 2-3 weeks ago on follow up gold at salmon gums.

-Has large scale project potential

-Strong news flow next 3-6 months.

*I was NOT part of the raise*

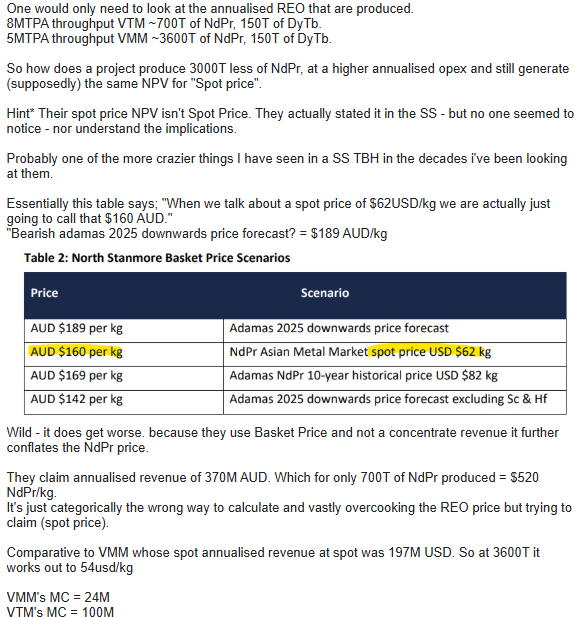

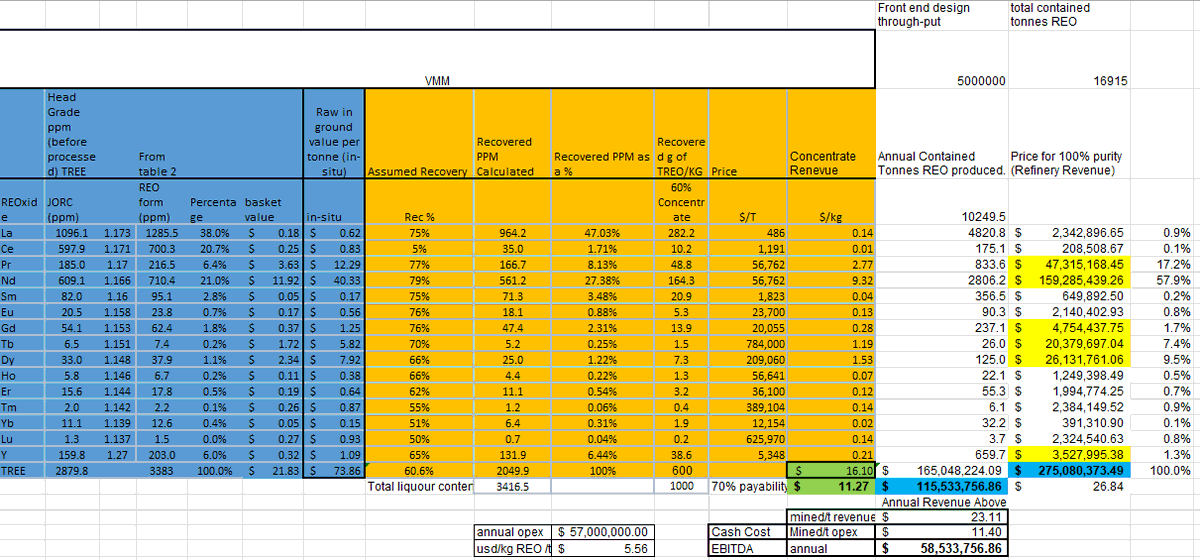

$VMM lowest quartile for AISC according to the studies makes the project viable in all pricing cycles.

Other projects need agreed pricing higher than spot long term to have a positive NPV.

$AAJ is a recent Copper play I’m speculating on.

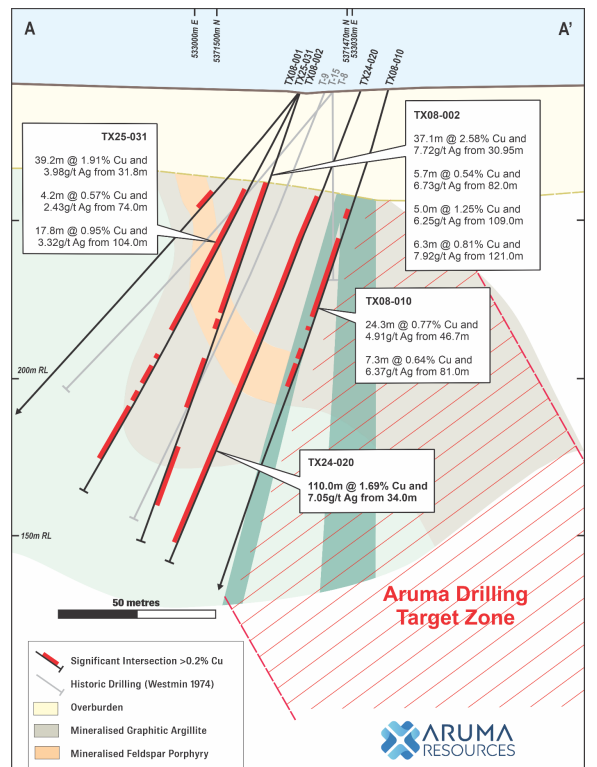

Historic drilling already proved very solid high-grade Cu-Ag: 110m @ 1.69% Cu and 92m @ 2.12% Cu.

New EM suggests a conductor may extend to ~400m depth.

EV only ~$7M. drill results due in May. Happy to die on the sword if wrong.

$VMM lowest quartile for AISC according to the studies makes the project viable in all pricing cycles.

Other projects need agreed pricing higher than spot long term to have a positive NPV.

Viridis Mining and Minerals $VMM is progressing discussions with partners in the US and Europe to secure rare earth offtake agreements, supporting diversified supply chains amid growing geopolitical pressures.

As highlighted by Bloomberg, these efforts reflect increasing demand for reliable rare earth sources outside China and reinforce the strategic importance of our Brazilian projects in meeting global needs.

Read more here 👇

https://t.co/lwIk0B78qS

#RareEarths #CriticalMinerals #VMM #Colossus #Project #Brazil #SupplyChain #Viridis

MRG Metals (#ASX: $MRQ) has strengthened its portfolio with the acquisition of the high-grade Garies Rare Earth Project in South Africa, marking a key step in building a diversified critical minerals business.

The acquisition adds a magnet-rich rare earth asset with exceptional grades and a defined pathway toward development, complementing MRG’s fully funded Heavy Mineral Sands Joint Venture in Mozambique and its rapidly advancing Adriano–Fotinho rare earth portfolio.

Read more: https://t.co/wr7RTkPYMA

@sonofhippocrate@Roon_aus If you’ve got a solution for how to raise money and not cause dilution let the ASX directors know because you’ve cracked the code for non revenue generation public listed companies and how to raise funds.

Dilution is just reality in spec investing.

Stick to trading - IMO

$MRQ

Only 3/23 identified targets have been partially drill tested to date, “significant mineralised tonnage with grades exceeding ~4% TREO”

4% TREO hardrock is economical. Now proving a mineable resource now.

This excludes the 50M USD JV payment for HMS proj

10-15M MC AUD

@sonofhippocrate@Roon_aus You’re right they should raise money at twice the trading shareprice. I’m sure loads of investors will be happy to give money at a premium. (Sarcasm)

This was raise at/above last trading price.

I’ll take economic and sovereign risk over a dead rubber in Aus. That’s me though.

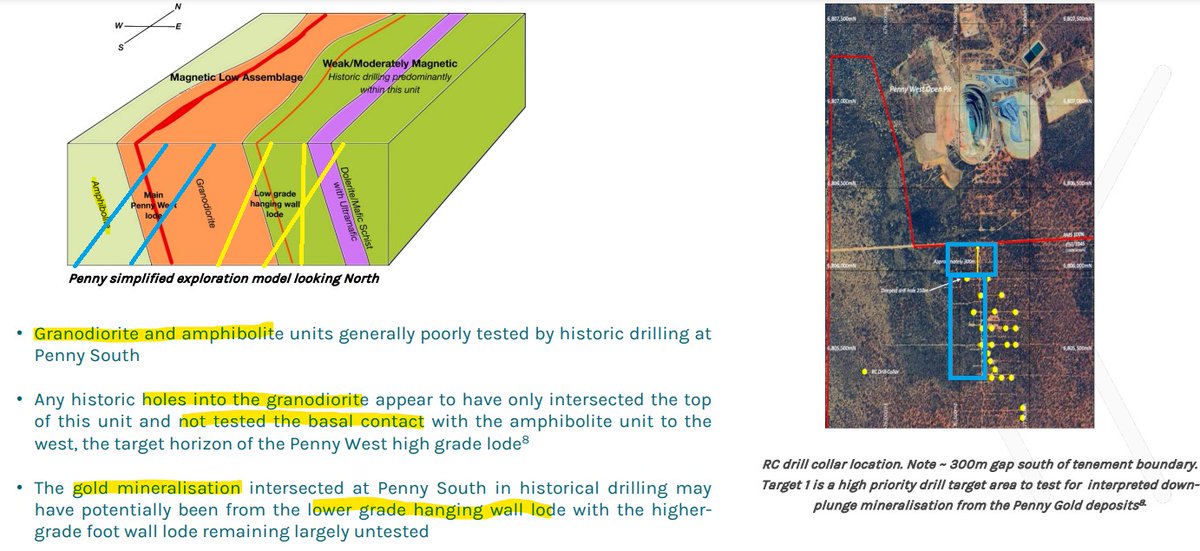

$SMX @StrataMinLtd gold micro cap i like.

Spectrum Minerals 2.0 - Penny West/South

Strata is drilling 'west' of historicals and to depth to ensure basal contact with amphibolite. i.e. where the high grade lode is.

3.5M MC - 1.5M cash

Q1 drilling

RVR

https://t.co/41JvdHDbax

@RawMinerals I do congratulate them on getting the loan.

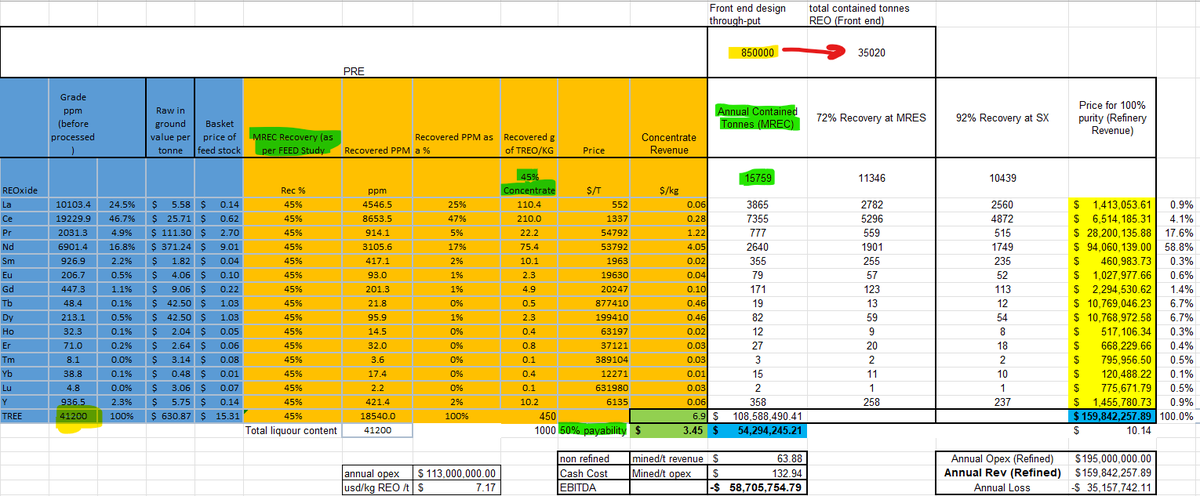

Obviously no one read the detail in the SS to realise the project is totally uneconomic IMO. My estimates are 80M USD loss p/a @ spot REO price.

Comparison to $VMM in below post by me on HC if interested.

https://t.co/7FFcz6arqr

$VMM $MEI just secured funding/grant via BNDES (Brazil Government).

With 1Bn to divi up across 10/11 projects they could each secure up to or around 100M each if evenly distributed.

More detail to come but not inconsequential.

$VMM Currently trades at 2% its NPV @ 36M MC

@Sustainabledud1 What am i missing?

4.12% TREO ~ 0.9% NdPr Head Grade

850,000tpa Front End design.

Total Input REO ~35,000

Concentrator recovery = 45%

Output REO ~ 15000 (no where near 20,000)

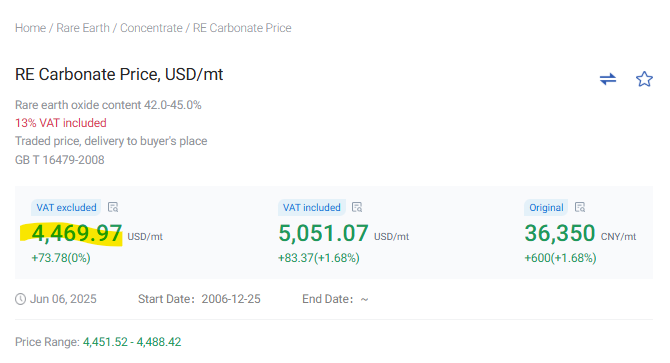

MREC is ~45% Conc level = 50% Payability (At best). 15000T @ $3.5 usd/kg = 50M USD Rev

Opex 110M USD

It's not too late to pull the plug on 'construction' for $PRE #Pensana.

OPEX = 113M USD

MREC production = 20000T

MREC value ~ 4400USD/T

Rev at spot REO ~ 88M USD

"technical" due diligence was performed.

Unfortunately (or intentionally) it never assessed economic viability.

@Contrarian_WA Unfortunately EBITDA of zero at current REO price. 240M usd opex and almost exactly 240M usd rev for the ndpr.

IMO SEG and Phos CR won’t cover the AISC cost on 1.2Bn USD.

$VMM and $MEI capex is less than 400M and still makes 20-40M USD on a AISC basis at current spot.

$ARU also not good valued at 450M MC

4400T NdPr

Nd Pr revenue 240M USD

Opex costs annual ~240M USD

1.2Bn USD capex for EBITDA of 0. Phos/seg credit won’t cover AISC

For comparison

$VMM (30M mc) and $MEI (260M mc) capex is 1/3rd the above both make 40-50M usd EBITDA at spot

@Spearhead_Cap Correct - Further strengthening the argument that even low HREO content deposits are still desirable as the HREO are more economically separable. Essentially what $LYC discovered with their SEG product.

$LYC makes it's second move partnering for ionic clay REO supply in Malaysia. That's notionally important as it validates the need for IACs for HREO.

IACs info in malay is opaque - but most look low grade and not viable. A couple of 1000ppm+ projects.

Very good for $VMM $MEI

$LYC finally admits they're looking at REO projects in Brazil.

https://t.co/iWIp7vGO7t

"Yes there are deposits there, yes there are deposits in Brazil. Yes we are looking at them"

$VMM $MEI $BRE the only ones that possibly make sense.

My opinion here.

https://t.co/7BdktAanMI