thanks for taking the time to reply and I will look forward to more of your thoughts when you have the time. I can address some pieces now, just from what you have shared. I'm going to italicize yours.

—

"You are assuming a settlement was made that will take care of former equity holders and are presenting it very definitively… That is NOT just “how it works”"

I am not assuming in the traditional sense, I am drawing this conclusion from the language in the Plan. specifically, the third-party release within the Plan accounts for Holders of Claims or Interests. in a previous post, I was able to conclude that this wording was a strategic move to preserve the rights of the shareholder (Holder of Interests) as the shares had to be cancelled so that the Plan could be Confirmed—Rule 1129(b).

note: they admit they had to go to (b) as the Plan could not be confirmed through 1129(a)(8) because some members of Class 6 were not cooperating.

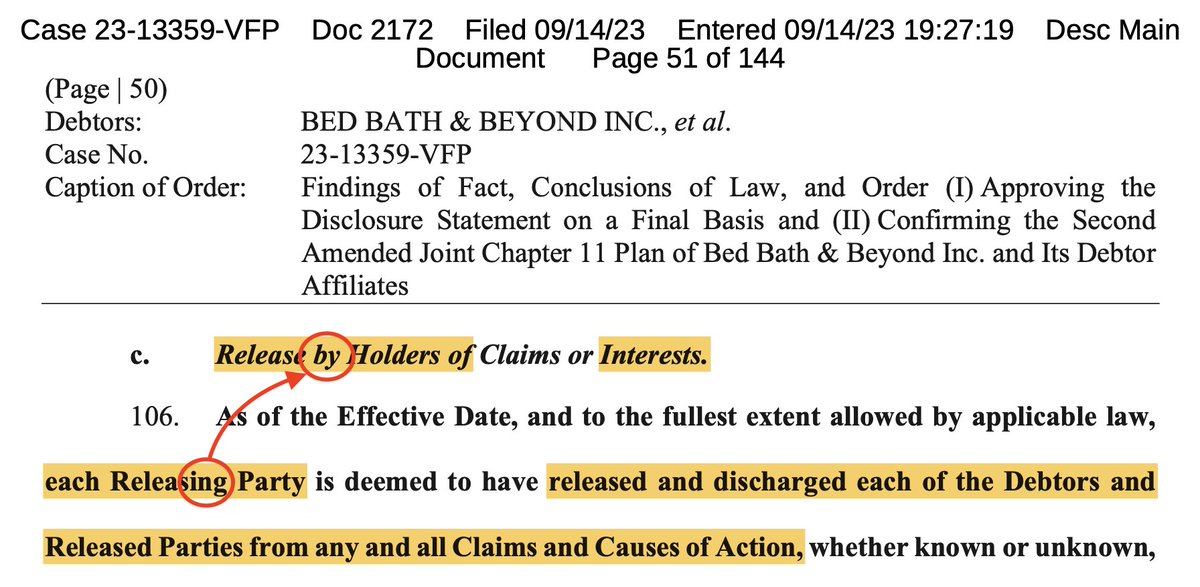

I know you laughed at me when I initially presented the idea that a Shareholder would be an involved party to the third-party release, but I feel that I have done a very good job to present my reasoning and conclusion of how I got there over the last month. I believe it is very clear that is the case and for anyone else reading, here is a simple summary:

now, as there was only one class of equity security, the Holder of Interests could only have Class 9 common stock. recall, you cannot give preferential treatment within a Class, so the only possible conclusion is that SOMEthing is coming to Class 9 in exchange in connection with the third-party release.

I am presenting it definitively only because the Law is clear—you cannot discriminate within a Class, or give preferential treatment within a Class. the Plan for Bed Bath even ensures to confirm that this discrimination did not occur:

and look, even language to cover their bases for Class 6's alternative and negotiated recovery (red underline).

reading that statement, we again see the reference to Interest—note the Capitalization. they are clear, the third-party release did not only benefit the one, singular shareholder who held the claim.

my other posts about the releases, specifically the U.S. Trustee objection to the Confirmation of the Plan, go into great detail about the handling of Class 9.

—

"and other solutions will not ‘take far too long and cost far too much.’"

I made this statement simply because that was the statement provided by the plan man in regards to your motion.

—

"I do not accept these as black and white determinations as they are being continually presented lately (by many, not trying to single out this one specifically). I do not believe tax paying American citizens or any shareholders of a publicly traded company should “just accept it” either."

that is a fair opinion and your right to feel that way. personally, I do believe that this thinking is leading your actions. you should recognize that this is an emotional expression and I further believe this emotional driver is impacting your pursuit in a way that is not beneficial to you.

to the "just accept it" statement, although I can sympathize with your frustration what you have said is somewhat beautiful because it really is that simple—we have to just accept it. the Law is structured in a way where there is no other possible outcome, especially at this stage. we are not going to rewrite the Bankruptcy Code.

and guess what, thanks to that very Bankruptcy Code and 1123(a)(4), shareholders of Bed Bath will be just fine.

—

I think am getting a better understanding of what your intentions are, at least from what I am reading. I believe that you are attempting a righteous pursuit and feel that settlement and compromise should not be on the table in exchange for what had transpired. I can respect that, but respectfully, I do believe that this is a flawed approach.

reason one: this Company is in the jurisdiction of the Court and the significant preference and "skew" in the Law when it comes to Chapter 11 is expediency and re-emergence, where possible. these are powerful factors that you cannot overcome. the Law is the Law.

reason two: as an offshoot of reason one, this Company is not in a position to make the righteous effort. who will pay for the attorneys to (allegedly) hold JP Morgan accountable? BNY Mellon? these are colossal entities. they have armies of litigation attorneys. the righteous process could and would take over a decade, because the primary legal strategy for the (alleged) defendants would be delay, stall, accrue expenses, countersue for costs, etc. all while requiring the Bed Bath side to be represented by competent, evenly-matched attorneys the entire time. who would pay for it?

also, given that Bed Bath is in the jurisdiction of the Court, with a DIP loan that has been offered by a creditor, this presents a complication of its own—the creditor is a publicly-traded Company itself, accountable to its own shareholders. it needs to fulfill its commitment to them, by having the DIP repaid. now, this is not a good reason on its own, but again it is the reality. no creditor will allow a decade-long window of time to "do the right thing."

Bed Bath is not the righteous venue. I know of another Company that is, however. I have been on that battlefield since 2020, first educating myself and then participating with my own capital since January 2021.

Bed Bath, given the situation it is in, is a ripe candidate for a compromise. we don't even know the amount of money coming to the estate in exchange for the debtor release.

if you take your enthusiasm for accountability, apply it to how bad the crime could have been (we don't even know the full extent!), trust the experts uncovering it got to the core,—then can you imagine the potential?

can you even imagine what you could do with a significant distribution of new capital (I'm not even talking about warrants or potential new equity) on a righteous battlefield? (this is not financial advice of any kind).

—

fundamentally, I trust in Ryan Cohen. I cannot fathom him being treated how he was by the Bed Bath board and then just walking away from what he saw.

no. in fact I resolutely believe the complete opposite. I believe that a man who was turned down by over 100 investors/venture capitalists for Chewy and never lost conviction in himself, his idea or his goal, presenting his dream for a pet retailer with the same enthusiasm on the 101st attempt as he did on the first, would in fact turn around and hold anyone possible at Bed Bath with extreme accountability, to the fullest extent possible, given the situation.

have you forgotten the enormous elephant-sized pile of trouble the former Board is in? there will be accountability.

even better, there will be this accountability plus proceeds of release settlements. and soon.

I trust Ryan Cohen. you're on the Class 9 rollercoaster my friend and guess what, you're getting the fruit of RC's labour like everyone else.

I respect your position if you disagree. I am not uncertain of mine.

$BBBY #BBBY $BBBYQ #BBBYQ

“I will no longer be complicit in genocide.”

— Aaron Bushnell, US Air Force

Aaron passed away after setting himself on fire outside of the Israeli Embassy in Washington DC protesting against the Gaza genocide committed by Israel and aided by the US Govt.

$BBBYQ stock ticker now shows again on IBKR.

I'm sure this happens to every delisted ticker /s

The bonds reappeared the first week of November 2023.

🔁Repost, because glitch better have our money