Sen. Cynthia Lummis: "The next window for digital asset legislation after this Congress is likely 2030. Until then, developers remain exposed with no legal protections."

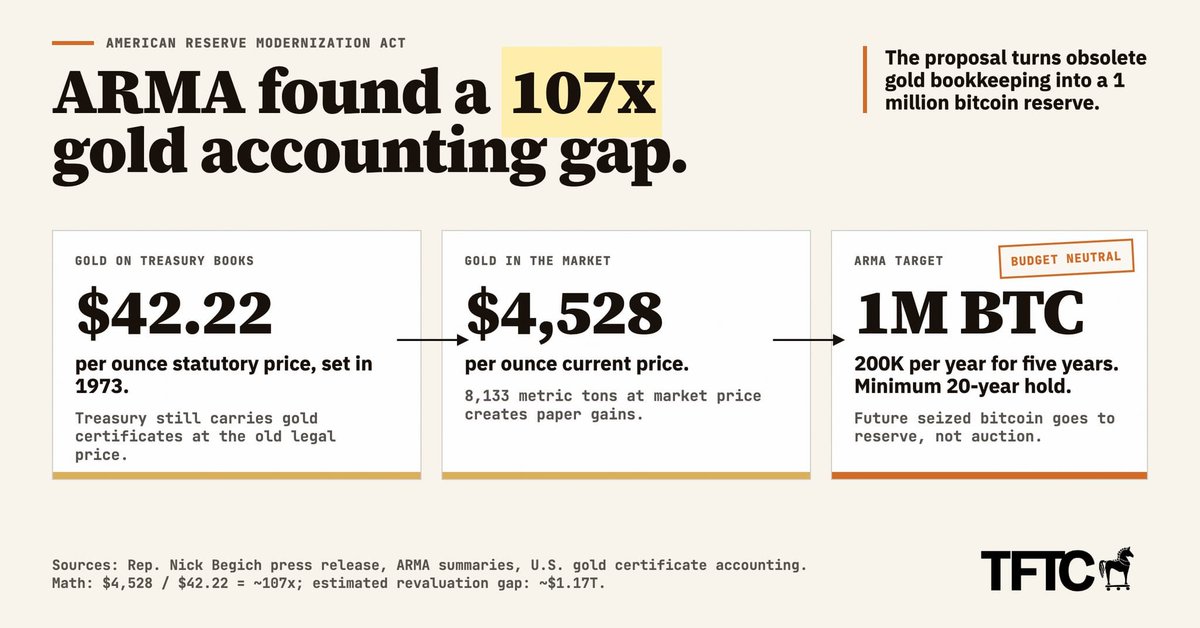

A new bill in Congress would fund a 1 million bitcoin reserve by closing a 107x accounting gap on U.S. gold.

Rep. Nick Begich (R-AK) and Rep. Jared Golden (D-ME) introduced the American Reserve Modernization Act of 2026 (ARMA) on Wednesday with 21 cosponsors.

The bill would authorize the U.S. Treasury to acquire up to 200,000 bitcoin per year for five years. It is a rebranding of the original BITCOIN Act co-introduced by Begich and Senator Cynthia Lummis, and would codify Trump's March 2025 Strategic Bitcoin Reserve executive order into permanent law.

The bill classifies bitcoin as a "Tier 1" strategic reserve asset, putting it on the same legal footing as gold. All acquisitions must be budget-neutral. The funding mechanism is revaluing Federal Reserve gold certificates from their statutory price of $42.22 per ounce, set in 1973, to current market prices. At today's gold price of $4,528, that revaluation would unlock over $1.17 trillion in paper gains on the government's 8,133 metric tons of gold without new taxpayer debt.

The bill ends the practice of auctioning seized bitcoin. All future seizures go directly to the Strategic Reserve instead of being liquidated by the U.S. Marshals Service. Bitcoin in the reserve would be held for a minimum of 20 years, with the only exception being sales to reduce the national debt.

Federal custody standards include geographic distribution of private keys across air-gapped facilities, multi-signature governance requiring authorization from the Treasury, the Fed, and an independent third agency, and investment in quantum-resistant cryptographic upgrades. This is the most technically detailed bitcoin custody language ever written into a Congressional bill.

The U.S. government has been carrying gold on its books at $42.22 an ounce for over 50 years while the market price surged past $4,500. ARMA would close that gap and use the difference to buy an asset that cannot be debased. Whether it passes is one question. That it exists with bipartisan support and 21 cosponsors on day one is the signal.

AOC brought jars of brown water to a congressional hearing this week, saying they came from wells near Meta's data center in Morgan County, Georgia. The clip went viral.

Here is what the data actually says.

Data centers use water primarily for cooling. A typical facility uses about 300,000 gallons per day. Large hyperscale facilities can use up to 5 million gallons per day, roughly the water needs of a town of 50,000 people. That sounds like a lot until you zoom out.

All US data centers combined account for somewhere between 0.1% and 0.4% of total national water withdrawals, depending on the year and whether you count indirect water from electricity generation. Agriculture accounts for 70-80% of water withdrawals in arid states. In Arizona alone, agriculture uses 86% of total water. The entire industrial sector, which includes data centers, sits at around 8%. Golf courses alone use significantly more water nationally than all data centers combined.

Data centers also generate roughly 50x more tax revenue per unit of water consumed than golf courses. Nobody is holding up jars of brown water at congressional hearings about golf course irrigation.

The technology is also moving fast. Closed-loop cooling systems can reduce freshwater use by up to 70%. Air cooling and immersion cooling can nearly eliminate water use entirely. The industry is trending toward less water-intensive designs with every new facility built.

Now, the Morgan County situation specifically. Residents near Meta's data center campus say their well water turned brown after construction began, which included forest clearing and blasting. AOC visited the area and brought the water samples to the hearing.

Meta commissioned a third-party groundwater study that found no connection between the well issues and Meta's operations or construction. The EPA's Assistant Administrator for Water said she was aware of complaints about data center water usage but had not received reports about quality impacts. She agreed to look into it. No investigation has confirmed a causal link.

Construction blasting near private wells can disturb sediment and temporarily affect water quality. This is a known issue with large-scale construction of any kind, not unique to data centers. Whether Meta's construction specifically caused these well problems is an open question that has not been answered.

The broader framing, that AI data centers are a national water crisis, does not hold up against the numbers. At less than half a percent of national water withdrawals, data centers are a rounding error compared to the sectors that actually drive water stress. The real concern is local: a single hyperscale facility dropping into a small rural county can strain a local water system that was not built for that kind of demand. That is an infrastructure planning problem, not an AI problem.

Projections from Ceres show that data center cooling water demand could increase by 870% as more facilities come online. That growth rate deserves attention. But the starting base is so small that even an 870% increase would still leave data centers well below agriculture, manufacturing, and thermoelectric power generation in total water use.

The conversation about data center water should be about local infrastructure planning and modern cooling technology, not viral clips of brown water with no confirmed cause.

He may not have done extremely well in NASCAR, but this man Travis Pastrana can drive the wheels off of anything. I love watching these videos of his. I just want to see the tires before and after! 🛞🔥🔥🔥

This guy quit his corporate job and opened a business where he:

- Is on track to make $100K / year profit

- Works an hour a week

The whole business runs on $40/month software.

His 14-year-old helps clean on Saturdays.

It's 24/7 door access, so he doesn't even have to be there.

What in the world is this unicorn?

A single bay golf simulator with a membership model.

Members pay $175 to $325 a month to practice their swing in a private space.

He opened with 5 friends as his first customers. Within 3 months he hit 15 members and broke even.

Now he's at 28 members after 6 months. Max capacity is 40 per bay.

In this episode Jay breaks down:

- Exactly how he validated demand before opening (talked to 10 friends, 5 committed immediately)

- His three-tier pricing model and why unlimited is only $325/month

- How he negotiated his lease to not pay rent until he opened

- Why he's deliberately not marketing yet (he wants to learn the business first)

- His plan to scale from 1 to 5 locations in the next couple years

This one is so dang good!

I love this stuff.

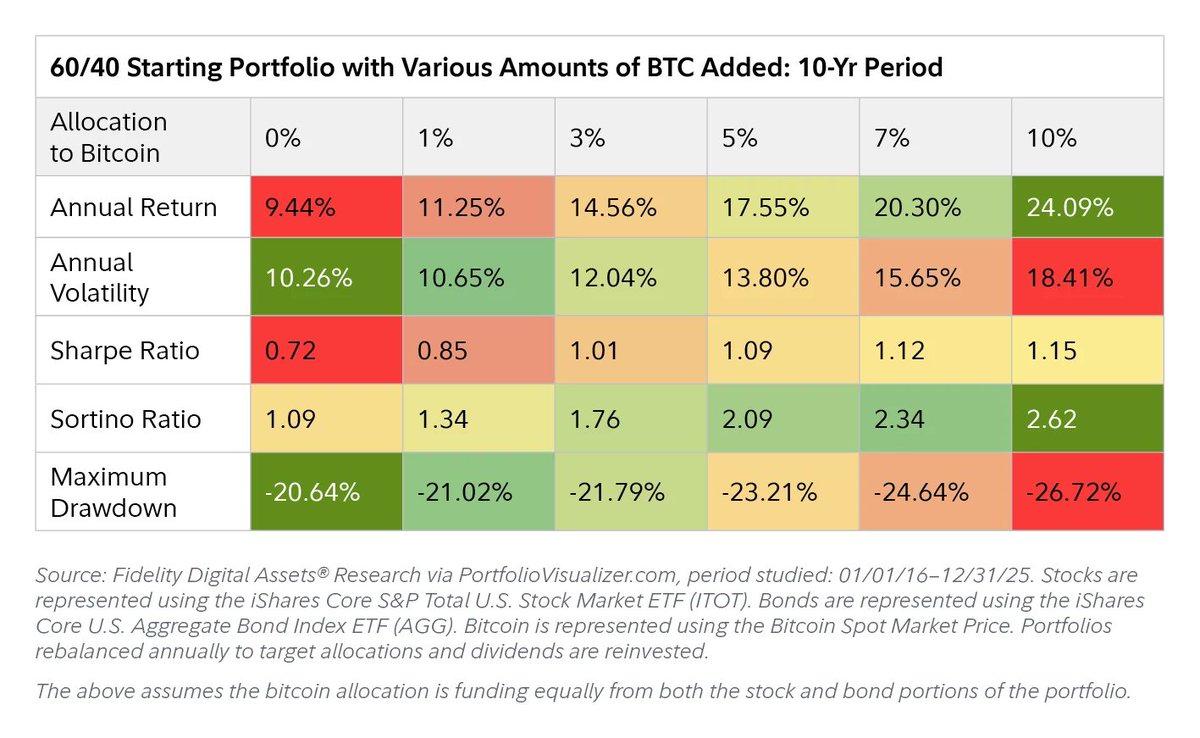

Fidelity Digital Assets says the most important portfolio decision isn't how much bitcoin to buy. It's going from zero to any.

Their data shows that adding just 1% bitcoin to a traditional 60/40 portfolio produced 30% more compounded value over the study period, increased risk-adjusted returns by 20%, and only increased maximum drawdown by 0.27%.

The first 50 to 100 basis points of bitcoin allocation delivered the most efficient improvement in portfolio performance. After that, returns scale but so does volatility. The initial move off zero is where the math is most lopsided.

The corporate treasury findings are even more striking. A 1% bitcoin allocation to a standard corporate bond portfolio more than doubled returns, actually reduced overall drawdown, and increased the Sharpe ratio by over 40%.

For companies sitting on cash reserves earning next to nothing in a negative real rate environment, Fidelity is saying the risk of holding zero bitcoin is greater than the risk of holding some.

The report also found that where you source the allocation from barely matters. The difference between funding it from stocks versus bonds was 0.11% in returns and 0.13% in volatility for a 1% position. The decision that moves the needle is binary: zero or not zero.

Fidelity manages over $5 trillion in assets. This isn't a bitcoin company talking its book. It's one of the largest asset managers in the world telling institutional clients that the data favors allocation, and that the biggest risk in a portfolio may be having none at all.

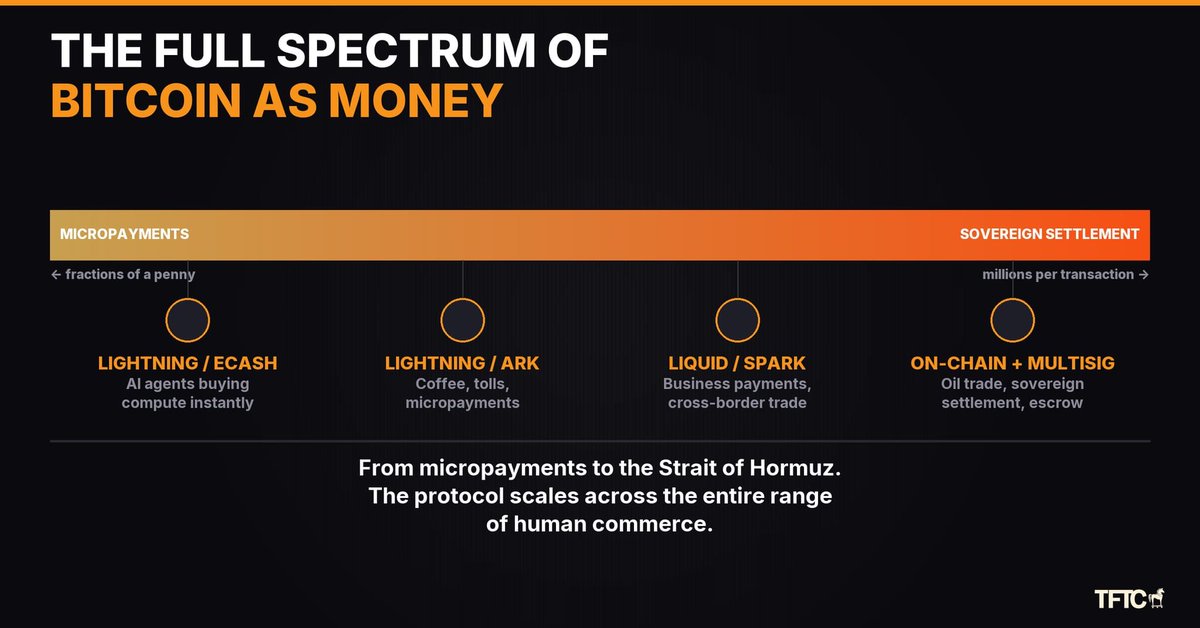

Bitcoin covers the full spectrum of medium of exchange.

At one end, AI agents buy compute for fractions of a penny over Lightning. At the other, sovereign nations settle geopolitical transactions on-chain with multisig escrow and thermodynamic finality backed by over 1,000 EH/s of hashrate.

Iran demanding bitcoin tolls at the Strait of Hormuz isn't "bitcoin finally has a medium-of-exchange use case." Bitcoin has always been a medium of exchange. Hormuz just revealed where on the spectrum things get most interesting.

The endgame is bitcoin integrated into international oil trade. Buyer puts bitcoin in multisig escrow. Oil gets delivered. Escrow releases to the seller. On-chain settlement provides the irreversible, verifiable finality that high-value international trade demands. No intermediary can freeze it. No stablecoin issuer can blacklist an address after the fact. The base layer is neutral by design.

This isn't prescriptive. It's descriptive. Bitcoiners have said for over a decade that geopolitical counterparties who can't trust each other will need a Schelling point: a neutral reserve settlement protocol. That's playing out right now.

From micropayments to the Strait of Hormuz, the protocol scales across the entire range of human commerce. That's not a theoretical framework. It's happening.

Kid just SMOKED a CNN reporter outside of Artemis II launch:

CNN: "Why do you want to be here?... Why do you love being a part of history?

Kid: "We're going back to the f*cking moon, that's why!" 🤣

Jack Mallers: "Rubio says Iran war to last weeks, not months, with no US ground troops needed. Okay, well then what the f**k is this? What's the letter to the Marines saying, prepare your family, we're going to war?"

"Somehow, no matter who's the president, we're in conflict. Bush, conflict. Obama, conflict. Biden, conflict. Trump, conflict. Spend, spend, spend. Debt, debt, debt. Lie, lie, lie. War, war, war."

"This isn't a blue thing, this isn't a red thing. This isn't a left thing, this isn't a right thing. This is, government's gotten too big, they have a monopoly on printing money, they can finance these things, they can steal our wealth through dilution, through inflation."

The median home has tripled in price since 1980 after adjusting for inflation. Wages over the same period are up 18%.

That one gap explains more about the economy than any jobs report or GDP number ever will. Housing didn't become unaffordable because people got lazier. It became unaffordable because asset prices outran wages by a factor that compounds every single year.

In 1980, the median home cost 3.9 times the median household income. Today it costs 5 times. A 20% down payment went from $12,740 to over $83,000. The paycheck that's supposed to cover it barely moved in real terms across 44 years.

This is what currency debasement looks like up close. The dollar has lost over 70% of its purchasing power since 1980. That doesn't show up on a grocery receipt all at once. It shows up over decades in the growing distance between what people earn and what things cost.

The generation that bought homes at 3.9x income is telling the generation facing 5x income to work harder. The math doesn't back that up.

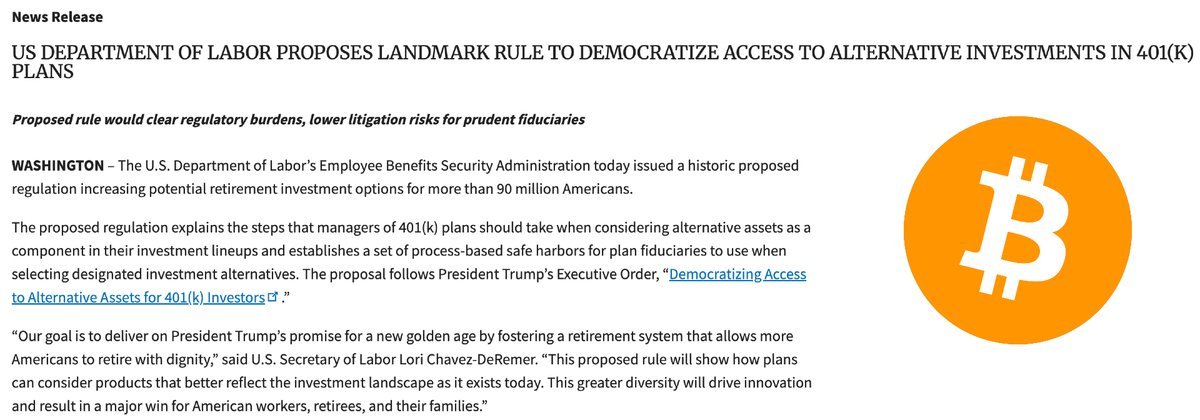

The U.S. Department of Labor just proposed a rule that would open 401(k) retirement plans to alternative assets, including bitcoin.

There are technically no existing restrictions preventing 401(k) plans from including bitcoin. The problem has always been legal risk. Plan fiduciaries, the people responsible for managing retirement investments on behalf of employees, have avoided bitcoin because they feared being sued or challenged for offering volatile or unconventional assets.

The proposed rule changes that by creating what the Department calls "process-based safe harbors." If a fiduciary follows the outlined process for evaluating an alternative asset, considering its performance, fees, liquidity, valuation, and complexity, they're legally shielded from liability. That removes the single biggest barrier that has kept bitcoin out of the $11 trillion 401(k) market.

Labor Secretary Lori Chavez-DeRemer framed it as delivering on Trump's promise for "a new golden age" by building a retirement system that "better reflects the investment landscape as it exists today."

The rule covers more than just bitcoin. Real estate, private equity, and other private-market assets would all fall under the same framework. But the bitcoin angle is the headline for a reason: this is the first time a federal agency has moved to provide explicit legal cover for retirement plan managers who want to offer bitcoin exposure to tens of millions of American workers.

The rule is now in a 60-day public comment period before it can be finalized.

Put this alongside today's other developments, Morgan Stanley filing for a spot Bitcoin ETF at the lowest fee in the market, the Mined in America Act creating a pipeline for miners to sell bitcoin to the government, and Fannie Mae recognizing bitcoin-backed mortgage products. The infrastructure for bitcoin's integration into the traditional financial system is being built in real time.

Square just auto-enabled Bitcoin Lightning payments across 4 million U.S. merchant terminals. No opt-in required. Sellers receive USD by default.

This is the most significant Bitcoin payments infrastructure move since the Lightning Network launched. Every coffee shop, barber, and food truck on Square can now accept sats over Lightning at zero fees through 2026.

Jack Dorsey's Block didn't ask for permission. They flipped the switch.

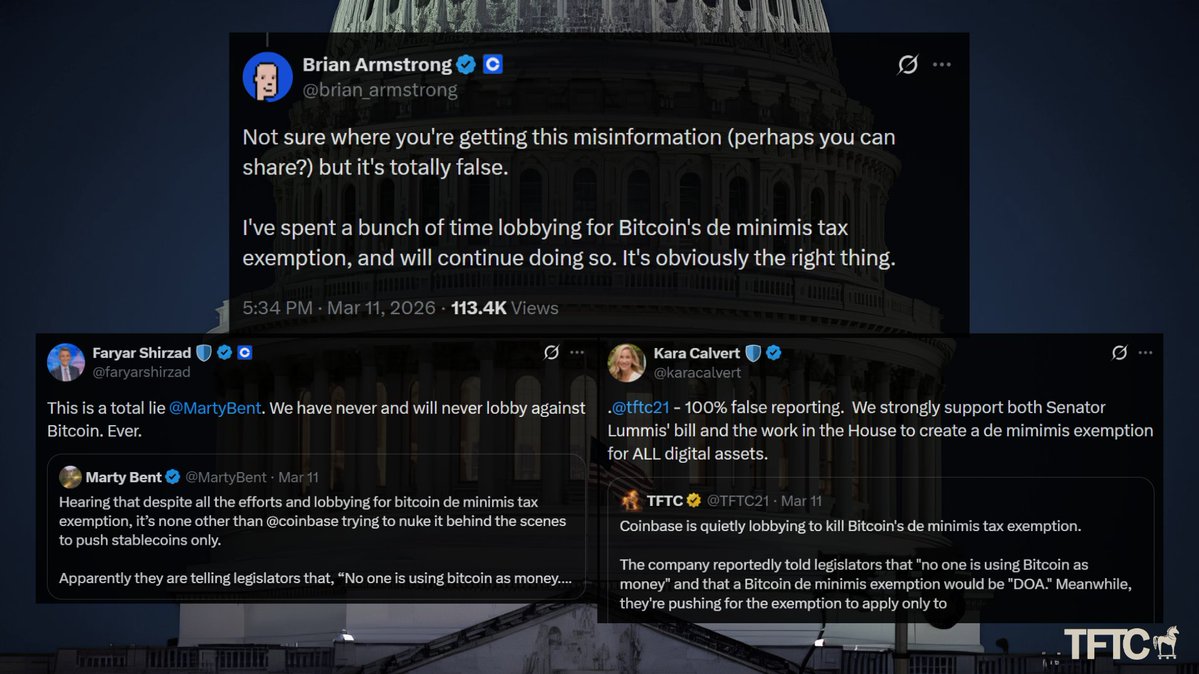

Folks, we told you this was coming, and today the mask is fully off.

A couple weeks back we reported, based on solid sources, that Coinbase was quietly lobbying to kill a real de minimis tax exemption for Bitcoin while pushing one that applied only to stablecoins like USDC. We laid out the clear incentives in our deep dive. Coinbase made 1.35 billion dollars in stablecoin revenue last year, up 48 percent year over year, almost entirely from yield on the Treasuries backing USDC.

A proper Bitcoin de minimis would let people spend sats on everyday purchases without triggering taxable events on every transaction. That directly competes with their centralized yield machine. We called it what it was. Policy that protects Coinbase’s float rather than advancing neutral Bitcoin adoption.

Brian Armstrong pushed back hard. He called our reporting totally false and misinformation while insisting he was personally lobbying for Bitcoin de minimis. Some accused us of lying or spreading rumors. We stood firm. We offered to have Brian on the TFTC podcast to clear the air. We waited.

Now the latest draft from Reps. Horsford and Max Miller on the updated PARITY Act framework has dropped. It confirms exactly what we warned about. It gives a de minimis exemption to stablecoins but leaves Bitcoin out entirely. It keeps the punishing double taxation on Bitcoin mining fully intact while carving out relief for passive validation, basically staking. This is not an oversight or sloppy drafting. It abandons any pretense of technology neutrality and deliberately picks winners. Dollar-pegged stables and staking get the breaks, while actual Bitcoin usage as money and Proof-of-Work mining get kneecapped.

Without de minimis for Bitcoin, every small Lightning payment or sat transaction still forces cost-basis tracking and IRS headaches. Paying your plumber in sats or grabbing lunch with Bitcoin remains a taxable event. Stablecoins, being pegged and low-volatility, get an exemption they barely need. The real beneficiary is protecting that massive USDC reserve float and the yield it generates.

Meanwhile, American Bitcoin miners, already operating in one of the toughest, most capital- and energy-intensive industries, face continued double taxation while staking gets a pass. That is not neutral policy. It is industrial policy against domestic Bitcoin mining at a time when we should be leaning into energy abundance and securing the hardest monetary network.

The Bitcoin Policy Institute is releasing a full statement soon, and we fully back the call for strong community pushback. Every Bitcoiner needs to contact their reps and make it politically radioactive to sideline Bitcoin while handing carve-outs to stables and staking. This language slows real adoption, entrenches custodians, and weakens American Bitcoin infrastructure.

We weren’t lying. Our sources weren’t lying. The draft proves the reporting was on target. Those who rushed to call it misinformation owe the community some honest reflection.

Brian, if you’re still open to that conversation, the invitation stands. Come on the podcast. No spin, just walk us through how this draft lines up with your stated support for Bitcoin de minimis. The mic is warm.

This fight isn’t over. Bitcoin doesn’t need permission, but bad policy can delay sovereign adoption and punish the miners securing the network. We’re here to protect the protocol and the right of individuals to use sound money without turning every transaction into a compliance nightmare.

Stay sovereign. Stack sats. Use Bitcoin as money anyway. Call your reps today.

Five years ago, telling your mortgage lender you owned Bitcoin was a red flag. Today, Fannie Mae is backing home loans where Bitcoin IS the down payment.

That's not a crypto startup. That's the U.S. government's mortgage backbone treating Bitcoin as collateral with the same protections as a conventional 30-year home loan.

Here's what changed: 41% of American families fail to buy a home because they can't scrape together the cash for a down payment. Not because they're broke. Because their wealth is locked in assets they'd have to sell, triggering capital gains, paperwork, and a tax bill that eats the down payment itself.

Bitcoiners know this trap better than anyone. You're sitting on life-changing wealth and the system punishes you for trying to use it.

This product eliminates that wall. Pledge BTC or USDC as collateral, receive a loan for the down payment, keep your Bitcoin, pay no capital gains. Rate is 0.5 to 1.5 points above standard depending on borrower profile.

The key detail: no margin calls. No collateral top-ups. If Bitcoin drops in value, the mortgage terms remain unchanged and no additional collateral is required. Market movements alone never trigger liquidation. The only liquidation risk is a 60-day payment delinquency, same as any conventional mortgage.

This is how billionaires have operated for decades. Borrow against assets, never sell. Private banks built empires on this model for the ultra-wealthy. The difference now: it's available to anyone holding Bitcoin on an exchange.

The real story isn't the product. It's what Fannie Mae's involvement signals. A government-sponsored enterprise formally underwriting Bitcoin-collateralized debt means the U.S. housing system no longer views Bitcoin as speculation. It views it as wealth. That's a classification shift that took 15 years to happen and will be impossible to reverse.