🚨 2.5 BILLION $DOGE Just Got YANKED Off Robinhood 🪶

5 huge transfers of 513 million coins each!

($245M total)

1 of the biggest single-day liquidity drains in Dogecoin history.

Big holders moving it straight into cold storage? That’s diamond hands holding for the future 💎

Congress has spent the better part of half a decade trying to pass a framework to onshore the future of finance.

It is time for @BankingGOP to hold a markup and send the CLARITY Act to President Trump’s desk.

Senate time is precious, and now is the time to act.

VeChain is doubling down on real-world utility.

@vechainofficial continues to focus on enterprise adoption, staking participation, and real-world applications, rather than chasing DeFi volume.

-- 9–10.7B $VET staked after the StarGate launch

-- ~94% growth in active stakers in the first 3 months

-- VTHO emissions cut, with deflationary pressure appearing in some periods

-- 5M+ ecosystem users and 350+ apps built

-- 5.2M+ wallets earning B3TR rewards weekly

-- VeBetter pushing X-to-Earn real-world actions

-- EU MiCA compliance positioning VeChain for institutional partnerships

VeChain’s strategy is clear: build infrastructure for real-world use cases first, and let the ecosystem grow around it.

VeChain ($VET) is the most quietly used blockchain in the world.

Price today: $0.0067

ATH: $0.2782

Down: -97% from peak

Who is actually using it RIGHT NOW:

— Walmart China — food safety tracking

— BMW — car part verification

— PwC — audit and compliance

— DNV — sustainability certifications

— 940,191 smart contracts deployed

$0.0067 with Walmart as a client.

You decide if that is undervalued.

Follow @CoinIntelOrg

https://t.co/uLp9Znvki9

#VeChain #VET #CryptoGems #CoinIntel

🚨 Here is the full 40 minutes of my crew and I exposing California fraud, Minnesota was big but California is even bigger... We uncovered over $170,000,000 in fraud as these fraudsters live in luxury with no consequences. Like it and share it, the fraud must STOP.

We ALL work way too hard and pay too much in taxes for this to be happening. These fraudsters have been able to defraud American taxpayers for years without any pushback from the public and politicians.

It is time to EXPOSE IT ALL and end America's fraud crisis.

For the record.

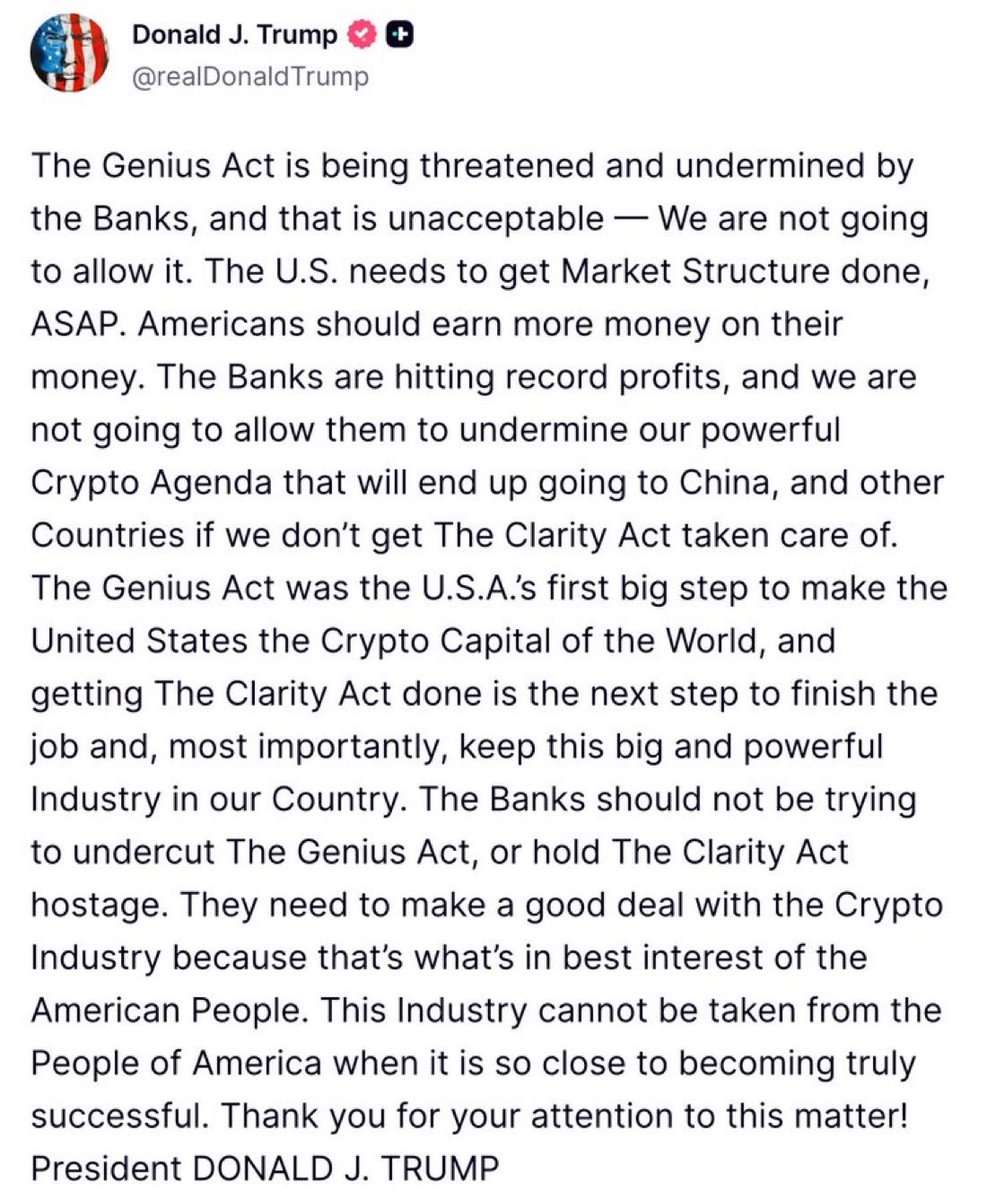

Jamie Dimon says he wants a “level playing field” for stablecoins. What he really wants is to make sure nobody can offer you a better deal on your own money than tradtional banks can. The president is right to call the banks out on this.

We’ve seen this before. In the 1970s, money market funds started paying real yields while banks were locked under deposit caps. Banks cried “unfair” and “unsafe,” lobbied furiously, and lost. Policymakers chose competition over protection; savers got paid, and banks had to adapt instead of suffocating the threat.

Today’s script is the same, just with better technology. Stablecoin issuers now operate under licensing, 1:1 high‑quality reserves, liquidity and risk rules, audits and strict AML standards. This is not the Wild West. Yet Dimon still talks as if they exist with “no reserves, no compliance, no oversight.” He’s not describing reality; he’s describing a story that justifies shutting down a rival funding system.

The Clarity Act is the real battlefield. On paper, it’s about integrating crypto into U.S. market structure. In practice, the big banks are fighting to ensure that anything that looks like a deposit with yield must either become a bank product or be regulated into irrelevance. “Level playing field” in their vocabulary means: everyone wears the bank straitjacket, or no one plays.

Why? Because yield‑bearing stablecoins blow up the quiet cartel behind record profits. Banks live on deposits that pay close to nothing even when risk‑free rates are high. They earn a clean spread and interest on balances parked at the Fed, while passing little of it through. Savers get crumbs; banks get the margin; inertia does the rest. A credible, regulated stablecoin that passes through money‑market yields detonates that racket: with a few clicks, your cash can leave the cartel.

The president’s critique goes straight at this arrangement: Americans should “earn more money on their money,” and banks should not be allowed to undermine laws designed to make that possible or to stall a market‑structure bill so the whole “powerful Crypto Agenda” decamps overseas. He’s not attacking banking; he’s attacking a model that treats low‑yield deposits as an entitlement and regulation as a weapon.

Crypto‑native firms, for all their flaws, behave like they live in a real market: they build new instruments, disclose, and pay up to attract capital. The banks build talking points and hire lobbyists. Stablecoins don’t just threaten their funding; they threaten their chokehold on payment rails and transaction data.

Call this debate what it is: not a fight over “safety,” but a fight over whether a protected deposit cartel gets veto power over technologies that finally let savers earn something closer to the risk‑free rate. In the 1970s, policymakers chose competition.

In the 1970s, banks were forced to stop hiding behind regulation and compete. If Jamie Dimon wants a level playing field, he should stop complaining and start doing the same.

The “Big Banks”—the very institutions that have held a monopoly and screwed their customers for years, offering near-zero yields on retail Money Market Accounts while crushing low-balance accounts with exorbitant fees—are now doing everything they can to block the Crypto industry from offering real benefits, perks, and rewards on their platforms.

They are the greatest hypocrites and are in mass panic given they know they are losing the digital finance race! @worldlibertyfi