Aeroflex

Yesterday (July 6, 2026), the prominent semiconductor research firm SemiAnalysis published claiming that Nvidia's highly anticipated next-generation, liquid-cooled rack architecture—codenamed Kyber NVL144—is facing a massive 12-month delay, pushing its release from 2027 out to 2028.

(Note: Nvidia issued a short statement yesterday denying the delay, claiming their "roadmap is intact,).

Here is why this is directly crashing cooling stocks:

The Bottleneck: The delay isn't caused by the AI chips themselves. It is caused by a physical manufacturing failure in the massive circuit boards (the PCB midplane) that route signals inside these ultra-dense liquid-cooled cabinets.

the report also stated Nvidia has outright cancelled a backup rack design (the NVL72x2) because major cloud providers rejected the awkward architecture.

The Direct Impact on Aeroflex (and the Cooling Space)

The Pipeline Pushback: Aeroflex manufactures Liquid Cooling SFN skids—the exact plumbing required to cool these ultra-dense AI racks. If Nvidia's next-generation liquid-cooled infrastructure is delayed by a full year, it means Big Tech hyperscalers will delay their data center upgrades. Consequently, the near-term order book for every cooling component supplier globally just got pushed back.

Here is how Aeroflex's global peers reacted to the rumor yesterday:

Ibiden (Japan): One of Nvidia's largest PCB and advanced packaging suppliers. The stock crashed as much as 10%.

Kingboard Laminates (Hong Kong): A major supplier of circuit board materials. Tumbled 18%.

Taiwanese Hardware Hub: The entire ecosystem took a hit. Elite Material plunged ~10%, Nan Ya PCB dropped ~9.3%, and Kinsus Interconnect fell 8.4%.

#Apollo Micro Systems: ₹3,322 Cr Fund Raise Announced

Apollo Micro Systems has announced one of the largest fund raises in the Indian defence sector, aimed at accelerating its next phase of growth.

🔹 Total Fund Raise: ₹3,322 Cr

✅ Preferential Equity Issue

• ₹951 Cr through 2.28 Cr equity shares

• Issue Price: ₹416.60/share

• 55 non-promoter investors participating

✅ Convertible Warrants

• ₹2,371 Cr through 5.69 Cr warrants

• Issue Price: ₹416.60/warrant

• 25% payable upfront, balance on conversion within 12 months

🏛️ Strong Institutional Participation

• Tata Mutual Fund

• Saint Capital Fund

• Nautilus Private Capital

• Maestro Emerging Fund

• Robust Knights Fund

• Cullinan Opportunities Fund

• Multiple domestic & global institutional investors

💪 Promoters Show Confidence

Promoters are subscribing to 2.61 Cr warrants worth over ₹1,087 Cr (on full conversion), reflecting long-term commitment to the company's growth.

🎯 Why This Matters

✔ Massive capital available for expansion

✔ Strengthens balance sheet for future growth

✔ Supports defence manufacturing, R&D and capacity expansion

✔ Institutional validation at ₹416.60/share

✔ Positions Apollo to bid for larger defence programs

⚠️ Key Watchpoints

• Deployment of ₹3,322 Cr

• Return on capital generated

• Execution of expansion plans

• Future order inflows

• Impact of dilution after conversion

Overall, this is a landmark fundraising that significantly strengthens Apollo Micro Systems' financial position. The key factor for shareholders will now be management's execution and its ability to convert this capital into sustained revenue, profit and order book growth.

#ApolloMicroSystems #Defence #DefenceStocks #MakeInIndia #StockMarket #Investing #IndianDefence

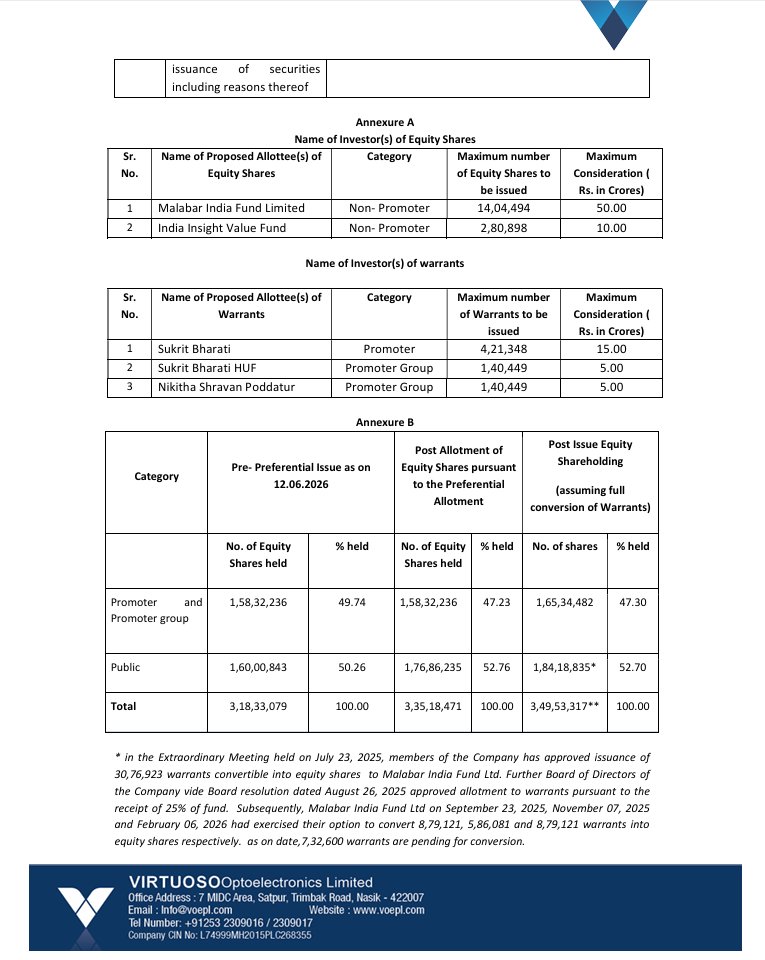

Virtuoso Optoelectronics (VOEPL) is raising ₹85 crore through a preferential issue.

- Malabar India Fund – ₹50 crore

- India Insight Value Fund – ₹10 crore

- Promoter group participation – ₹25 crore through warrants

Institutional investors are bringing in fresh capital while promoters are also participating alongside them.

Post allotment and warrant conversion, the promoter stake is expected to remain broadly stable around 47%, while growth capital comes into the business.

#VirtuosoOptoelectronics #VOEPL #PreferentialIssue #ElectronicsManufacturing #EMS #MakeInIndia #SmallCaps #IndiaInvesting #StockMarketIndia

@AethosWealth

Here’s a list of stocks with massive/significant FII holding increases over the last 3 years (or sharp recent surges), based on Trendlyne & shareholding data (as of Mar 2026 qtr):

1. Five-Star Business Finance: 8.7% (Jun’23) → 48.5%

2. Sammaan Capital: Sharp jump to 46.2% (+21% in latest qtr)

3. Home First Finance: Strong rise to ~45.7%

4. MCX: Steady buildup to 26.1%

5. 360 ONE WAM: Highest at 63.3%

6. Redington: 61.5%

7. Paytm: 49.4%

8. YES Bank: Elevated ~46%

9. BlackBuck: +~21% in 1yr to ~32%

10. IDFC First Bank: Notable rise to ~36.5%

Data shifts quarterly—check latest filings. Which ones stand out to you?

If any country is considering buying the Chinese HQ-9 air defense system, it should watch what happened to it today

5 HQ-9 have been destroyed in 1 year

1 by India during ops against Pakistan in May 2025

3 by the U.S. during the ongoing Iran war

1 by Israel in today's strikes

#sigmaadvancedsystems#sigmaadvanced

Sigma Advanced Systems — Could be India's Most Underrated Dual-Engine Defence Play?

What if one company was simultaneously:

🔵 Writing the firmware for India's next-gen missiles 🔴 Machining jet engine parts for Rolls-Royce in the UK

Same balance sheet. Same team.

The Business = two engines running in parallel

Engine 1: Defence Electronics→ Missile & avionics sub-systems → Multi-domain radars & counter-UAS (anti-drone shields) → Naval & submarine ruggedized electronics → CEMILAC + AS 9100 Rev D flight-certified — mandatory for the Indian MoD

Engine 2: Precision Engineering (Aerostructures)→ 5-axis & 8-axis CNC machining of aero-engine housing parts → NADCAP-certified chemical surface treatment — rare globally → Fuelled by the acquisition of UK's Nasmyth Group

Revenue split:

Electronics: sovereign Indian MoD orders

Precision Eng: £300M Rolls-Royce contract (₹3,800 Cr over 7 years)

Q4FY26 revenue: ₹323 Cr (+469% YoY). This is no longer a small-cap experiment.

The Real Moat

This isn't a story about who has the best product. It's about who can even get certified to make it.

Supply-side lock:→ AS 9100 Rev D + NADCAP + CEMILAC + DGQA = 4 separate certifications → Each takes 2–4 years of zero-defect audits → ₹130–190 Cr minimum capex just to set up a competing facility → Certifications are facility-specific and non-transferable

Demand-side lock:→ Sigma's sub-systems are written into OEM master airframe blueprints→ Switching supplier = $2–5M re-validation + 24 months FAA/EASA recertification → Customer retention: >95% on mature platforms

The Nasmyth arbitrage (uncopiable):→ UK front-end for NADCAP finishing + Western OEM relationships → Hyderabad back-end for low-cost 5-axis CNC machining → Sigma takes a Rolls-Royce order. Nasmyth handles the front-end design and NADCAP finishing. Hyderabad handles the bulk CNC carving at 35–40% lower cost. The customer sees a UK-certified supplier. The P&L sees Indian manufacturing costs. → The two nodes are only valuable together — which is precisely what makes the combination hard to replicate. That window has already closed.

The Numbers (Stripped of the Noise)

Before anything else — a flag that separates serious investors from the rest.

FY26 reported PAT is ₹268 Cr. Screener shows EPS of ₹15.21. Both numbers are technically correct and completely misleading. Strip out the ₹262 Cr one-time land and asset sale gains and the actual defence manufacturing business earned ₹16 Cr in core PAT in FY26. Core EPS: ₹2.28. That's the real starting line.

Here's what the core operational business actually looks like:

Revenue is real and scaling — ₹474 Cr in FY26 to a projected ₹938 Cr by FY28. The Rolls-Royce contract alone runs at ₹543 Cr per year. Current installed capacity is ₹600 Cr. A ₹95 Cr capex program in FY27 takes that ceiling to ₹1,250 Cr. The FY28 projection assumes only 75% utilisation — there's 33% upside if execution holds.

Margins today are honest and modest. Core EBITDA is 10.4% in FY26 -- The path to 19% by FY28 is entirely a Nasmyth story. Every machining job that migrates from high-cost UK workshops to Hyderabad flows directly into margin.

By FY28, core PAT reaches ₹108 Cr and fully diluted EPS hits ₹12.67 — on a post-placement share base of 8.50 Cr shares that already prices in the June 2026 preferential allotment.

The working capital discount is real and you need to price it in.

Debtor days sit at 270. Net cash cycle is 310 days. Sigma is essentially pre-financing ~₹350 Cr of working capital for the Ministry of Defence at any given time. The fix is the revenue mix shifting toward Rolls-Royce, which pays on commercial terms. As that happens, debtor days compress to 210 by FY28 and CFO reaches ₹114 Cr. ROIC climbs from 7.1% to 13.4%.

Management & Governance

Promoters hold 71.22%, pledged shares are zero — completely cleared, zero forced liquidation risk, zero overhang — and they chose a ₹460 Cr equity raise over bank debt to fund growth, with India Ratings independently monitoring every rupee of deployment.

The walk-the-talk record is clean: margin pivot promised and delivered, Nasmyth integration promised and delivered, ₹3,800 Cr Rolls-Royce contract signed — founders are fully in, unencumbered, and building with their own skin in the game.

Closing - know the past to forecast the future

This company has a complicated past worth understanding before you size a position.

Megasoft Limited was a Hyderabad-based telecom software company that for years sat dormant on the BSE — negligible revenue, no meaningful business, a shell in all but name. The transformation into a defence engineering company happened through a reverse merger with the unlisted private entity Sigma Advanced Systems, sanctioned by NCLT only in December 2025. The listed vehicle that retail investors are buying today is legally the same entity that was filing near-zero revenue returns as a telecom software company twelve months ago.

Layer on top of that: a ₹262 Cr gain from selling land and assets that inflated FY26 reported profits to ₹268 Cr — numbers that led many investors to build models on ₹15.21 EPS when the actual defence business earned ₹16 Cr in core PAT. And a UK acquisition — Nasmyth Group — executed in November 2025, consolidated for only five months in FY26, carrying its own one-time transaction costs of ₹9.13 Cr, and still in early integration. These are not small footnotes. They are the entire context behind every headline number this company has reported so far.

So the question is whether the overhang from that messy past has been genuinely wiped clean — and the evidence is starting to point that way.

The shell is no longer a shell. The NCLT merger is sanctioned, the name is changed, the promoter structure is consolidated at 71.22% with zero pledged shares. The asset sales that distorted FY26 are one-time and done — they won't repeat, which means FY27 reported numbers will finally reflect only what the factories produce. The ₹460 Cr equity raise retires the debt that the transition period accumulated. And Nasmyth, whatever its integration complexities, just unlocked a £300 Million seven-year contract with Rolls-Royce — one of the most demanding aerospace customers on the planet. You do not win that contract without genuine engineering credibility.

The order book now has a different character entirely. ₹3,800 Cr from Rolls-Royce. ₹208 Cr in artillery shell exports. ₹107 Cr from North American defence customers. A ₹450 Cr electronic warfare contract from the Indian MoD. These are not prototype orders or one-off government allocations — these are series production commitments from customers who spent years validating the supplier before signing.

The past was messy. The transition was opaque to anyone relying on screening platforms. The FY26 numbers require significant stripping before they tell you anything useful. All of that is fair and should be priced into your risk assessment.

But the overhang is structural, not permanent. A dormant shell has been replaced by a live operating entity. A real estate windfall has been replaced by aerospace contracts. And a telecom software footnote in Hyderabad is now a certified Rolls-Royce supply partner with seven years of revenue visibility.

Whether the bright future the order book promises actually converts into cash depends entirely on one thing: Nasmyth workload migrating to Hyderabad fast enough to show up in margins before the market loses patience. Watch the FY27 quarterly filings. When debtor days compress and normalised EBITDA crosses 15%, the transformation story stops being a thesis and starts being a fact.

[Not investment Advice, DYOR]

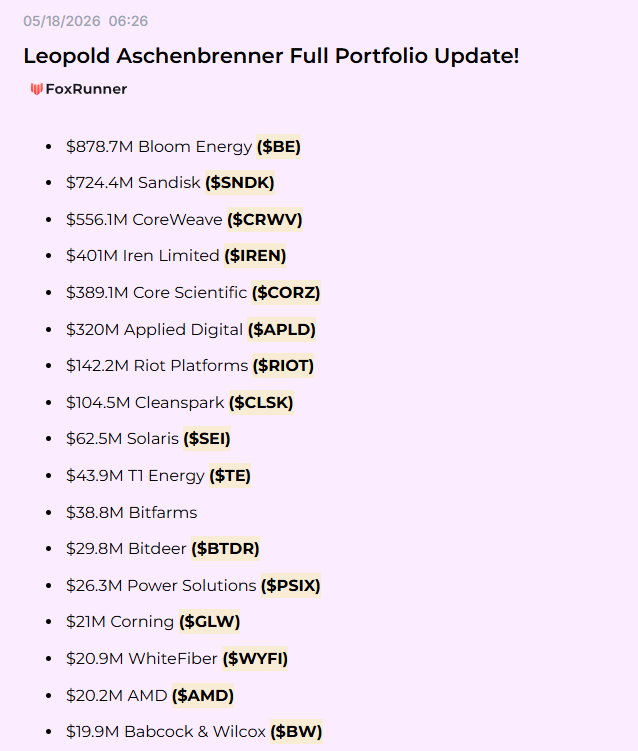

For those who do not know, Leopold Aschenbrenner is the 25 year old man who predicted the spike on $LITE, $SNDK, $BE, and more! He is one of the most watched names on Wall Street as his hedge fund gained from $200 million to now over 5.5 BILLION dollars!

HIS NEW PORTFOLIO!

Got laid off? Find 2 people and do a revenge startup.

What did the previous company screw up? Try 3 products they slept on. Double down on whatever gets traction. Either look at it like a victim or as an opportunity and become independent.

" $ONDS is trying to become the one stop shop for all your drone needs."

The stock up over 20% on the print. Backlog jumped from $68M to $457M as the acquisition stack consolidates into one platform.

Chamath on Mag 7 capex numbers and what means for capital allocation

"These companies will now get levered and highly sophisticated around the financial engineering. They will have more debt and all kinds of different vehicles. Term loans and revolvers, and all of this stuff.

And so they will look like these big bulky industrial businesses in 5 years. And I am not sure if there is a good valuation case to be made"

@reachanandl Message

4 PM IST works for me<week days>. I’m based in the UK, but over the next 7 weekends I’ll be attending an Agentic AI course 3.30 pm .so wont available that time during weekends

![ramesh_vd's tweet photo. #sigmaadvancedsystems #sigmaadvanced

Sigma Advanced Systems — Could be India's Most Underrated Dual-Engine Defence Play?

What if one company was simultaneously:

🔵 Writing the firmware for India's next-gen missiles 🔴 Machining jet engine parts for Rolls-Royce in the UK

Same balance sheet. Same team.

The Business = two engines running in parallel

Engine 1: Defence Electronics→ Missile & avionics sub-systems → Multi-domain radars & counter-UAS (anti-drone shields) → Naval & submarine ruggedized electronics → CEMILAC + AS 9100 Rev D flight-certified — mandatory for the Indian MoD

Engine 2: Precision Engineering (Aerostructures)→ 5-axis & 8-axis CNC machining of aero-engine housing parts → NADCAP-certified chemical surface treatment — rare globally → Fuelled by the acquisition of UK's Nasmyth Group

Revenue split:

Electronics: sovereign Indian MoD orders

Precision Eng: £300M Rolls-Royce contract (₹3,800 Cr over 7 years)

Q4FY26 revenue: ₹323 Cr (+469% YoY). This is no longer a small-cap experiment.

The Real Moat

This isn't a story about who has the best product. It's about who can even get certified to make it.

Supply-side lock:→ AS 9100 Rev D + NADCAP + CEMILAC + DGQA = 4 separate certifications → Each takes 2–4 years of zero-defect audits → ₹130–190 Cr minimum capex just to set up a competing facility → Certifications are facility-specific and non-transferable

Demand-side lock:→ Sigma's sub-systems are written into OEM master airframe blueprints→ Switching supplier = $2–5M re-validation + 24 months FAA/EASA recertification → Customer retention: >95% on mature platforms

The Nasmyth arbitrage (uncopiable):→ UK front-end for NADCAP finishing + Western OEM relationships → Hyderabad back-end for low-cost 5-axis CNC machining → Sigma takes a Rolls-Royce order. Nasmyth handles the front-end design and NADCAP finishing. Hyderabad handles the bulk CNC carving at 35–40% lower cost. The customer sees a UK-certified supplier. The P&L sees Indian manufacturing costs. → The two nodes are only valuable together — which is precisely what makes the combination hard to replicate. That window has already closed.

The Numbers (Stripped of the Noise)

Before anything else — a flag that separates serious investors from the rest.

FY26 reported PAT is ₹268 Cr. Screener shows EPS of ₹15.21. Both numbers are technically correct and completely misleading. Strip out the ₹262 Cr one-time land and asset sale gains and the actual defence manufacturing business earned ₹16 Cr in core PAT in FY26. Core EPS: ₹2.28. That's the real starting line.

Here's what the core operational business actually looks like:

Revenue is real and scaling — ₹474 Cr in FY26 to a projected ₹938 Cr by FY28. The Rolls-Royce contract alone runs at ₹543 Cr per year. Current installed capacity is ₹600 Cr. A ₹95 Cr capex program in FY27 takes that ceiling to ₹1,250 Cr. The FY28 projection assumes only 75% utilisation — there's 33% upside if execution holds.

Margins today are honest and modest. Core EBITDA is 10.4% in FY26 -- The path to 19% by FY28 is entirely a Nasmyth story. Every machining job that migrates from high-cost UK workshops to Hyderabad flows directly into margin.

By FY28, core PAT reaches ₹108 Cr and fully diluted EPS hits ₹12.67 — on a post-placement share base of 8.50 Cr shares that already prices in the June 2026 preferential allotment.

The working capital discount is real and you need to price it in.

Debtor days sit at 270. Net cash cycle is 310 days. Sigma is essentially pre-financing ~₹350 Cr of working capital for the Ministry of Defence at any given time. The fix is the revenue mix shifting toward Rolls-Royce, which pays on commercial terms. As that happens, debtor days compress to 210 by FY28 and CFO reaches ₹114 Cr. ROIC climbs from 7.1% to 13.4%.

Management & Governance

Promoters hold 71.22%, pledged shares are zero — completely cleared, zero forced liquidation risk, zero overhang — and they chose a ₹460 Cr equity raise over bank debt to fund growth, with India Ratings independently monitoring every rupee of deployment.

The walk-the-talk record is clean: margin pivot promised and delivered, Nasmyth integration promised and delivered, ₹3,800 Cr Rolls-Royce contract signed — founders are fully in, unencumbered, and building with their own skin in the game.

Closing - know the past to forecast the future

This company has a complicated past worth understanding before you size a position.

Megasoft Limited was a Hyderabad-based telecom software company that for years sat dormant on the BSE — negligible revenue, no meaningful business, a shell in all but name. The transformation into a defence engineering company happened through a reverse merger with the unlisted private entity Sigma Advanced Systems, sanctioned by NCLT only in December 2025. The listed vehicle that retail investors are buying today is legally the same entity that was filing near-zero revenue returns as a telecom software company twelve months ago.

Layer on top of that: a ₹262 Cr gain from selling land and assets that inflated FY26 reported profits to ₹268 Cr — numbers that led many investors to build models on ₹15.21 EPS when the actual defence business earned ₹16 Cr in core PAT. And a UK acquisition — Nasmyth Group — executed in November 2025, consolidated for only five months in FY26, carrying its own one-time transaction costs of ₹9.13 Cr, and still in early integration. These are not small footnotes. They are the entire context behind every headline number this company has reported so far.

So the question is whether the overhang from that messy past has been genuinely wiped clean — and the evidence is starting to point that way.

The shell is no longer a shell. The NCLT merger is sanctioned, the name is changed, the promoter structure is consolidated at 71.22% with zero pledged shares. The asset sales that distorted FY26 are one-time and done — they won't repeat, which means FY27 reported numbers will finally reflect only what the factories produce. The ₹460 Cr equity raise retires the debt that the transition period accumulated. And Nasmyth, whatever its integration complexities, just unlocked a £300 Million seven-year contract with Rolls-Royce — one of the most demanding aerospace customers on the planet. You do not win that contract without genuine engineering credibility.

The order book now has a different character entirely. ₹3,800 Cr from Rolls-Royce. ₹208 Cr in artillery shell exports. ₹107 Cr from North American defence customers. A ₹450 Cr electronic warfare contract from the Indian MoD. These are not prototype orders or one-off government allocations — these are series production commitments from customers who spent years validating the supplier before signing.

The past was messy. The transition was opaque to anyone relying on screening platforms. The FY26 numbers require significant stripping before they tell you anything useful. All of that is fair and should be priced into your risk assessment.

But the overhang is structural, not permanent. A dormant shell has been replaced by a live operating entity. A real estate windfall has been replaced by aerospace contracts. And a telecom software footnote in Hyderabad is now a certified Rolls-Royce supply partner with seven years of revenue visibility.

Whether the bright future the order book promises actually converts into cash depends entirely on one thing: Nasmyth workload migrating to Hyderabad fast enough to show up in margins before the market loses patience. Watch the FY27 quarterly filings. When debtor days compress and normalised EBITDA crosses 15%, the transformation story stops being a thesis and starts being a fact.

[Not investment Advice, DYOR]](https://pbs.twimg.com/media/HKiEqf4aUAAIIxy.png)