Being bad is not good but trying to be good by spending excessive energy & huge resources for the sake of being good is no good either. Hope I learnt it right 🙄. Thank you @AswathDamodaran for this insight! @malpani_megha

The promise of ESG is that it is an unalloyed good, with companies, investors and society all benefiting from its adoption. I believe that claim is internally inconsistent and at odds with the data. https://t.co/N4QEFn9IwI

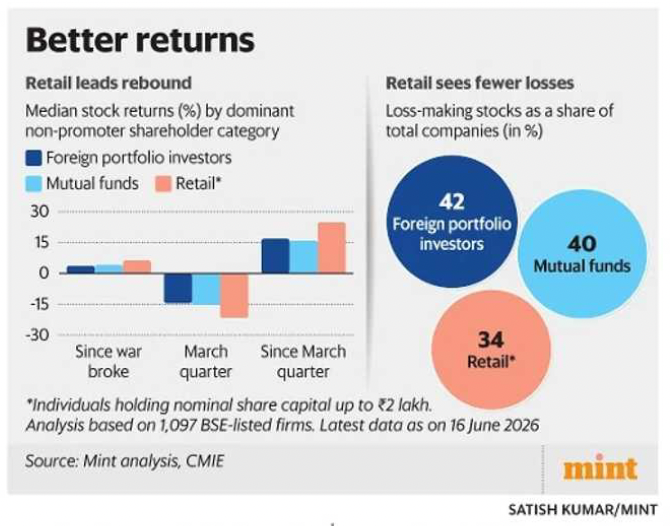

Since the start of the West Asia conflict on 27th February 2026 :

• Stocks where retail investors hold the majority stake delivered a median return of +6.4%

• The same number for stocks dominated by Mutual Funds was +4.1%

• For FII-dominated stocks, it was +3.7%

So, does this mean retail investors are smarter than Mutual Funds and FIIs?

Let's look at another dataset.

From 1st January 2026 to 31st March 2026:

• Stocks where retail investors held the majority stake delivered a median return of -21.7%

• Mutual Fund-dominated stocks delivered +15.3%

• FII-dominated stocks delivered -14.5%

Does this mean the skill sets of retail investors, fund managers, and FIIs dramatically changed between Q1 and the period of the war? (Incidentally, the two periods even overlap by a month.)

Let's add one more piece of data.

Since the conflict began:

• Nifty 50: -4.3%

• Nifty Midcap 150: +4.3%

• Nifty Smallcap 250: +10%

Does that mean active retail investors have broadly outperformed Large & Mid Cap funds since the war began?

Also notice a small but important word used throughout this post: median, not average.

A few changes in the methodology, time period, starting point, benchmark, or statistic used can completely change the narrative.

Today, the challenge is no longer access to data.

The challenge is identifying which data matters and which data is merely interesting.

For investors with a 5-, 7-, or 10-year horizon, most of these short-term observations may have little bearing on outcomes.

Data is the new oil. And like oil, too much of it can be harmful if consumed indiscriminately.

As our Prime Minister said on 10th May:

"अगर हम तेल खाना कम करें ना, तो भी वह देश-भक्ति का बहुत बड़ा काम है। इससे देश सेवा भी होगी और देह सेवा भी होगी। इससे देश के खजाने का स्वास्थ्य भी सुधरेगा और परिवार के हर सदस्य का स्वास्थ्य भी अच्छा रहेगा।"

In investing, perhaps we can replace:

Oil → Data

Desh → Portfolio

Deh → Mental Health

Just as consuming less oil may benefit both the nation and the body, consuming less irrelevant data may benefit both the portfolio and the mind.

#DataCalories

Parag Parikh has 3 equity funds. iShares by BlackRock has more than 1,500 ETFs. Both are doing great for their target segments.

Costco has around 3,800 SKUs. Walmart has close to 140,000. Both are the top retailers in the world.

Tata Memorial Centre primarily caters to one disease. Manipal and Apollo are multi-specialty healthcare institutions. That doesn't make one more relevant than the other.

There are investors with only one asset class in their portfolio - real estate, equities, or fixed deposits. There are also investors who own almost every multi-asset fund available across fund houses.

The world is full of examples where seemingly opposite approaches succeed.

The question is often not, "Which approach is right?"

The question is, "Right for whom, and under what circumstances?"

#442To433 (FIFA)

One of the biggest myths in investing and business is that lower cost means less affluent customers.

But consider this:

• IndiGo often offers the cheapest airfares, yet many well-off travellers choose it over full-service airlines for its reliability and on-time performance.

• Costco offers some of the lowest prices in retail, yet many of its customers are financially comfortable enough to buy in bulk and pay annual membership fees.

• Cafés in Indiranagar serve coffee at a fraction of the price charged by five-star hotels, yet their tables are often occupied by founders, venture capitalists, and senior professionals.

• IKEA offers functional furniture at prices far below luxury brands, yet a significant portion of its customer base consists of well-off households.

• Low-cost mutual funds and passive funds charge a fraction of the fees of many exotic investment products, yet an increasing number of wealthy investors prefer them.

Very often, the wealthiest customers are not buying the most expensive product in the room. They're buying the smartest one.

#ValueOverVanity

It's been over four years, and the war that Ukraine was supposed to lose in 2–3 weeks is still on. Many times over these four years, the tide has turned against mighty Russia.

It's been more than 100 days, and not a single US soldier has been able to set foot on Iranian soil (other than perhaps during one rescue mission) in a conflict that many expected to be over in 4–6 weeks.

And it's not the first time in history.

The US had to retreat from Vietnam. Both the US and Russia have had patchy records in Afghanistan. And about Iraq - the less said, the better.

The weak aren't as weak as many believe.

And the mighty aren't as strong as they believe themselves to be.

Markets, much like wars, have a way of reminding us of that.

A single fund house - Vanguard, with its largely low-cost passive investment approach, manages over $12 trillion in assets.

The entire mighty hedge fund industry manages less than half of that.

The lesson? Never underestimate the power of the underestimated.

#ItsNotGuaranteedThatFranceWillWinFIA

Narrative: Gold prices go up when geopolitical uncertainty is high.

Reality: Geopolitical uncertainty today is far higher than it was on 29th January 2026.

Narrative: The global silver market has been in a structural supply deficit for six consecutive years. Prices will keep rising as long as the deficit continues.

Reality: The supply deficit still exists. The price doesn't.

Narrative: Precious metals are safe havens. They have the volatility of bonds, not equities.

Reality: The last few months suggest otherwise.

Narrative: Gold rarely enters a bear market and falls 20%+ in a short period of time.

Reality: Whether it is rare or common is not the point. What matters is how much weight it carries in your portfolio when it happens.

At times, five months are enough to teach us more about asset allocation than years of reading books.

Nothing lasts forever. Not even the gold standard.

#GoldenLessons

On one hand, we have podcasts stretching 3+ hours with millions of loyal listeners. On the other hand, we have a craze for micro-dramas where an entire season wraps up in 120 minutes.

On one hand, we have warmongers aspiring for Nobel Peace Prizes. On the other hand, we have peacemakers who can't get a seat at the table.

On one hand, we have people fasting for 9, 28, even 40 days straight. On the other hand, we have the "graze every 2 hours or your metabolism dies" crowd.

On one hand, we have digital nomads owning nothing and living everywhere.

On the other hand, we have people taking 30-year home loans for 600 sq ft.

On one hand, we have people doing silent retreats for 10 days. On the other hand, we have FOMO so severe that their phone goes to the bathroom with them.

On one hand, we have 6 crore mutual fund investors patiently building wealth.

On the other hand, we have expiry-day options traders who want the outcome before 3:30 PM.

It's not that the middle ground has disappeared. It's just becoming a much lonelier place.

#MyLongestHoldingPeriodWasDhurandhar7Hours2Minutes

PMS and Mutual Funds are often compared, but the real question is not which product is superior, it is which one is right for a particular investor.

In my recent conversation with @MVachhrajani on Your Money Matters on @NDTVProfitIndia , we discussed:

• PMS vs Mutual Funds: performance, costs, and taxation

• Why concentration can be both a strength and a weakness

• How PMS and mutual funds behave differently during market corrections

• Which option may be better suited for different investor profiles

Sharing the conversation for investors evaluating these vehicles as part of their long-term wealth creation journey.

My thanks to @NDTVProfitIndia and @MVachhrajani for curating a thoughtful discussion on an important topic.

#PMSvsMutualFunds

https://t.co/ct7ng2Zi4O

Look at the 12-month equity returns in USD for some of the global indices.

Most of these indices were in bad shape from a historical return perspective in 2022. No one was interested in them at that point in time, while everyone wants to invest in them today.

Now let's look at our home market.

The last one-year return of the BSE Sensex in USD terms (S&P DOLLEX-30) is -18%.

No one seems interested in this index at this point in time, and most investors want to avoid it.

Good news and good stock prices rarely come together and neither does good investing behaviour.

The assets everyone wants to buy today are often the ones nobody wanted a few years ago.

The assets everyone wants to avoid today may look very different a few years from now.

Investor attention usually arrives after returns, not before.

#SentimentFollowsReturns

There is a country that recently raised 50% more money through its bond issue than what it had originally asked for.

Its currency has remained broadly stable against the USD over the last one year.

During the recent IMF visit, it reaffirmed its commitment to reach 2% fiscal surplus next year

Would you invest in this country? Probably yes.

This country was shut out of the global bond market for four years and its 10 years bond trades at 12.75%

It has received 25 IMF bailouts.

Its democracy is in shambles, and a Field Marshal remains the major power centre.

It does not have enough foreign exchange reserves to cover even three months of imports.

It relies on Gulf states for nearly 80% of its fuel requirements.

Would you invest in this country? Probably no.

It is friendly with the US, China, and Saudi Arabia and all three, in one way or another, have been helping it financially.

Would you invest in this country now? Maybe yes.

The name of the country is Pakistan.

Would you invest in this country now? For many Indian investors, definitely no.

If I had mentioned the country's name at the beginning, most of us might not have even bothered reading the full post.

Yet, this country's stock market has generated better returns for an Indian investor over the last five years than our own market.

And you still think macros alone have a major role to play in equity market and currency performance?

Sometimes, the table on which you sit matters more than the cards you hold.

#DhurandarDilemmas

Narrative: Crude is the reason the Indian market is correcting.

Reality: Crude oil fell 18% in May, and the market is still in the red.

Narrative: If INR weakening reduces in intensity, the market may take a breather.

Reality: INR strengthened from 97 to 95, and the intensity of the market's fall actually increased.

Narrative: FII flows are the culprit. Markets that have seen FII outflows are in a mess.

Reality: India has seen FII outflows of USD 26 billion from 1st January 2026 till now. The number is USD 77 billion for Korea (almost three times India). Korea is up 102% YTD, while we (Nifty 50) are down 11% YTD.

By the way, Taiwan has also seen net FII selling this year and is up 55% YTD

Narrative: Don't do SIPs. They're not a good vehicle. SIP investors are merely giving an exit to FIIs.

Reality: The 5-year rolling SIP CAGR for Nifty 100 is 13.14%, Nifty Midcap 150 is 17.66%, and Nifty Smallcap 250 is 15.47%.

If you don't have a lump sum and save monthly from your salary, show me a better way of investing over the last 5 or 10 years. Ideally, SIPs should be diversified across India and offshore markets. But even for someone who invested only in India, SIPs have generated meaningful inflation-beating real returns over 5/7/10 years

At times, we all interpret market moves based on easy narratives and short term moves without taking the cognitive load of checking the facts.

#LowEffortThinking

The joy of winning in tennis never feels quite the same when it comes from your opponent's double faults or unforced errors, rather than from winning a tough, tricky, hard-fought rally.

The joy of winning market share in business never feels as satisfying when it comes because a competitor went bankrupt, rather than because you earned it through better strategy, hard work, execution, and healthy competition.

The joy of finally owning that elusive dream watch never feels the same when it's gifted by parents or in-laws, rather than when you save, work hard, earn the bonus, and reach the financial milestone yourself.

And the joy of making money from a stock tip (even if it works out) is never quite as satisfying as doing the detailed research, putting in the effort, building conviction, and then watching your hypothesis play out even if the money earned in both cases is exactly the same.

Because in the end, it's not just about the outcome.

It's about the journey, the effort, and the satisfaction of knowing that you earned it.

#EarnedNotGifted

In our society WhatsApp group:70+ years: Discussion is around religion and different poojas to be organised.

60-70 years: Vegetable vendor's billing, music from other apartments after 8 pm, doctor's availability around the society, and tailors for alteration.

50-60 years: Illegal construction, property valuation, society dues/rules, and whether quick-commerce delivery boys should be allowed to use the lift.

40-50 years: Pets (both lovers and haters), availability of drivers, cooks, maids, and domestic help.

30-40 years: Passport renewal, Aadhaar address changes, school admissions, and government paperwork.

Below 30 years: ............

I have yet to read a single message from this cohort in the last three years.

It's somewhat similar in investing.

From 30 to 70 years of age, investors are broadly clear about what they want from their portfolios.

People in their 30s are building wealth.

People in their 40s are balancing growth with responsibilities.

People in their 50s start thinking more seriously about retirement.

People in their 60s and 70s want stability, income, and peace of mind.

But it is the sub-30 investor that we have never really been able to decipher.

Some don't have spare money to invest.

Some have money but don't want to think about investing.

Some are willing to take extreme risks.

Some are happy keeping everything in cash.

Some buy only stocks.

Some buy only crypto.

And many seem completely indifferent to markets altogether.

At times, I wonder if it's a confused generation.

Then I remind myself:

Maybe the under-30 investor isn't confused.

It's the advisor who is confused and asking the wrong questions.

#BlueTicksNoReplies

Next to the office vending machine today, I spotted a recipe pamphlet titled "Make It Your Own."

Feeling adventurous, I decided to try a Coconut Americano.

Bought coconut water from the BB Instant fridge next to the coffee machine, pulled an espresso shot, mixed it up... and didn't like it.

"No problem," I thought. Maybe Coconut Americano just isn't my thing.

Round two: Ginger Espresso Tonic.

Bought a tonic water, pulled another espresso shot, mixed it up... and didn't like that either.

Both mugs went into the sink.

Two wasted espresso shots. One coconut water. One tonic water. Ten minutes spent experimenting and another 7-8 minutes writing this post (that too on a super busy day).

And now I'm convinced BB Instant and the coffee bean company are co-conspirators. 🙂

Eventually, I went back to my reliable iced latte and got on with work.

The same thing happens in investing:

Every day, we're surrounded by advertisements for AIFs, private credit, unlisted shares, SIFs, structured products, and the latest "exclusive" opportunities.

Just because something is available doesn't mean it's suitable.

Not everything is for everyone.

My coffee experiment cost me about ₹150. Bad investment experiments can cost a lot more.

Sometimes, the best investment decision is the same as the best coffee decision: know what works for you.

#BrewYourOwnPortfolio

Last 1 year returns (in USD)

Nvidia: +59%

Intel: +483%

Micron: +679%

Sandisk: +3772%

Nasdaq 100: +37%

At the same time:

Microsoft: -9.14%

Meta: -5%

Last 5 years absolute returns and not CAGR (in INR):

Kotak Mahindra Bank: +8.15%

HDFC Bank: +3.79%

HUL: -5%

Asian Paints: -10%

Nifty 50: +55%

Three learnings:

1. Buying a few “high quality” stocks and expecting to retire based on that alone may or may not work.

2. Diversification helps - both within your home country and globally.

3. If stock investing is not your day job, it may be worthwhile exploring active funds / index funds instead of trying to pick individual winners.

No sane investor would have picked Intel over Nvidia, Microsoft or Meta a year back (other than the US government, of course 🙂).

#NobodyKnowsAnything #MarketsHaveHumour

I have a dishwasher, robot vacuum , washer + heat pump dryer at home. Why do I need domestic staff?

I have a smart irrigation system with AI monitoring. Why do I need a gardener?

I have a Delonghi Maestro and a Wilfa tea maker. Why do I need Chai Point or Blue Tokai?

I have DelishUp. Why do I need Zomato and Swiggy?

I have Barsys 360. Why do I need to go out on weekends?

And I have so many AI portfolio tools. Why do I need a financial advisor?

Because I didn’t automate my life to work harder. I automated it to live better.

The question is - did you?

#LivingSmarterOrLivingHarder

s part of our investor education initiative, I was featured on @NDTVProfitIndia's "Your Money Matters" with

@MVachhrajani

Topic: Are You Choosing Mutual Funds the Wrong Way?The Problem With Chasing Past Returns

The discussion focused on one of the most common investing mistakes, choosing mutual funds primarily based on historical returns or last year’s top-performing funds. We spoke about how fund rankings can become a drag at times, the risks of chasing recent out-performers, the impact of fund size on performance, consistency versus high returns, risk-adjusted investing, and the role of investor behaviour in long-term wealth creation.

Core message: Successful investing is less about predicting the next winner and more about building a disciplined framework that survives market cycles.

Aired on 20th May, 5 PM. Thank you @MVachhrajani and @NDTVProfitIndia for hosting such a thoughtful discussion, and for the opportunity.

#YourMoneyMatters

@malpani_megha@Zvestfamilyoffc

https://t.co/Dlp0IcGgCc

A few days back, in a restaurant in a non-English speaking geography, I ordered a Margherita pizza for my daughter and was served a Margarita cocktail instead.

Reason?

I didn’t specify. I just said, “Get me a Margherita please.”

I was too lazy to use Google Translate and explain properly.

And the staff taking the order probably realised I was a tourist and served me what tourists usually like.

I have seen this happening in investing too.

When your neighbour mentions that he made 10X in a property, you are too lazy to ask the holding period. And your neighbour doesn’t consider it important enough to calculate CAGR.

When your friend mentions the stock tip that helped him make much more than NVIDIA or Alphabet, you are too lazy to ask about his overall portfolio return. And he is too ecstatic to realise whether it was skill or luck.

When your distant cousin mentions the mouthwatering return on his speculative crypto coin, you are too lazy to ask how much he actually invested. And he is too preoccupied to notice how little it changed his overall net worth.

Unless we ask, and till we keep assuming, we end up in situations where a small child remains hungry for another 20 minutes… and a whiskey lover has to contend with a savoury-sweet drink instead.

Returns without context are just financial cocktails.

#BenchmarkYourStories