Introducing the Scottish-American travel dictionary 🇺🇸🏴

We’ve put together this guide to keep the Tartan Army out of trouble in the States.

Read carefully to avoid confusing the locals, deeply offending the country, or being interrogated by Homeland Security over a sandwich.

Ryan Cohen just dropped $GME earnings a week early. Just like I predicted.

On the day before HSR clears.

While the stock sits below his own buy.

No one knew the date. That was the point.

The numbers:

- $389.6M net income - highest quarter in GameStop's history!!

- Revenue up 14% YoY!!

- Operating income $143.3M vs a LOSS of $10.8M a year ago!!

- SG&A cut from $228M to $201M!!

- Cash UP to $9.7B!!

- $268.4M unrealized gain on eBay derivative position

- $1.0B in collateral pledged for derivative asset - the eBay position is a named balance sheet item

- $2.0 BILLION share repurchase authorization approved today

19 SEC filings in 26 days.

Then silence.

Everyone assumed earnings was next week. NOT ME.

He surprise dropped the best quarter in the company's history, with the eBay derivatives visible in the financials for the first time, a $2B buyback at the cash floor, the day before his 34.5M eBay derivatives become convertible to voting shares.

$EBAY AGM is in 15 days.

https://t.co/oaPe4Eo8Uk is still dark.

GameStop reports highest quarterly net income in company history of $389.6 million. Highest first quarter operating income in GameStop’s history of $143.3 million. Net sales grew 14% year-over-year, driven by collectibles. Cash, marketable securities, digital assets and related receivables, and collateral pledged for derivative asset of $9.7 billion.

https://t.co/BAu3T6V9w4

This New Glenn rocket explosion released 20% of the energy of the Hiroshima atomic bomb and that wasn't even the bad part:

→ The pad: LC-36 is the only pad on Earth that launches New Glenn and now it's gone. Over $1B to build. SpaceX needed 7 months to rebuild after a similar hit.

→ The deadline: Amazon needs 1,618 satellites up by July 30 to keep its FCC license. It has ~300. The rocket that was supposed to help fix that just blew up twice in a row

SpaceX made us believe that landing rockets on barges was a normal expectation. Turns out rocket science is hard after all. Wishing the team a speedy recovery 🚀

You used to sell stuff on eBay.

Maybe an old camera. Maybe Beanie Babies. Maybe a coat that didn't fit.

You paid a small fee. The buyer got the thing. Everyone went home.

That eBay is gone.

The website looks the same. The logo is the same. The 135 million buyers are still there.

But the company isn't really a marketplace anymore.

It is an advertising business with a marketplace attached for distribution.

Last year, sellers paid eBay $2 billion just to make sure their own listings showed up.

Read that again.

The board calls this growth.

A Canadian who runs a video game store called it something else.

Here is what actually happened.

In 2020 the board hired a new CEO. His name is Jamie Iannone. He arrived with a strategy called focused categories.

In plain English, that means leaning into the stuff people pay extra for. Sneakers. Watches. Trading cards. Auto parts.

The everyday seller, the person with the camera and the coat, was no longer the customer.

The customer was now the seller who would pay to be seen.

In 2025 eBay did $80 billion in transactions. They kept $11 billion of that as revenue. Of that $11 billion, $2 billion came from advertising.

Sellers paid them $2 billion to promote listings on a website those sellers already pay fees to use.

That is the growth story.

In the same year, the number of enthusiast buyers, eBay's own term for their best customers, was 16 million.

It was also 16 million the year before.

And the year before that.

And the year before that.

Four years. Zero growth. They mention this on every earnings call without mentioning it.

So what does a company do when growth stops?

It buys back its own stock.

In 2025, eBay returned over $3 billion to shareholders. Most of that was buybacks. In February the board authorized another $2 billion on top.

Buybacks shrink the share count. Earnings per share goes up even when earnings stay flat. The stock price follows.

The stock was $68 a year ago. It is $108 today.

The company did not improve. The denominator got smaller.

Then a man from Canada noticed.

His name is Ryan Cohen. He runs GameStop. He started his career selling pet food online and sold it to PetSmart for $3.35 billion.

He looked at eBay. 135 million buyers. $80 billion in transactions. Real margins. Real cash flow. A board harvesting the business instead of running it.

He bought 5% of the company through derivatives and stock.

Then on May 4, he offered to buy the rest. $125 per share. $56 billion total.

On May 12, the eBay board rejected the bid. They called it not credible.

The math is credible.

What the board means by not credible is we would have to explain why we sold.

Then Cohen went on Piers Morgan.

He said eBay is run by a bunch of losers with perverse financial incentives.

He pointed out that eBay's CEO has been paid $144 million over six years.

He pointed out that he personally takes no salary and has put $128 million of his own money into the company he runs.

You do not have to like Ryan Cohen to notice he is making a point that is hard to argue with.

eBay used to be a place where regular people sold things to other regular people.

Now it is a $48 billion company whose largest growth driver is charging its own sellers to advertise to a buyer base that stopped growing four years ago, while spending billions a year buying its own stock to make the chart go up.

The board calls this strategy.

A video game CEO from Canada called it what it is.

The market is now waiting to see who else agrees.

Plz fix. Thx.

Sent from my iPhone

Allow me to translate this letter from eBay for those who don’t speak legalese:

Ryan,

We got your unsolicited offer to buy eBay for $125/share (half cash, half stock) supported by your 5% economic interest in eBay.

Our board, backed by the usual crew of bankers and lawyers who get paid either way, “thoroughly reviewed” it.

We’re rejecting it. Not because the math doesn’t work. Not because the highly confident letter from TD Securities for up to $20B on top of your $9B+ cash pile is fake. None of that.

We’re rejecting it because your entire approach to running a company is an existential threat to how we like to operate here.

Here are the reasons we feel this way, and the things we considered before paying consultants to write this:

1) We’d rather keep milking eBay as a “standalone” cash cow than let you turn it into something bigger and better.

2) Sure, you’ve got real financing lined up and you “know people” with deep pockets, but we’re going to call it “uncertain” anyway so we don’t have to engage.

3) Your plan would actually force real long-term growth and profitability changes we’d rather not be held accountable for.

4) The debt we pretended you can’t even obtain, the operational integration and focus on seller satisfaction, and most importantly, putting someone like you in charge of the combined entity all sound like a nightmare for our current leadership structure because all of us would have zero job security.

5) The valuation math only looks bad if you ignore the 46% premium you’re offering our shareholders and the upside from fixing eBay the way you fixed GameStop, which we are choosing to do and hoping nobody notices.

6) And I hope we buried the lede far enough here: Your governance and executive incentives are completely incompatible with ours. You and your board take zero cash, no salary, no bonuses, no golden parachutes. You buy shares with your own money and only get paid if shareholders win. We, on the other hand, like our nice, reliable annual payouts regardless of whether the stock is flat or the company is just coasting. We’re not about to hand over our golden goose to a guy who eats only what he kills.

Look, eBay is “strong” and “resilient” in the way every entrenched public company says it is while handing out eight-figure checks and perks to the C-suite. We’ve done the usual incremental stuff: tweaked the marketplace a bit, returned some capital, and we’d like to keep doing that without any cowboy from GameStop coming in and demanding actual skin-in-the-game accountability. Can you just leave us alone?

Our team remains focused on protecting the current regime and delivering “value”… mostly to ourselves and our consultants.

Thanks, but no thanks,

Paul S. Pressler Chairman of the Board, eBay (And proud beneficiary of the status quo)

1/ On How Short Life Is

A few years ago, I was walking around in a blizzard in SoHo (New York). It was late, midnight, and it was beautiful.

Some friends, about 15 blocks away, called: "come over?"

It was late, it was cold, was tired, thought "maybe not worth it" but then...

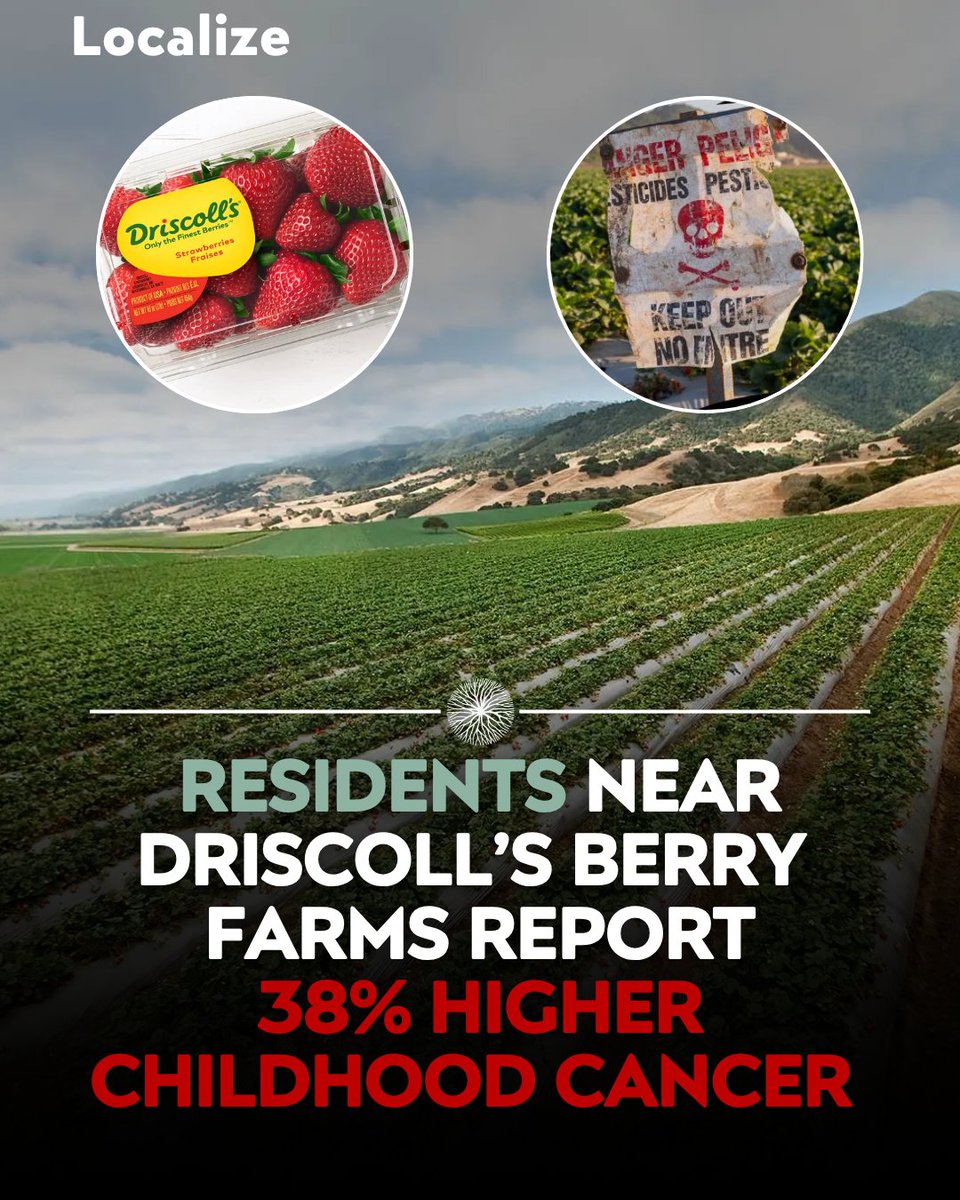

I wish this was fake but residents near Driscoll’s berry farms report a 38% higher incidence of childhood cancer.

Santa Cruz County is the heart of California's $3B strawberry industry and home to Driscoll's world headquarters.

Coincidentally, it also has the second-highest childhood cancer rate of any county in California.

At 22.5 childhood cancers per 100,000 children, the rate is more than 38% above the statewide average of 16.3.

Over 5,060 acres of pesticides linked to those same cancers are sprayed in the Pajaro Valley every year to grow 40% of California's strawberries.

Worst of all, it’s often next to schools and homes where children spend most of their time.

According to the latest data, over 2,000,000 pounds of pesticides were applied just in this school district’s area alone.

Driscoll’s is reported to apply two together:

1. 1,3-D: fumigant used to sterilize the soil, officially listed by the state as a carcinogen, causes tumors in multiple animal studies

2. Chloropicrin: originally deployed as a chemical weapon in World War I, so toxic that it kills or disables test animals before scientists can even evaluate its long-term carcinogenicity

But yeah it’s probably just a coincidence all the kids are getting cancer?

This is why you need to be buying local and seasonal fruit.

Do not trust major corporations to do the right thing for our food or health.

A Hungarian psychologist raised three daughters to prove that any child could become a chess grandmaster through early specialization. He succeeded. Two of them became grandmasters. One became the greatest female chess player who ever lived.

Then a sports scientist looked at the data and found something nobody wanted to hear.

His name is David Epstein. The book is called "Range."

The Polgar experiment is one of the most famous case studies in the history of deliberate practice. Laszlo Polgar wrote a book before his daughters were even born arguing that geniuses are made, not born. He homeschooled all three girls in chess from age four. By their teens, Susan, Sofia, and Judit were dominating tournaments against grown men. Judit became the youngest grandmaster in history at the time, breaking Bobby Fischer's record. The story became the gospel of early specialization. Pick a domain young, drill it hard, and you can manufacture excellence.

Epstein opens his book by telling that story honestly and then quietly demolishing the conclusion most people drew from it.

Chess works that way. Most things do not.

Here is the distinction that took him four years of research to articulate, and that almost nobody who quotes the 10,000 hour rule has ever read.

There are two kinds of environments in which humans develop expertise. Psychologists call them kind and wicked. A kind environment has clear rules, immediate feedback, and patterns that repeat reliably. Chess is the cleanest example. Every game ends with a winner and a loser. Every move is recorded. The board never changes shape. The pieces never invent new ways to move. A child who plays ten thousand games will see most of the patterns that exist in the game, and pattern recognition is exactly what chess mastery is built on.

A wicked environment is the opposite. Feedback is delayed or misleading. Rules shift. The patterns that worked yesterday may be exactly the wrong patterns to apply tomorrow. Most of the real world looks like this. Medicine is wicked. Investing is wicked. Building a company is wicked. Scientific research is wicked. Almost every job that involves a complex changing system with humans in it is wicked.

The Polgar sisters trained in the kindest environment any human can train in. Their success was real and the method was correct. The mistake was generalizing the method to fields where the underlying structure of the environment is completely different.

Epstein's research is what made the implication impossible to ignore.

He looked at the careers of elite athletes outside of chess and golf and found that the pattern was almost the inverse of what people assumed. The athletes who reached the very top of their sports were overwhelmingly people who had played multiple sports as children, specialized late, and often switched disciplines well into their teens. Roger Federer played squash, badminton, basketball, handball, tennis, table tennis, and soccer before tennis became his focus. The kids who specialized in tennis at age six and trained year-round for a decade mostly burned out, got injured, or topped out at lower levels of the sport.

The same pattern showed up everywhere he looked outside of kind environments. Inventors with the most patents had worked in multiple unrelated fields before their breakthrough work. Comic book creators with the longest careers had drawn for the most different genres before settling. Scientists who won Nobel Prizes were dramatically more likely than their peers to be serious amateur musicians, painters, sculptors, or writers.

The skill that mattered in wicked environments was not depth in one pattern. It was the ability to recognize when a pattern from one domain applied unexpectedly in another. That kind of thinking cannot be built by drilling a single subject. It can only be built by accumulating mental models from many subjects and learning to move between them.

The deeper finding is the one that should change how you think about your own career.

Specialists in wicked environments often get worse with experience, not better. Epstein cites studies of doctors, financial analysts, intelligence officers, and forecasters showing that years of experience in a narrow domain frequently produce more confident judgments without producing more accurate ones. The expert builds elaborate mental models that feel comprehensive and turn out to be increasingly disconnected from the actual structure of the problem. They stop noticing what does not fit their framework. They mistake fluency for understanding.

Generalists do better in wicked domains for a reason that sounds almost mystical until you understand the mechanism. They have less invested in any single mental model, so they abandon broken models faster. They are used to being a beginner, so they are not threatened by the discomfort of not knowing. They have seen enough different domains that they can usually find an analogy from one field that unlocks a problem in another. The technical name for this is analogical thinking, and the research on it is one of the most underrated bodies of work in cognitive science.

The single most useful sentence in the entire book is the one Epstein puts almost as a throwaway.

Match quality matters more than head start.

A person who tries six different fields in their twenties and finds the one that genuinely fits them will outperform a person who picked one field at fourteen and stuck to it on willpower alone. The lost years were not lost. They were the search process that produced the match. Every field they walked away from taught them something they later imported into the field they finally chose.

The reason this is so hard to accept is cultural, not empirical. We tell children to pick a path early. We reward the prodigy who knew at six. We treat the late bloomer as someone who failed to launch on time, when the data suggests they were running an entirely different and often more effective optimization process underneath.

The Polgar sisters were not wrong. The conclusion the world drew from them was.

If your environment is genuinely kind, specialize early and drill hard. If it is wicked, and almost every interesting human problem is, then the people who win are the ones who refused to specialize until they had seen enough to know what was actually worth specializing in.

You are not behind. You were running the right experiment all along.

I’m not a lawyer, but I’m a commodities trader and I know the rules of my own market. I wonder if Ravid and others have ever heard of the Eddie Murphy Rule?

It’s the closest thing commodities have to an insider trading statute and it originates from my favorite Christmas movie,Trading Places.

In the film, the Duke brothers get their hands on a stolen USDA crop report and try to corner orange juice futures. In 2010, Gary Gensler admitted under questioning that the scheme wasn’t clearly illegal at the time. Congress fixed it with Dodd-Frank §746 — codified at CEA §4c(a)(4), known ever since as the Eddie Murphy Rule. It bans trading commodity interests on misappropriated nonpublic U.S. government information. It reaches the leaker, the trader, and anyone in the chain who knew.

That covers stolen real information. The companion provision, CFTC Rule 180.1, covers the other case: knowingly or recklessly false statements of material fact, and the delivery of false reports affecting commodity prices.

Misappropriated truth and manufactured falsehood are both covered. The statute does not require the information to be accurate. It requires only that someone profited from a market that moved on it.

Worth thinking about every time a market-moving headline on Iran, OPEC, sanctions, or tariffs hits the tape minutes before any official confirmation, and is later quietly walked back.

The interesting question is who was positioned in the right strikes the hour before, and whether the chain from source to byline to brokerage account would survive a subpoena.

“Press freedom” is a real and important protection. It is not, and has never been, a shield for knowing participation in market manipulation or wire fraud. The First Amendment protects publishing. It does not protect trading.

A quick check list of Cohen’s actions:

1. Let shorts overextend → done

2. Finance through their pain → done ($4.6B raised)

3. Fortify the balance sheet → done (zero debt, cash fortress)

4. Build structural traps (warrants, NOLs, holdco architecture) → in progress

5. Deploy capital into acquisitions at scale → live right now (eBay bid)

6. Reveal the completed structure → upcoming (Annual meeting is the obvious window)

Read part 2 below 👇

True…. Working with founders in private companies, there’s a tremendous sense of ownership. That sense often disappears in larger companies that can easily turn into expansive bureaucracies that only know how to add but not subtract.

A simple query to plug into your favorite LLM when evaluating a public company:

In the last [3] years, how many open-market purchases—both in number and dollar amount—has the [company name] board of directors made?

The media still wants $GME investors to look stupid.

But the actual thesis has gotten sharper:

A debt-light company with billions in liquidity is trying to buy a stale internet marketplace, cut waste, plug in physical stores, add live selling, authenticate collectibles, and turn dead retail square footage into commerce infrastructure.

You do not have to agree with it.

But pretending there is no strategy anymore is intellectually lazy.

This is not 2021.

This is the second act.

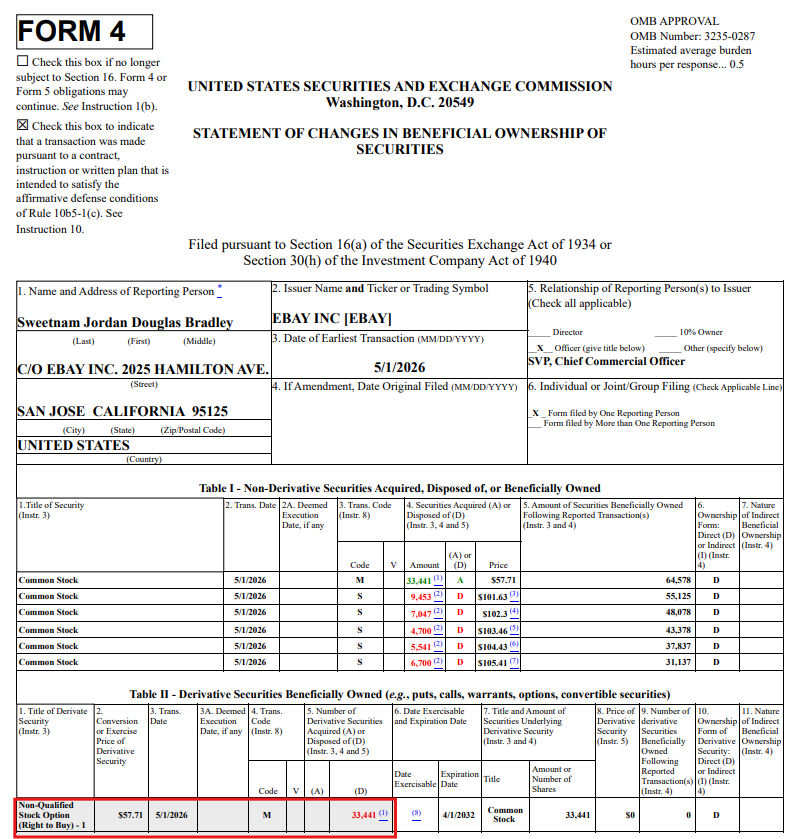

Wow EBAY CEO Jamie Iannone just sold $4,550,000 worth of stock and SVP CCO Jordan Sweetnam sold $3,426,000 on May 1, the same day WSJ published its exclusive $GME takeover bid story.

That is not a good look for EBAY.

"Professor, don't you find it curious that a new US-Iran peace deal leaks almost every time the 10y UST yield breaks 4.4% on the upside?"

"Actually, if I think about it, I don't find it curious at all."