So much noise everywhere. All you need now is to avoid all that are either over-leveraged or has some sort of bug or exploit. In the long run perhaps it doesn't matter as much, but right now just go for the safest pick and hold. This is where profit is made.

What just happened?

The S&P 500 just erased nearly -$2 TRILLION of market cap just hours after 3rd strongest US jobs report in 18 months.

Meanwhile, Bitcoin is officially down over -50% from its record high in October 2025.

What's happening? Let us explain.

(a thread)

A TON OF THINGS HAPPENED IN THE STOCK MARKET TODAY.

Here's a full recap:

1. $NVDA Nvidia CEO Jensen Huang joined President Trump’s China trip after receiving a last-minute invitation, increasing attention on the stalled H200 chip sales to China. Reuters reported that Trump called Huang after seeing reports that he had not been invited, and Huang later boarded Air Force One in Alaska. Nvidia hit an all time high today.

2. $NBIS Nebius reported Q1 revenue of $399M, ahead of the $388.6M estimate and up 684% year-over-year. Adjusted EBITDA came in at $129.5M, beating expectations of $90.5M, while ARR reached $1.92B, up 674% year-over-year and 54% quarter-over-quarter. For 2026, the company reaffirmed its target for year-end ARR of roughly $7B-$9B and raised its contracted power capacity outlook from more than 3GW to more than 4GW.

3. April PPI came in much hotter than expected, with headline producer prices rising 6% versus estimates of 4.9%. Core PPI also beat expectations, increasing 5.2% compared to the 4.3% forecast. This marks the highest producer inflation reading since March 2022.

4. Consumer credit stress is rising across major debt categories. In the U.S., 13.1% of credit card balances are now 90+ days delinquent, the highest level since 2011. Student loan delinquencies have climbed to 10.3%, the highest since 2020, while auto loan delinquencies reached 5.6%, the highest level on record.

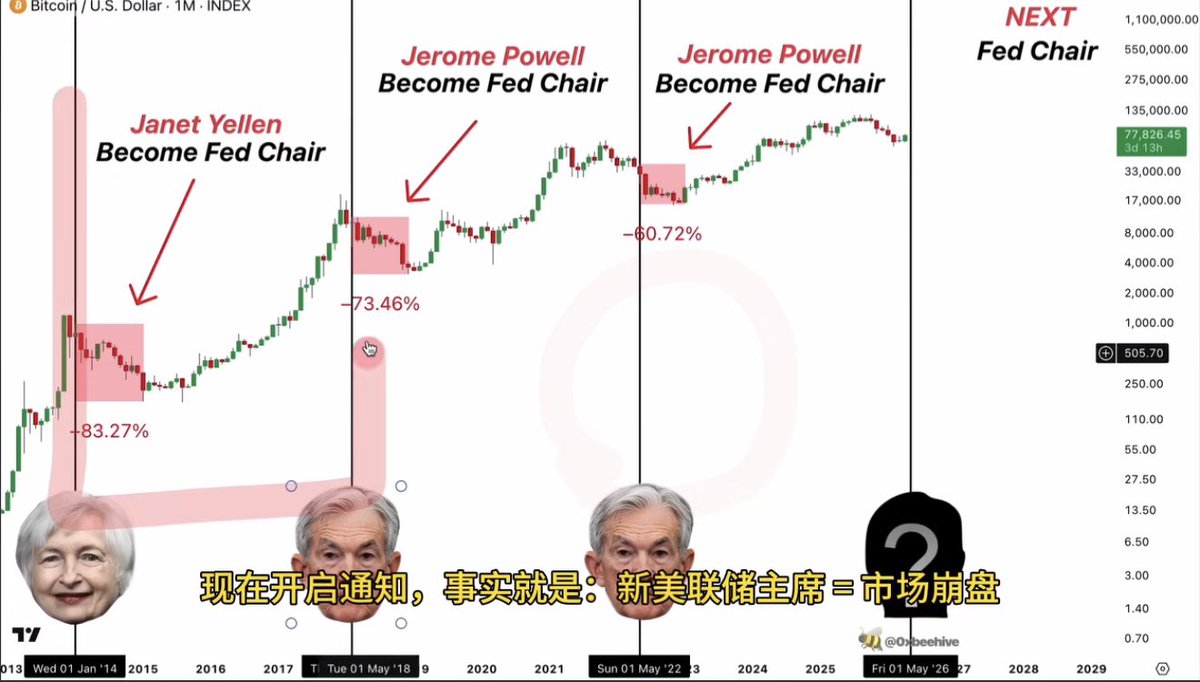

5. Kevin Warsh has been confirmed as the 17th Chair of the Federal Reserve, taking over at a time when inflation is rising again, Americans remain frustrated with the economy, and the Fed’s independence is facing intense political pressure. The Senate confirmed Warsh to a four-year term on Wednesday in a 54-45 vote, with unanimous Republican support and only one Democratic vote in favor, from Pennsylvania Senator John Fetterman.

6. Bank of America raised its AI data center systems forecast to $1.7T by 2030, up from its prior estimate of $1.4T, implying a 45% compound annual growth rate. The firm now expects AI accelerators to represent roughly $1.2T of that market, with AI networking reaching $316B as custom chips like Google’s TPUs and Amazon’s Trainium continue to scale.

7. $F Ford shares moved higher after Morgan Stanley said the company may announce energy storage supply agreements with large commercial customers, potentially including hyperscalers, within the next few months. Morgan Stanley estimates Ford Energy could be worth around $10B.

8. $HOOD Robinhood released its April 2026 monthly metrics, showing continued growth across the platform. Funded customers rose to 27.6M, up 1.65M year-over-year, total platform assets increased 49% to $345B, and April net deposits reached $6.0B, implying a 29% annual growth rate. Trading activity also remained strong, with equity trading volume up 57% year-over-year to $249B, while the margin book more than doubled from $8.4B a year ago to $18.0B, showing customers are borrowing more to invest. Crypto was the weaker area, with volumes down 33% from March and Bitstamp volumes falling 46% month-over-month.

9. U.S. data center construction spending rose 34% year-over-year in March to a record annualized pace of $50B. Spending has now increased 437% since the start of 2021, when the annualized run rate was about $9B, and 688% since 2018, when it was roughly $6B. At the same time, office construction continues to weaken, falling 9% year-over-year to $46B, its lowest level since 2015.

10. $CSCO Cisco reported Q3 revenue of $15.8B, above estimates of $15.54B and up 12% year-over-year. Adjusted EPS came in at $1.06 versus estimates of $1.04, up 10% year-over-year. Product orders rose 35%, networking product orders were up more than 50%, data center switching orders increased more than 40%, and campus networking orders rose more than 25%. Cisco also raised its FY26 AI infrastructure order outlook to $9B from $5B and lifted expected AI infrastructure revenue to $4B from $3B.

11. U.S. leveraged ETF assets have climbed to a record $177B, up $45B since the March market bottom. Tech remains the dominant category, representing about 69% of total leveraged ETF AUM. Within that, technology-focused funds hold $65B, semiconductor funds hold $32B, and Magnificent 7 funds hold $25B, while S&P 500-linked leveraged ETFs account for another $24B.

12. Anduril raised $5B at a $60B valuation in the private markets. Anthropic raised $30B at a $900B valuation. The street now awaits Cerebras going public tomorrow, with estimates assuming a $40-$50B valuation and SpaceX this summer at $2T.

WALL STREET IS THE GREATEST SHOW ON EARTH.

Two weeks ago, Paul Tudor Jones was sounding the alarm.

He went on record saying the U.S. stock market is at 252% of GDP, a level that makes 1929's peak of 65% and the dot com era's 170% look mild by comparison.

His message was if we mean revert to historical P/E multiples, you're looking at a 30 to 35% decline and at 250% of GDP, that wipes out 89% of GDP in wealth, tax revenues collapse, the bond market gets smoked, and the budget deficit explodes.

He said if you buy the S&P at today's valuations, history says your 10 year forward return is negative.

Then he went to a private AI conference with about 35 to 40 people and he came back and bought more AI stocks.

What changed? He walked out of that conference believing we are at the 1981 moment, the equivalent of Microsoft launching the PC for mass commercial adoption. Claude Code, launched in January, is the inflection point.

Before that conference, his framework was pure macro, valuations, leverage, liquidity but after it, he layered in a new variable, a productivity miracle that has historically rewritten the rules on valuation for a multi-year window.

He still believes a correction is coming.

He said if stock market cap reaches 300 to 350% of GDP, what follows will be breathtaking but he also said the AI bull market has another year or two to run and 40% more upside from here and that's enough of a runway to stay long.

He's not ignoring the risk but rather decided the opportunity is bigger than the risk right now.

This is exactly why Milk Road analysts hold these assets in their portfolios and is up massively.

Go PRO to see exactly what we hold, the allocations, and the full thesis behind every position, link below!

Great commentary yet again from BTIG’s Jonathan Krinsky

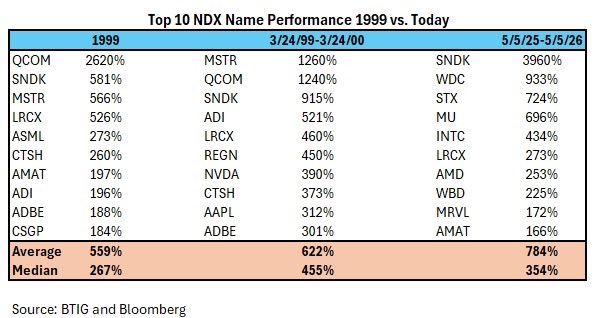

•Party Like It's 1999. In 1999, the best performing Nasdaq 100 stock was Qualcomm (QCOM, not rated), up 2600%. The best rolling 52-wk return for QCOM during the entire dot-com bubble was 2600%, so SNDK is beating that by 1300bps. Interestingly, the second-best stock in 1999 was SNDK up 581%.

•More Extreme. If we look at the top 10 performing NDX stocks in 1999, they were up an average of 559%. The top 10 in the year leading up to 3/24/00 were up an average of 622%. The top 10 NDX names over the last year are up an average of 784%, beating both the dot-com periods..

The S&P is 45% AI and 4% energy.

The market is massively long the output.

Massively short the input.

AI runs on power.

Every dollar flowing into Nvidia eventually flows into a gas turbine, a transformer, or a transmission line.

The market has built a portfolio that ignores its own supply chain.

I wrote about it, in my latest article, link in replies 👇

The S&P 500 $SPY rallied at least 0.25% to a new high.

Not even 40% of its stocks rose on the day.

This has happened two other times since 1962. LOL, make of it what you will.

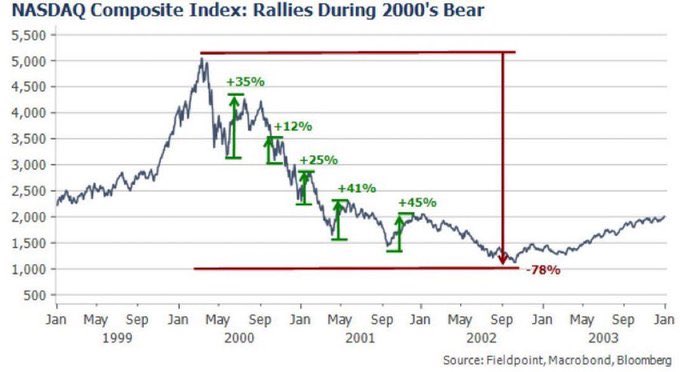

The Nasdaq during the Dotcom crash. 2000 to 2002.

Total decline: −78%.

Along the way:

+35% rally

+12% rally

+25% rally

+41% rally

+45% rally

Every single one felt like the bottom.

Every single one was a trap.

The +45% rally was the cruelest.

It came right before the final collapse.

This is the anatomy of a bear market.

Violent rallies that shake out the shorts.

Convince the bulls to re-enter.

Then resume the decline.

BREAKING: Money market funds posted -$172.2 billion in outflows last week, the largest weekly drawdown on record.

This is +320% above the average April weekly outflow of -$410 billion seen over the last 4 years.

As a result, the 4-week moving average of withdrawals is down to -$30.0 billion, the largest since early 2024.

Some of the outflows were redirected into other assets, with +$11.3 billion flowing into equity funds and +$7.9 billion into bond funds last week.

At the same time, gold and crypto funds each attracted +$1.2 billion in inflows.

The move was also likely tax-related, as April typically sees an increase in cash withdrawals for tax payments.

Market flows are shifting again.

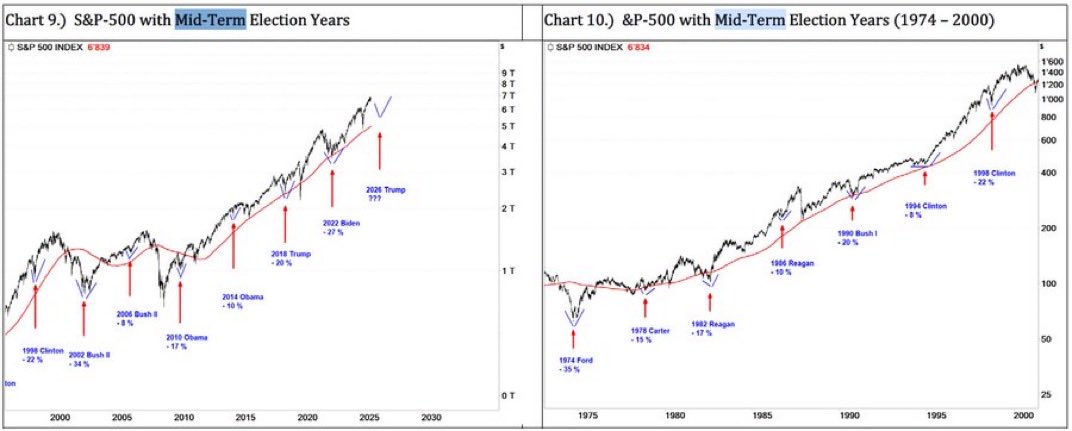

Every single midterm year since 1974.

Same pattern.

1974 Ford: −35%

1978 Carter: −15%

1982 Reagan: −17%

1986 Reagan: −10%

1990 Bush: −20%

1994 Clinton: −8%

1998 Clinton: −22%

2002 Bush: −34%

2006 Bush: −8%

2010 Obama: −17%

2014 Obama: −10%

2018 Trump: −20%

2022 Biden: −27%

2026 Trump: ???

Every single one had a significant drawdown.

Every single one recovered.

The long-term chart kept going up.

The question for 2026 is not if it recovers.

The question is whether you will still be invested when it does.

fucking ruthless lol. now we know why anthropic left the board of figma this week

they built a product that not only replaces them it’s just better

Figma stock is getting crushed on the news and already down 50% this year 💀

claude design

> reads your code base,

> creates a custom design system for it

> uses new opus 4.7 to create design assets

this is 90% of the work designers do.