Anti-Algo slop warchest:

1. https://t.co/y6xNJZP4W4

(Free website for ambient / white noise)

No excuse to get stuck in a loop on youtube looking for background noise.

updated chart showing ratio of VIXEQ to $VIXY which has moved sharply lower after reaching an extreme.

seeking insights on these (nerdy but important) dynamics in markets is why I hope you follow.

there are few indicators of unsustainable price moves better than a sharp "spot up, vol up" episode. Crude in 2008, Gold in 2011, Bitcoin in 2017, the VIX in 2020, GME in 2021, Silver in 2026, KOSPI in 2026... Each of these featured a feedback loop in which the asset rallied sharply and brought much higher levels of implied vol with it.

https://t.co/NU2Fltkx9a

Maybe I’m wrong but I’m not sure how quickly it can go much higher if I am

And if you’re going to take the trade you look for:

- scorching hot jobs print

- scorching hot dc demand

- max buildout exps

- potential AI efficiencies

- broader topping action

- tight credit spreads

https://t.co/V40FxpwRkW

It really does feel like we are in a dark period for this 'industry'. Still probably a space for BTC but imo back in its core thesis and community (and therefore priced lower). Saylor giving up would be something.

Find interesting in the Jeff piece is that himself and others mention they are only still in crypto because of HL. Otherwise they would not be. Its a hot topic with MSTR and WLDFI e.t.c.. Minds far smarter than mine are confirming fears for the future of most these 'assets'

Everyone is buying a car. It seems to be the future of transportation. I should buy a lot of donkeys, they are cheaper.

The Car -> Donkey rotation will be big

TLDR: history tells us that the SK Hynix leveraged ETF may end in tears for long holders. Be careful.

With respect to the the leveraged ETF on SK Hynix, there may be something akin to the price/vol spiral that occurred in $MSTR 2x ETFs back in Nov'24, $MSTU, $MSTX

Below, a 23 min podcast I did on this dynamic at that time.

SK Hynix now has a market cap of 1T USD. The 2x ETF has a market cap of 10bln USD. That's nearly double the market cap that the two referenced Bitcoin lev ETFs had at peak in late Nov'24.

Both products rely on swap counterparties to gain the necessary leverage. In late 2024, it was reported that counterparties to the MSTR and MSTU products were reducing how much leverage they'd extend. It reportedly forced the ETF providers into the options market. This created inelastic demand for options at any price to get the needed delta exposure. Implied vol surged, as I covered in the podcast.

Let's look at some option market dynamics in SK Hynix that trade out of South Korea. Note, the ETF trades in Hong Kong. The first chart is call option volume. The second (top right) is a snapshot of open interest for June 11 expiries. Look at the circled strikes. Below that, tying those open interest levels to recent volume.

Lastly, the recent surge in implied vol on one of those options.

The next pic below is with the help of Claude who read the leveraged ETF prospectus with attention to the hedging protocol. They can utilize options up to 25% of NAV...and well, it seems they may have, according to what they report, also shown below.

If the late 2024 MSTR spiral can inform us about this episode - and I think it does - the SK Hynix 2x ETF provider has played a meaningful role in contributing to the massive realized vol on up days in SK Hynix and has moved the vol market considerably as well.

Last chart shows deviations from NAV. It gets really sloppy when you have to into the options market and put up prints of 100k. You are forcing the seller to make a price on convexity risk that is the equiv of flood insurance in a flood zone. Both prices are going to be crazy high.

The odds of a leveraged ETF on a 100 vol asset succeeding are incredibly low.

And zooming out, if some part of the market's run is simply a wealth effect reinforcing loop, this could reverse some of that quickly. Hard not to think the gains in all of these stocks, not just SK Hynix, are part of the large chip stack being risked in an increasingly loose poker gain.

https://t.co/p9NRNUXiif

TradFi Terminal for @HyperliquidX and @tradexyz is now live.

No up-front costs, supported by a competitive builder fee.

News feed powered by @TreeNewsFeed

People are misreading the savings rate as a vulnerability. When it declines, it is a sign of confidence the economy is improving. You only see contractions when it is rising.

Whenever it has dislocated from my model, it has been early cycle when confidence is improving.

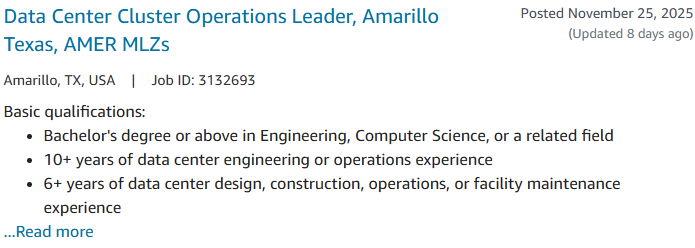

There's a good chance that $AMZN could partner with $FRMI for their build-out in Amarillo

$AMZN posted this job listing for "Data Center Cluster Operations Leader" on Nov. 2025, and they updated the listing 8 days ago

During the dot com melt-up of 1995-2000, Nasdaq put up gains of 572%.

To date, from the 10/13/22 bear market lows, Nasdaq is up just 147%.

Listening to bears calling this a market top could cost you a lot of money.

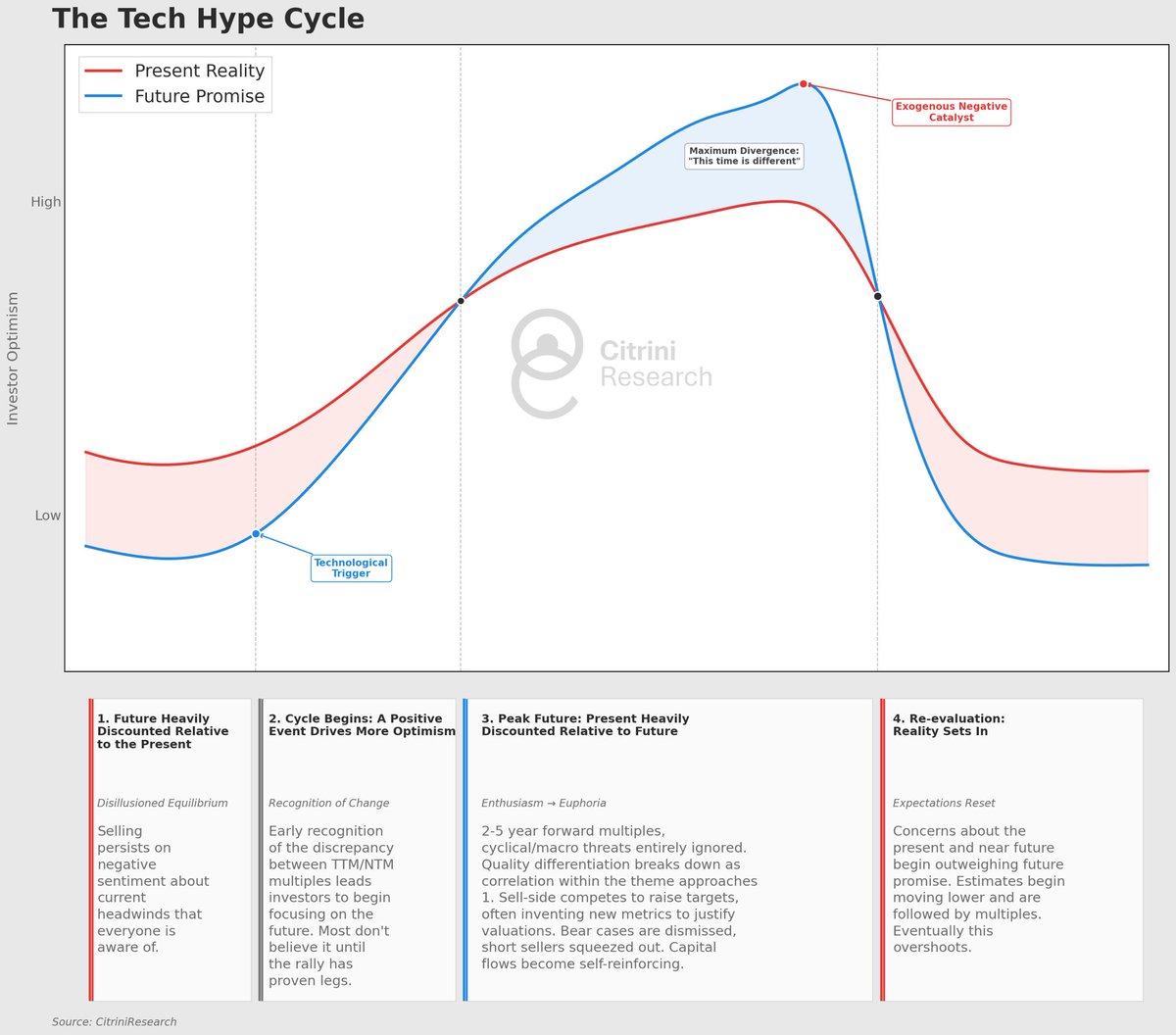

This is how I think about hype cycles in markets. It is basic, but that’s the point (frameworks shouldn’t be overly complex, I think).

Investors are always either discounting the promise of the future or the reality of the present. And they are never equally weighting them.

During the early part of a hype cycle, leading up to and directly following a technological advancement, investors are typically discounting the future while focusing on the present. A good example for this is Nvidia at the end of 2022: investors were solely focused on the headwinds presented by the crypto GPU glut, the anemic gaming PC market and the recent rise in rates causing fears about a near term recession.

Then, as the cycle begins, investors begin to shift to incorporate the future - they stop focusing so much on the present and see the promise. They move out in terms of valuing away from last twelve months current price / current earnings to next twelve months. Then, as price climbs and the technology becomes more exciting, their imagination takes hold. At a certain point they begin discounting the present much more heavily and the future becomes the only thing that matters. Valuation metrics over the next twelve months become useless in favor of 2, 3 or 5 years forward.

At the peak, the present is not considered at all, it is 100% driven by an imagined future (even when that imagination doesn’t necessarily align with a bullish outcome for the stocks driving the rally). Analysts aggressively raise estimates in ways that, at the time, seem fundamentally justifiable (if you take the assumptions at face value - for example, “everyone in the world will have two cell phones” was a good one from the mobile phone hype cycle). Capital is sucked in which ultimately forces performance chasing and crowds stocks with money that doesn’t really believe in the thesis. “A twilight period where people continue to play the game, but no longer believe in the rules” emerges, as Soros put it.

The valuation of SaaS stocks in mid-2021 is a great example of what happens when the future is overvalued relative to the present - nobody cared about climbing inflation, that rates had nowhere to go but up, that these companies were reliant on ZIRP or that software could become more competitive.

Then, a negative catalyst occurs - this can but doesn��t have to be related to the technology, macro, credit, underwhelming earnings. The estimates start to seem unattainable, and the present begins to matter more when the future seems more uncertain. That exact mechanism that drove future optimism to unsustainable heights mechanically reverses, everyone needs out. The future begins to be discounted until it results in a sense of disillusionment with not just the stocks but the technology itself. This overshoots to the downside, investors eventually become disillusioned and seemingly allergic to anything having to do with the technology. This happens in a very asymmetric manner to the climb (“stairs up, elevator down”).

This is the crucible in markets for truly transformative tech. If advancements persist, another opportunity to get long presents itself before capital once again begins flowing into the companies (the internet, for example). If they don’t - not necessarily “the tech goes away” but rather that it ceases to advance once the capital isn’t free or plateaus or the economics prove to be unfavorable - the cycle will still start again, just with a new technology.

Or maybe not…maybe this time is different.