For nearly 50 years the standard of care for joint sprains has included rest, ice, and ibuprofen not bc rigorous evidence showed that worked, but bc that made intuitive sense and seemed to help. Now there's good evidence those actually impede recovery.

Add it to a long list of medical reversals, whereby a practice that was once widely adopted is later shown to be ineffective or even harmful.

Promising theories, observational evidence, underpowered studies, and early experimentation can generate important hypotheses. But they do not eliminate the need for rigorous randomized trials, regardless of the financial or professional incentives to move faster.

Once ineffective or harmful care becomes embedded in standard practice, it is very difficult to overturn. There is a role for regulatory flexibility and clinical experimentation when patients have unmet medical needs. But neither eliminates the need for rigorous evidence to ensure that the medical system is actually helping patients.

OUSD enters a $311B market where Tether (60%) and USDC (24%) hold ~84% of supply.

The three biggest single-issuer coins (USDT, USDC, PYUSD) stayed out. Nearly everyone else piled in, including Coinbase and BlackRock, USDC's own distributor and reserve manager.

Better tech never dented the Tether-Circle duopoly. Owning the rails might.

Can 140+ giants finally crack it?

1/ BUFFETT'S #1 RULE ISN'T "BUY LOW, SELL HIGH."

Most people misquote it.

The actual rule is what kept him out of every bubble for 50 years.

Here it is🧵

Just listened to @FoundersPodcast #100 on Warren Buffet. The book was the Snowball in this case.

Couple of things:

1. love how David Senra is able to read about people and learn from them: both the good & the bad

2. Recognizing focus is a superpower AND it can also ruin you

I'm not the biggest fan of Warren Buffett and I still have plenty to learn from him.

Motivated me to read the shareholder letters. They are online for free as pdf's. One can also get the book. Hardcover is pricey, but is available on kindle for 3.99

https://t.co/mJwYXHpxUN

Outside of being a participant in this game, I’ve always been a student of it as well.

Growing up in the business, my first mentor was a gentleman who ran a firm that directly competed with the O’Connor guys long before my time. Both firms traded with similar philosophies, but O’Connor went on to become legendary in the derivatives world.

O’Connor became the breeding ground for some of the best volatility traders on the planet. Alumni from the firm eventually spun out and built powerhouse trading shops like Peak6, Wolverine, CTC, and many others. If you came out of O’Connor, there was a reputation attached to your name. You knew how to make money trading volatility.

The firm was built on old school derivatives prop pit culture. Extremely intelligent people, but even grittier competitors. Eddie O’Connor came from a tough background and attacked the pits with aggression, instinct, and an elite understanding of discretionary trading. The guy was savvy and knew how to wear risk. He printed money for years. But the firm evolved into something even more dangerous when he hired, seeded, and partnered with Michael Greenbaum to formally build O’Connor & Associates.

Greenbaum brought a deeply mathematical framework to the business and helped optimize volatility ideas into scalable models. It became the perfect marriage between pit instinct and quantitative rigor. That combination created a machine.

What made the culture special was the philosophy they drilled into traders. A philosophy that every great volatility business eventually arrives at: Make a little money consistently in normal markets by trading flow and pockets of edge, but absolutely blow the lights out whenever volatility goes into chaos.

Every risk taken sat within that framework. Greenbaum believed in “ALWAYS” maintaining long gamma exposure so the firm had the convexity to capitalize on outsized dislocations. That principle became deeply embedded into the DNA of the traders who came out of that ecosystem. It’s why so many alumni carried the same philosophy into the firms they later built themselves.

It’s no surprise O’Connor survived 1987 while many others were wiped out, despite carrying relative value exposure in parts of the book. It’s no surprise those Chicago volatility prop desks crushed environments like 2001, 2008, and 2020. They understood that the real money in this business is made during periods of disorder and panic.

Working under Rob, this same philosophy was hammered into my head from an early stage. That old school framework of volatility trading never left me, and it became foundational to the way I built my own firm. It is a principle I will never move away from.

Some of our investors and close trading relationships today are former O’Connor guys. There’s a natural synergy there because we think about volatility, convexity, and risk in very similar ways. In exchange for making them money, I get the privilege of listening to old war stories from eras of trading I wasn’t even alive to experience lol.

With all due respect, once UBS acquired the firm, it simply was not the same culture anymore. And in this business, culture matters. The edge is never just the model. It’s the mindset, the philosophy, the risk framework, and the people carrying it out.

I genuinely hope that in some small way, Ambrus can continue carrying a piece of that old lineage forward. The style, the culture, the obsession with convexity, and the mentality that defined those legendary volatility shops.

When people talk about the great firms in derivatives history, O’Connor often gets skipped over. Slowly it’s becoming a forgotten firm. But make no mistake, those were the guys who printed money for decades and ultimately sparked the creation of many of the volatility trading firms the street idolizes today. 🫡

@ferueda@JrdnMcFarland@SahilBloom which then gets flipped to the positive action items:

1. be on time for appointments

2. pick which are the important projects

3. actually to those important projects

you don't stay in the negative state. you use those to figure out the positive state.

@ferueda@JrdnMcFarland@SahilBloom i agree. he might say if i want to be successfully, then i think about what would failure *look like*

That would look like: not being on time for appointments, not accomplishing the things that i sad i would do, and volunteering to do too much.

The gamma trap: how traders extract real money from a strategy that's a long-run loser.

ex-Tudor PM Tom Costello (@tcoste110) explains:

"Gamma hedging is much more difficult than it looks. It's not simple."

"You can sell options for the premium and make money 99 days out of 100. For 98 of those 99 days, you're sure you're brilliant."

"You don't make much money every day. But you make it every day. So just multiply your size by 10,000. You think you've cracked the code."

"You haven't cracked the code. You've compressed your risk. You've traded a fraction of a percent gain every day for a 150% loss on the 99th day."

"Average it over years — you're a loser."

"But on the way up, you get paid. Year one you get paid. Year two you get paid. Year three you lose more than you made in the last two."

"Net loser overall. But you still got paid. Maybe you get fired, you go to another shop and do the same thing over again."

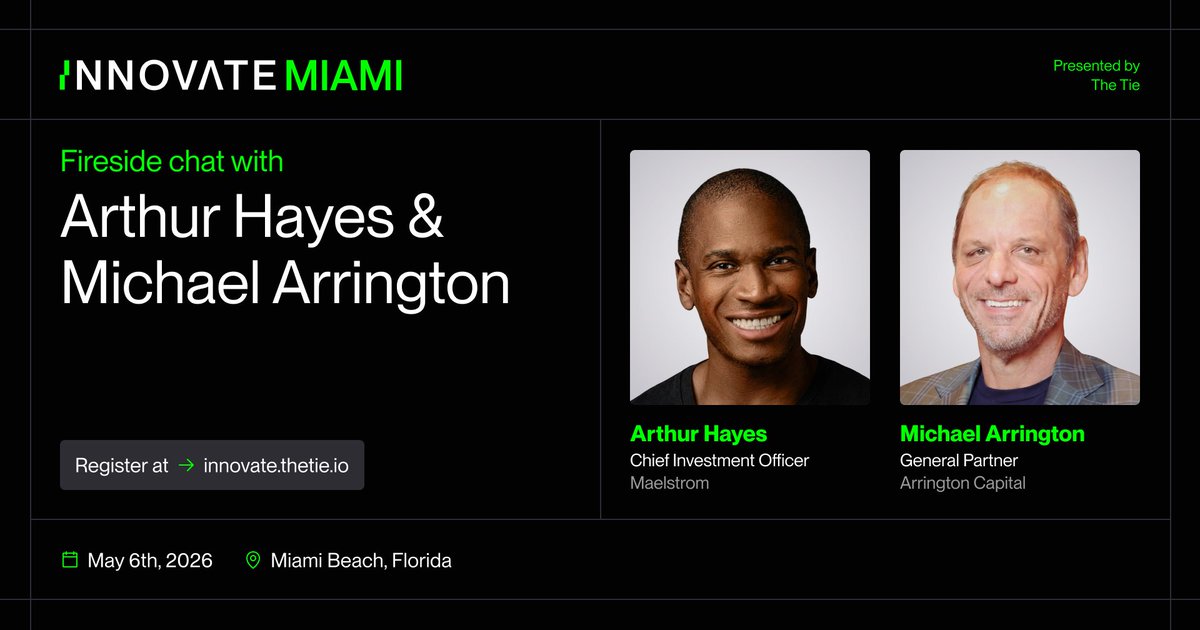

Join @CryptoHayes (@MaelstromFund) × @arrington (@Arrington_Cap) — live and unfiltered.

Two of the most influential voices in crypto and finance go deep on geopolitics, macro, and digital assets.

No scripts. No filters. Just signal.

Register now so you don’t miss it: https://t.co/jfOUk03pdz

Meet Owen B. Gloom.

He’s 11. He’s an aspiring influencer. His parents are retired vampires.

And he’s documenting all of it.

Owen Nowhere - a new animated comedy, only on LAMINA1. 🎥

"China. Russia. India. If they align, the next global boom may not belong to the US."

Louis Vinent-Gave @gave_vincent (Co founder and CEO, @Gavekal) on the macro shift he believes markets are ignoring:

"If you live in the Western world today… AI is the macro trend that you hear about all day, every day."

"But there’s other potential macro trends out there."

"China and India seem to be committed to repairing their relationship."

"Russia produces the world’s cheapest commodities. China produces the cheapest capital goods. India has the world’s cheapest labor."

"You match cheap capital, cheap commodities, cheap labor — you have the making for a potential explosive boom."

"Today you buy the world MSCI, you’re essentially buying 70% United States."

"It’s not priced anywhere."

The question: If the next economic explosion is Eurasian, not American, who is actually positioned for it?

Something caught my eye in the latest 13F filings.

The biggest new entrant into IBIT, from a brand new entity, is something called Laurore Ltd. No website. No press. No footprint. The only public information is that the filer's name is Zhang Hui and it's HK based.

Let's double click on that for a second.

Zhang Hui is the Chinese equivalent of John Smith. It's what I like to call it a "non-anonymous anonymous" name, something hiding in plain sight buried under the statistical weight of millions to make it untraceable. The "Ltd" suffix suggests a Cayman or BVI structure, the classic offshore wrapper for accessing US markets. And the portfolio? A single holding. Nothing but IBIT. This isn't a diversified fund. It's a $436 million Bitcoin access vehicle dressed in institutional clothing.

Why would you do this?

Because Chinese investors can't hold Bitcoin.

If this is what it looks like, it might be an early sign of institutional Chinese capital moving into Bitcoin, not through crypto exchanges or gray market channels, but through a BlackRock ETF, filed with the SEC in a regulated jurisdiction hiding in the most "transparent non-transparent" place imaginable.

Funny that the name Laurore likely derives from the French l'aurore: the dawn.

Smells like capital flight to me.

@KrisAbdelmessih know this, which is true. They also know that people like selling them.

anyway, this is not investment advice. and betting/investing on low probability outcomes (even with edge) is significantly more tricky than would seem obvious from a positive EV situation

I was just reading @KrisAbdelmessih whatever they call it on Jensen's inequality here:

https://t.co/lzeGxLxWAX

there is plenty of value there, but i grabbed one little nugget here to tie back to work that both Kris & @harvested_dafe did

@KrisAbdelmessih of Kris's article. which is Jensen's inequality is both 1) true and 2) hard for humans to wrap their brain around.

which has the suggestion that OTM options have the greatest opportunity to be mis-priced

and before one says that market makers like SIG/Citadel ...