If legislators always vote with the President, we have a king.

If legislators always vote with the prevailing wind, we have mob rule.

If legislators always vote with the Constitution, we have a Republic.

Milton Friedman: “I am not a conservative. I’ve never been a conservative. Hayek was not a conservative.”

“We are liberals in the true meaning of that term: concerned with freedom. We are not liberals in the current distorted sense—those liberal with other people’s money.”

Thinking through oracle design for on-chain parametric insurance.

Key insight: the oracle shouldn’t model risk or price anything.

It should answer one question — did the predefined trigger occur?

Simple, deterministic settlement beats complex oracle games, especially early.

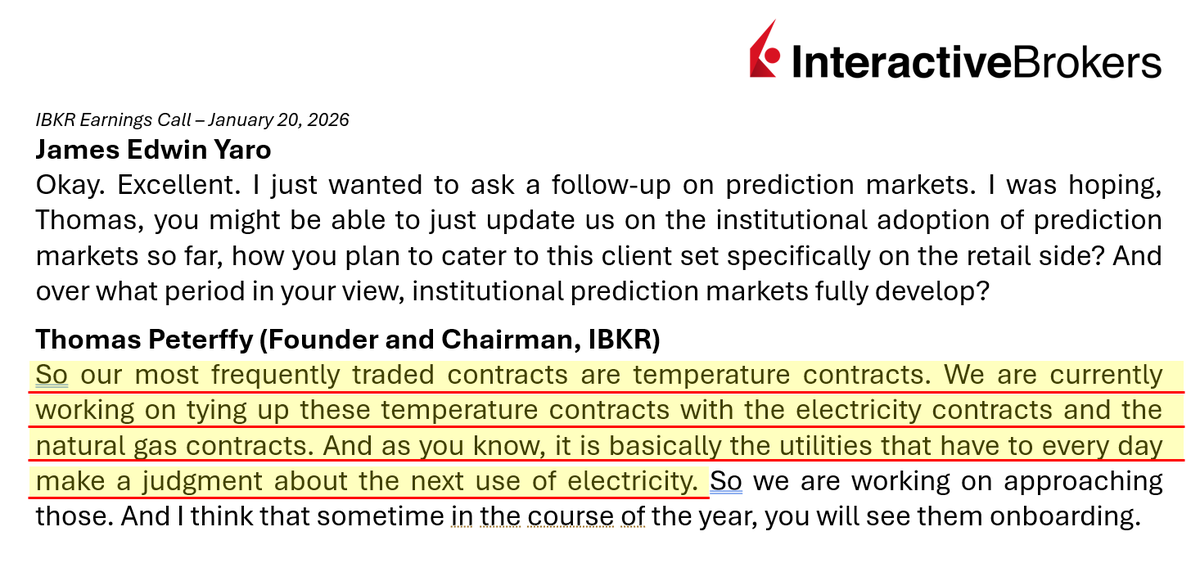

To everyone who said prediction markets are just sports, here’s the CEO of a $110b company:

1. Weather and temperature contracts are the most frequently traded

2. Utilities will soon hedge electricity and natural gas contracts using these markets

Prediction markets are already institutional

You’re just not paying close enough attention

I want to build a minimal onchain insurance contract.

The takeaway: don’t rebuild the product onchain. Just mirror what must be trusted — immutable trigger definitions, issuance caps, explicit capital layers, and deterministic payout logic.

Want to help/learn more? DM me!

Planning on how to bring a parametric insurance MVP onchain without rewriting it later.

Key realization: don’t move everything onchain.

Only mirror what’s deterministic and trust-sensitive—trigger definitions, capital accounting, issuance caps, and payout execution.

A quiet insurance lesson: most ideas aren’t rejected because they’re risky — they’re rejected because the risk isn’t clearly bounded.

The fastest way to lose credibility is to lead with confidence instead of failure modes.

Insurers trust people who explain how things break.

Bitcoin backed dollars for the onchain era.

Lock $cbBTC, mint $gynUSD, and unlock liquidity & yield on Base without ever selling your Bitcoin.

Welcome to Gyndore.

Another quiet insurance lesson: time is a risk dimension.

Seasonality and exposure overlap matter more than annual averages.

A single event hitting many active policies is one correlated shock—not many independent losses.

Survival isn’t about “more capital,” it’s about structured capital.

Tranching exists so frequent losses don’t threaten the whole system and tail risk is absorbed intentionally.

One of the biggest insurance lessons: expected value isn’t enough.

A product can have positive EV and still fail due to tail risk and loss clustering.

Insurance doesn’t break at the average — it breaks at the extremes.

Parametric insurance doesn’t fail because of basis risk — it exists because of it.

You’re trading perfect loss matching for speed, clarity, and certainty.

The real question isn’t “can we eliminate basis risk?” but “is the tradeoff intentional and explainable?”

The biggest pushback I had on prediction markets + insurance is “isn’t this just gambling?”

The framing that’s helped me: insurers already watch market signals (cat bonds, reinsurance pricing) to gauge risk.

Onchain markets just make that signal more transparent — not decisive

Thinking more about how to host productive conversations between insurance and crypto folks.

Framing: we’re not automating insurance — we’re exploring how onchain signals might help insurance systems react faster to changing risk.

Curious what questions you’d want discussed.

How to explain prediction markets + insurance?

The cleanest framing so far: markets don’t decide outcomes — they surface changing confidence around objective events.

Used carefully, that signal can complement parametric insurance without replacing models or claims logic.

Prediction markets don’t replace insurance logic — they surface confidence shifts around objective events.

Used carefully, they can inform pricing, underwriting pace, and capital buffers in parametric insurance, much like cat bond spreads or reinsurance pricing already do.

For insurance, the real prediction market MVP is proving judgment.

Clear parametric triggers + baseline models + simulated market signals are already enough to test whether an idea makes sense — long before capital or users.

Insurers already rely heavily on market signals—cat bond spreads, reinsurance pricing cycles, weather derivatives—to gauge risk in real time.

Prediction markets aren’t radical in that sense; on-chain just makes the signal more transparent and programmable.