Former Central Bank of Kenya Governor, Prof. Njuguna Ndung'u, reflects on his fallout with the International Monetary Fund (IMF) over Kenya's monetary policy framework.

He makes the interesting case of the twin occurrence of high growth (>7.0%) & high inflation (13.0% - 14.0%) while the Fund's prescription was monetary tightening amidst static velocity of money.

"I told the IMF that I am not a spanner boy"

Credit: Central Bank of Kenya (@CBKKenya)

Over 40 Kenyan companies are set to close after applying for bankruptcy in the nine months to March 2026, up from 24 in the same period in 2025.

.The increase is due to weak demand, cash flow problems and delayed payments

While you’re busy celebrating roads outside your docket, armed goons are robbing Kenyans at gunpoint. Chaiwali on General Mathenge Road tonight. Your ministry’s report card is written by the safety of Kenyans not by road projects. Armed robbers struck hotels and roads on a broad day light. Maybe secure lives before chasing credit.@NPSOfficial_KE@DCI_Kenya@C_NyaKundiH@NelsonHavi@omwambaKE

Money lenders can now call KRA bro.

Because starting 1st July 2026,

Finance Act 2026 has ended one of the biggest tax fights between KRA and money lenders.

For years, banks, microfinances and digital lenders have fought KRA in the Tax Appeals Tribunal and superior courts over one simple question.

A loan has two parts.

• The principal, and

• The interest.

Take for example a lender who gives out a loan of Ksh 1 million. At an interest of Ksh 100,000.

Then the borrower disappears. And all recovery efforts fail.

The lender finally gives up and writes off the loan.

The question is,

• What amount should the lender deduct for tax purposes?

- Is it the principal of 1 million? Or

- The interest of KSh 100,000?

- Or both?

KRA's position has traditionally been,

- Only the interest qualifies as a bad debt deduction. The principal does not.

Money lenders argued the opposite.

- The principal is our stock. That's what we trade with. If the principal is lost, that is a genuine business loss. It is tax deductible.

This disagreement has generated some of the fiercest tax battles between KRA and lenders.

One of the most notable being Branch International Ltd v KRA, involving over Ksh 800 million in loan write offs.

Finance Act 2026 has now settled the war.

�� It expressly provides that, for banks, licensed financial institutions, microfinance institutions and money lenders, a bad debt includes:

- The principal.

- The interest.

- And any other amount relating to the debt.

KRA and lenders can finally call each other buddies.

Meanwhile, the professional loan defaulters have entered the chat. They are asking,

So if Tala or Branch writes off my loan as a bad debt, does that mean KRA has carried the burden for me? Should I still repay?

Tax waiver has kicked off in Kenya.

Starting today, 1st July 2026, the tax amnesty introduced by the Finance Act, 2026 has officially taken effect.

• How does it work?

KRA shall delete your tax penalties, interest and non-compliance fines,

Provided you pay the principal (actual tax) due.

• What period does it cover?

It covers tax liabilities that arose on or before 31st December 2025.

Under one condition.

- You must clear the principal tax before 1st Jan 2027.

Example.

Say your actual tax bill for 2020 was Ksh 100,000.

You did not pay it because of cash flow challenges.

Over the years, penalties and interests have accumulated to Ksh 30,000.

If you pay the Ksh 100,000 before 2027,

KRA shall take the rubber, and erase the 30,000.

• One question many people are asking:

- Will KRA also waive the penalties for late filing of your 2025 tax return late?

The answer is: Yes.

• So what should you do?

• Check your iTax ledger immediately.

• Identify the principal tax outstanding.

• Pay the principal tax.

• Leave the penalties, interest and fines untouched.

KRA shall erase them.

A normal family of 8; 5 kids, dad, mum & house help requires KES 5000 a day to live a comfortable life. This roughly comes to KES 155,000. This is on food alone, eating eating on average twice a day.

Now we all know we are not living comfortably. We are basically surviving. The value of KES 1000 has dropped to KES 10.

All these is blamed on the incompetent economic, taxes & political policies of this government of Ruto & blantant theft of public resources.

We have done a summary of the proposals that were rejected by MPs, why they were rejected, and the proposals that were passed.

Here is the deeper thread.

Save and share.

To save with a SACCO or a MMF?

In a MMF, you can withdraw your money within 2 days.

For a SACCO, you can only access your savings by taking a low interest loan.

For a SACCO, you make money through dividends earned from share capital and interest on your deposits.

For MMFs, you only make money from the interest on your deposits.

A MMF is more liquid and used for capital reservation in the short term.

A SACCO is more illiquid and is used mostly to access low interest loans on friendlier terms

Finance Bill 2026 wants to forgive your sins.

It proposes to waive:

• All penalties, interest and fines on tax arrears up to Dec 2025.

But on one condition. You must pay the principal tax by end of this year, 2026.

This is a welcome proposal.

It gives everyone a fresh tax start.

Most Kenyans keep their savings in a money market fund and call it "investing."

There's nothing wrong with that, but if you want real wealth building, you need to own a piece of Kenyan businesses.

Here's how to build a serious stock portfolio on the Nairobi Securities Exchange. 🧵

Finance Bill 2026 wants to tighten eTIMS.

Under the proposal:

If you fail to issue an eTIMS invoice,

KRA can charge you:

• 2X the tax due

• Minimum 100K penalty for companies

• 10K penalty for individuals

But it gets deeper.

• Any expense without an eTIMS invoice is automatically disallowed. KRA has no power to accept manual non etims expenses.

Meaning:

- If you buy stock say from a farmer

- Farmer doesn’t issue eTIMS

- KRA ignores your cost

- Taxes you on fake profits

And now:

• Businesses making above 5M in yearly sales shall be forced to integrate their systems with KRA.

Meaning:

- KRA wants a live feed of your transactions

- This is live tax audit

Lesson:

• Deal only with eTIMS compliant suppliers

• Or prepare to donate money to KRA

Nearly half of the 2026/27 budget of Sh4.8 trillion, Sh2.3 trillion will go to debt repayment.

This will force Kenya to opt for more borrowing or cut spending on development and services.

KRA is not playing with KTDA.

KTDA buys and sells tea leaves. Not tea. Tea ni chai. Chai ni ya kukunyua. Tea leaves ni majani ya chai. Kirui are we together?

Now,

KTDA was growing very fast. They wanted the Gulf people to taste the classical definition of proper Kenyan tea.

In 2008, they opened a branch in Dubai. Branch role, to market and sell tea in the Gulf.

In this setup, KRA was eating well. Because branches are like agents. They sell and send all profits back home.

So Dubai sold tea. Profits came back to Kenya. KTDA consolidated everything. And handed KRA a biig fat cheque.

KRA was extremely happy.

In 2014, KTDA got tired of tickling KRA.

They discovered.

- If they register a separate company in Dubai

- Gulf profits won’t be taxed in Kenya

- And Dubai tax was 0% too

So no taxes nowhere.

Directors said: Perfect. Do it. Fast!

As they are doing all this, they are unaware of one dangerous sentence sitting quietly in Kenyan tax law.

It reads:

• Any company managed and controlled from Kenya is a Kenyan resident company.

The Dubai company was registered. Life was good. Money was flowing. Zero income tax.

Next year, KRA noticed their cheque suddenly got thinner.

They asked KTDA Kenya, ndugu ni nini inaendelea hapa?

KRA got the shocking news of its life from KTDA.

- We do not have a problem paying taxes. But the Dubai branch has been upgraded to a full Dubai company. And profits are no longer coming home to be taxed.

KRA could not believe it. It returned to Times Tower. And embarked a fault finding mission.

In 2021, they found out:

- Directors of KTDA Dubai were all Kenyans

- They lived and drank tea in Kenya

- They controlled every single affair of KTDA Dubai from Kenya

Wakasema baas, nini ingine tunatafuta?

They invoked the one dangerous sentence. You remember it?

• Any company managed and controlled from Kenya is a Kenyan company.

KRA declared KTDA Dubai a Kenyan company

• Tax demanded 122M

KTDA ran to court with Dubai registration papers.

The judges questioned KRA why it wanted to harvest where Kenya did not plant?

KRA responded: My Lords, if your hen lays eggs in your neighbour’s land, is that egg yours or your neighbour’s?

Judges paused.

Then sided with KRA.

KTDA wakaabiwa walipe tax.

Case closed.

Lesson.

• Structure your offshore company properly.

• Or KRA will structure it for you.

Bwana KRA imetuweza.

- The very returns we filed in 1 day now take 2 weeks min. to complete.

• Scan and upload receipts

• Prepare a csv for all those receipts

• Hunt for supplier's KRA PIN

My goodness!

How are you all accountants surviving?

Kenyan tax law is tricky, and sometimes entertaining.

There are guys called H-N-F.

High Networth Freelancers.

They earn in dollars. Think in dollars. And price everything in dollars.

They have made life particulary difficult for agents. I heard one casually say.

- I get the rent is Ksh 180k, but how much is that in dollars?

And before the agent could reach for the calculator. He told him to forget about it.

But now,

In Kenya, taxes are crazy.

A freelancer earning 10M annually,

Pay taxes worth 3M shillings.

• That is 30%.

They do not like that. So they get creative.

They look for low-tax countries:

- Dubai, Mauritius, cayman islands, etc.

They register brief case companies there.

- As sole directors & sole shareholders.

Clients pay directly to those companies.

The company pays Zero or very low tax.

• Then sends money to Kenya as dividends. Withholding tax about ~5%

- So tax drops from 30% to 5%.

Same 10m. Tax now 500,000.

But unknown to them. There is one dangerous sentence chilling quietly in Kenyan tax law.

It reads:

• Any company managed and controlled from Kenya, is a Kenyan resident company.

Meaning:

- You own the company in Cayman

- But run it from your laptop in Nairobi

That is a Kenyan company.

And Kenyan companies must pay Kenyan taxes.

So one day KRA audits the freelancer. He pays zero taxes in Kenya.

He says he earns dividend from his Cayman company.

KRA asks for the registration documents. And finds he is the sole director.

- KRA Taxes the company in Kenya

- Adds penalties for tax evasion

- And goes for him as the representative to pay

Lesson.

• Structure your offshore company properly.

• Or KRA will structure it for you.

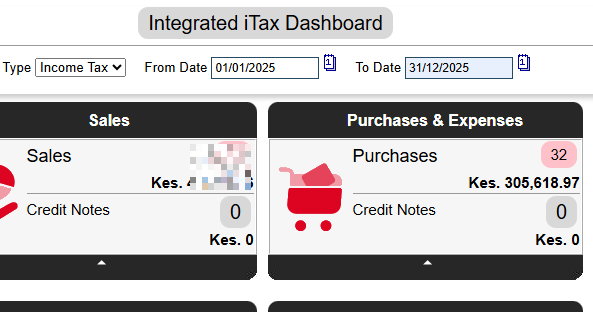

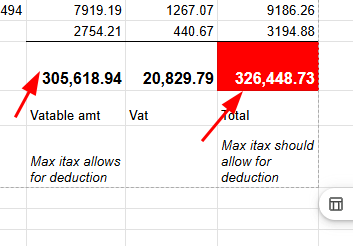

Hello @KRACare@KRACorporate,

Please, pass this to your devs.

- For a taxpayer out of vat category. They expense all vat charged on their purchases. Because they cannot claim it as input vat.

- But, itax only allows the deduction of the base amount without vat.

- This makes one pay more tax than they should.

Please fix it to allow deduction of vat component.