This past week, the Federal Housing Finance Agency officially blew up $FICO's decades-long monopoly. They announced that Fannie Mae and Freddie Mac will immediately accept a rival credit model, VantageScore 4.0. This caused FICO's stock to tank hard but it already made a solid recovery.

FHFA Director Bill Pulte and HUD Secretary Scott Turner officially announced that approved lenders can use VantageScore 4.0 right now. FICO's own modernized score, FICO 10T, is delayed. Its historical data will not be fully released to the market until this summer. This gives VantageScore a massive head start. For the first time in history, mortgage lenders do not have to pay FICO a toll to close a standard conforming loan.

In the last few years, FICO aggressively hiked its wholesale prices, pushing the cost of a tri-merge credit report from under $2 in 2022 to roughly $30 in 2026. Senator Josh Hawley has been aggressively going after FICO. He sent strict letters to the DOJ and the FTC demanding antitrust investigations. He explicitly called out FICO for doubling its per-score price to $10 in 2026 alone, arguing these hikes crush first-time homebuyers. The political heat is real, and it likely caps FICO's ability to just raise prices whenever it wants.

$EFX is subsidizing VantageScore 4.0 to make it cheap at $4.50. In response, FICO is started a wild new strategy. They proposed dropping the upfront cost of a score to just $0.99, but adding a hefty success fee of around $60 to $65 on the back end when a mortgage actually closes. Director Pulte is already publicly discussing the hope for a 99 cent pricing model. This is a smart defensive move by FICO. It stops the political complaints about high upfront application costs, but it makes FICO's revenue highly dependent on actual closed loan volumes instead of just application pulls.

Now, let's not forget... FICO has massive structural advantages. The secondary market controls everything. Wall Street buys Mortgage-Backed Securities, and they hate uncertainty. FICO has decades of performance data that survived the 2008 financial crisis. Institutional investors will likely demand FICO scores to feel safe. FICO also still has a total stranglehold on credit cards and auto loans. And FICO is deeply embedded in bank infrastructure through its enterprise software platform, which boasts a massive 122% net retention rate. Banks do not easily rip out core software.

FICO is transitioning from an unregulated monopoly to something a little more regulated. The massive drop in FICO's stock price is finally pricing in the DOJ antitrust risks and the end of infinite price hikes. However, FICO's deep roots in Wall Street securitization and global banking software mean they will remain a cash-generating fortress.

I spent a couple hours looking at some of these recommendations, and I have added $RMS.PA $TDG $RACE and $ADP to my watchlist for the time being. I'm gonna do some more research on these in the near future, and begin following these companies closer as they all look like appealing businesses.

Still have more recommendations to take a look into, but I appreciate everyone that left recommendations for me.

Thank you!

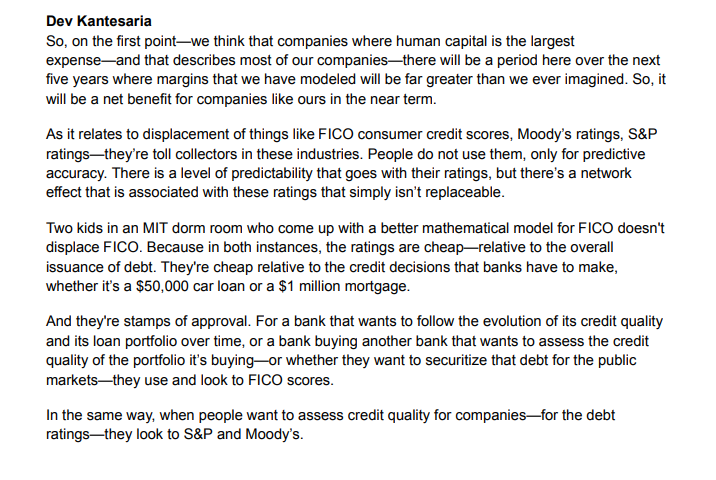

Dev Kantesaria on how AI will affect $FICO $SPGI $MCO

"As it relates to displacement of things like FICO consumer credit scores, Moody's ratings, S&P ratings- they're toll collectors... they're stamps of approval."

$FICO This company has unparalleled pricing power. In fact, increasing prices by 725% for their FICO scores in a couple of years put them in the crosshair of the FHFA (Federal housing finance agency).

However, they just found a way to increase their price by another ~700% in a single year! The best part is that they operate such a systemic moat, that even when their competitors offer their product _FOR FREE_, no institution switches over from FICO.

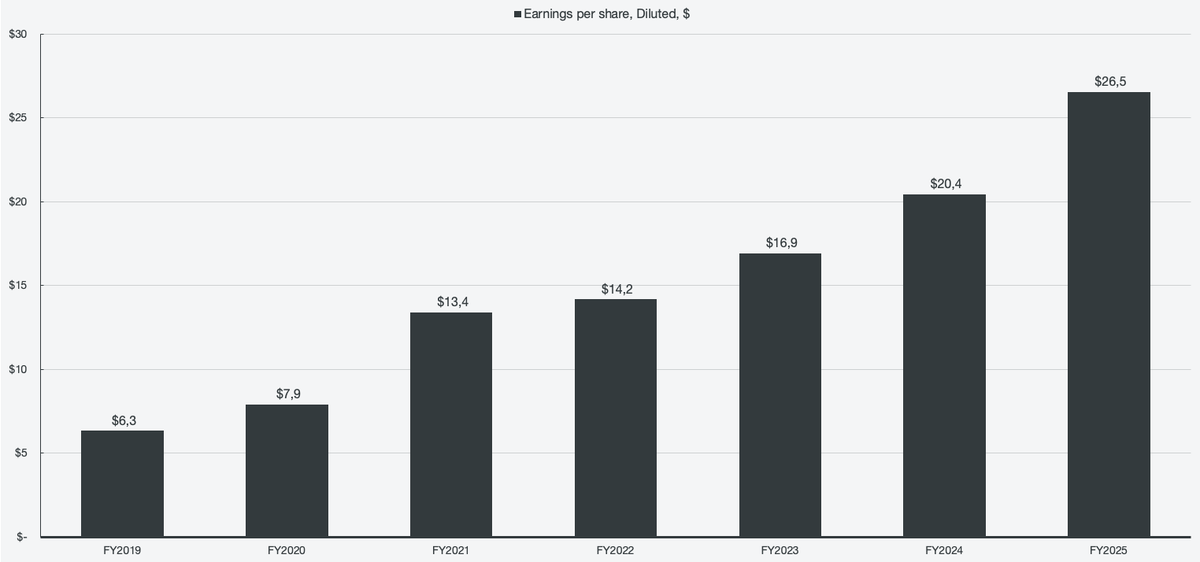

This is the kind of company that comes to mind when people say things like "compounding" machine. Ever wondered what that looks like? Well, here, I'll show you. 26% compounded EPS growth despite the past years being the bottom of the cycle (high interest rates, housing crisis).

The best part about FICOs score segment is that it is so unbelievable capital light, that their MASSIVE 88% operating margins are almost all converting into FCFF.

Now imagine another ~700% price increase; what that would do for revenue- and earnings compounding.

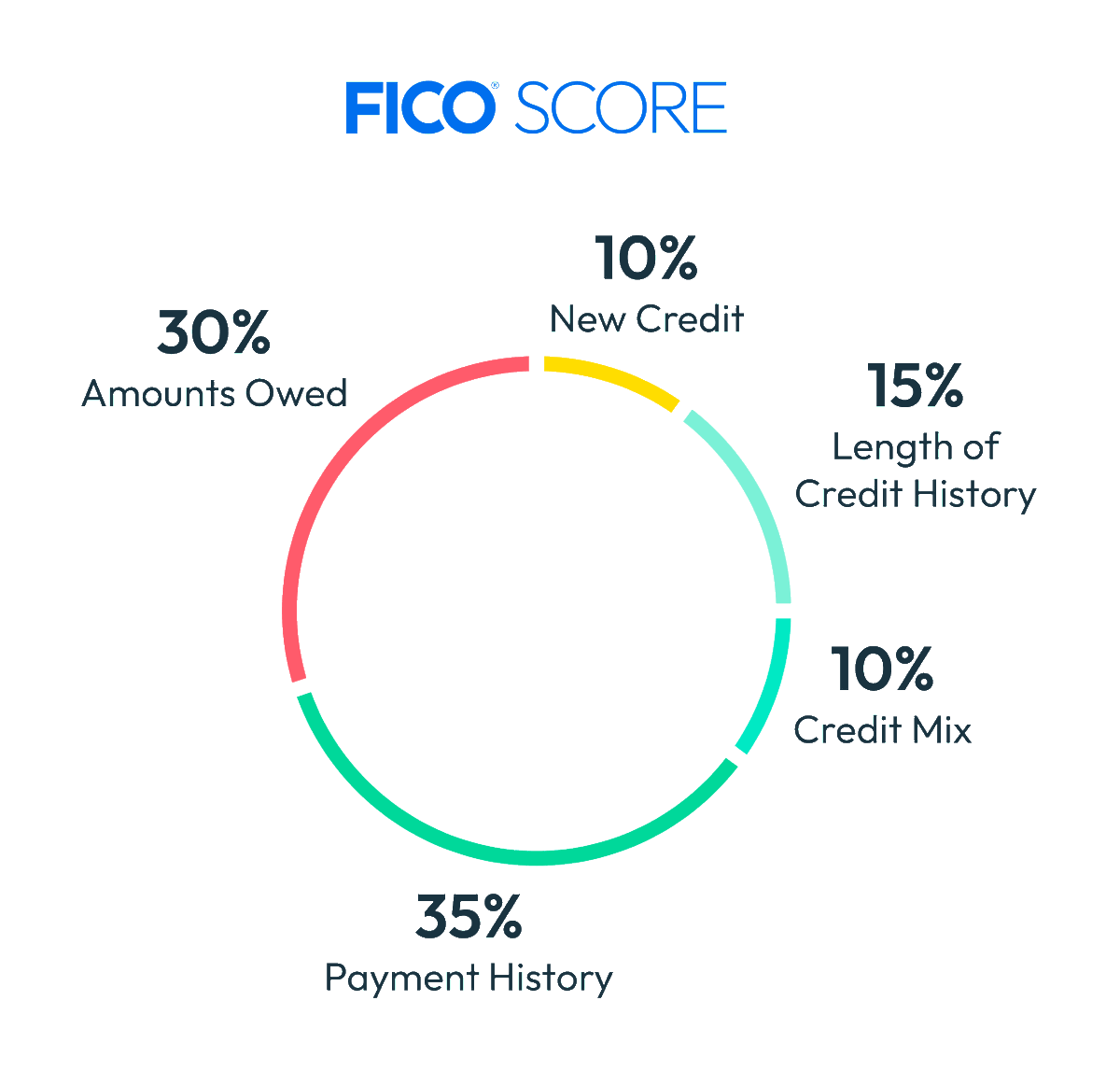

To understand how their pricing power is so immense, we first need to understand how it works when a FICO score is pulled. It is quite simple:

1. Consumer inquires about a loan to a lender

2. Lender pulls a FICO score from the 3 credit bureaus (equifax, transunion, experian).

3. The credit bureaus have the consumer data, but need to get the mathematical scoring model from FICO.

4. FICO provides the scoring model and collects a royalty from each of the 3 bureaus.

The royalty was fixed at $4.95 in 2025, up from $0.60 in 2018. That's where the 725% increase comes from. However, what is $4.95 (or ~$15 on a tri-merge basis) in the grand scheme of overall mortgage closing costs? Pennies, unnoticable. FICO could increase the royalties much further, and it would still be a drop in the bucket compared to hundreds of thousands, if not millions of dollars borrowed.

The FHFA targeted FICO for their pricing power, blaming them for causing the housing crisis due to their price hikes, saying it deters from getting a mortgage. The truth of the matter is that the FICO score cost is immaterial, and only represents a tiny fraction of overall mortgage costs.

- In a $500,000 home sale example, a FICO score needs to ben pulled 2000 times to equal a realtor commission at 6%.

- If the mortgage broker charges 1.8% in fees, FICO score would need to be pulled 600 times to equal the broker fee.

If the FHFA wants to combat expensive housing markets, FICO is not the target as it only represents 0.003% of the closing costs in the $500,000 example.

So what did FICO just do to allow them to increase their prices by another ~700%? They combat the FHFA by launching a "direct license model". This offers two transparent options for a lender:

- A flat $4.95 fee, with a $33 funded loan fee if the mortgage closes (670% increase in price)

- Flat $10 per score, no funded loan fee (100% increase in price)

The reason this works is because this is transparent in the invoice. It is clearly outlined what the cost for the FICO score is, as opposed to a bundled cost from the credit bureaus where they apply their own margin, often 5-10x the cost of the FICO score itself. Resellers are used for the direct license model, and the 3 credit bureaus still receive a fee for providing their data, but they aren't able to hike the prices massively with their own margin.

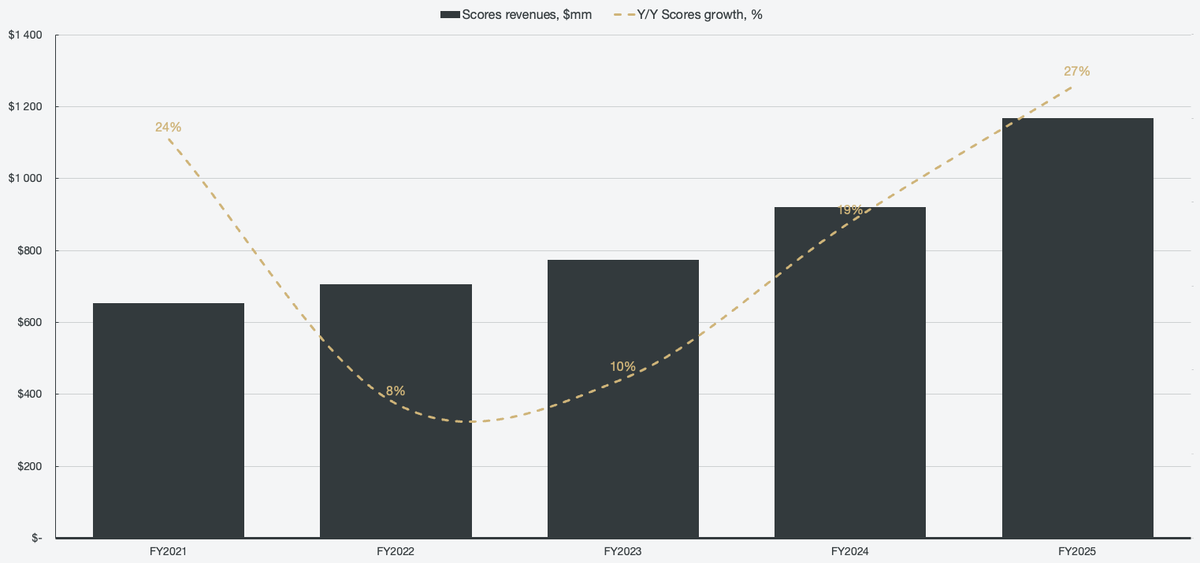

Scores revenue grew 27% in 2025 after exiting the bottom of the cycle in the years prior. With the new pricing model, I expect we may see an extreme acceleration in FICO scores and FCFF.

For my full equity research report that covers FICOs whole business (including their software segment), with intrinsic value models and more, check the comment section below 👇

My 2026 Top 5 Picks have defense & offense:

$CSCO “Keep Riding the AI wave”– corporate upgrade cycle

$BA “I love big backlogs I cannot lie” & ramping cash flow

$NKE “Just Do It”-Turnaround w/ depressed multiple & EPS

$AAPL “Better Late than Never”- AI enabled foldable iPhone

$PI “The time has come”- RFID tech at an inflection point

I will put out a more detailed write-up on each name this Sunday as well as the overall positive and negatives I see for the market as a whole. I wanted to keep this post shorter given my @CNBC interview on New Year’s Eve with @davidfaber and @saraeisen got into each name in a bit more detail.

These picks are for investors that cannot short stocks to manage risk, do not have access to the same hedging tools available to me or do not have time to manage a portfolio full-time as I do. These are my best ideas right now for an investor that wants to buy a basket of stocks and not trade it for the rest of the year. The goal is to not update this list unless I think I have really gotten the thesis drastically wrong on a name. Past performance is not indicative of future results.

To be clear, for my own investments, position sizes of all names including my Top 5 Picks below are constantly being adjusted depending on my view of the future risk adjusted returns. I also have many more positions than just my 2026 Top 5 Picks.

While these are my best five ideas for 2026 based on the information I have today, my thoughts are constantly evolving based on new information & the reaction of the stock market to that data. In addition, a good hit ratio is 60% so I would expect three of the names to outperform while two are likely to under-perform. Hopefully in aggregate the results will not only be better but less volatile than the overall market. This was certainly helpful in March/April of 2025. Sleeping well at night is worth something.

As always, the key will be to remain intellectually flexible and data dependent. As Charles Darwin said, "It is not the strongest of the species that survives, nor the most intelligent, but the one most adaptable to change."

Happy New Year and I wish you all a prosperous 2026.

Bank of America says, these 6 stocks will lead the $1 trillion chip surge in 2026:

1. Nvidia (NVDA)

2. Broadcom (AVGO)

3. Lam Research (LRCX)

4. KLA (KLAC)

5. Analog Devices (ADI)

6. Cadence Design Systems (CDNS)