Post 3/4: Final Educational Take

Skip or cautious apply at best.

Long-term: Auto EV/electronics tailwinds positive, customer risks & premium pricing cap upside. Better wait for post-listing clarity or dip.

DYOR – not advice. Consult pro. #SEDEMAC#ShareMarket#IPOAnalysis

Out of 5 IPOs closing today, prima facie decision:

1. Accord Transformer IPO: Applying for Listing gains

2. Mobilise App Lab: Listing gains

3. Kiassa Retail: Avoiding

4. Clean Energy: Long term only

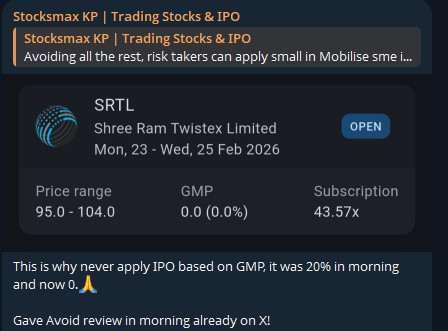

5. Shri Ram Twistex: Avoiding

Final update on https://t.co/qIvX1V18Y9

#ipo

Post 3/3: Final Take

Apply for listing gains and long term with diligence if bullish on IVF/infertility tailwinds. Long-term: Centre expansion + fresh funds positive, but attrition & competition (Nova, Indira) cap conviction.

DYOR not advice. #GaudiumIVF#ShareMarket#IPOAnalysis

Post 2/3:

Valuation: P/E ~25x FY25 PAT – reasonable for high-growth healthcare specialty vs broader peers (30-50x). Excellent ROE/ROCE.

Red flags: High attrition (31-63%), OFS (promoter exit), doctor retention risk. #IPO#HealthcareIPO

2/3 Yashhtej SME IPO

Valuation: P/E ~14-15x FY25 (attractive vs larger peers), but thin historical margins early on. High growth justifies for some.

Red flags: Soybean volatility, competition (Adani Wilmar etc.), working cap intensive. Score ~7/10. #IPO#YashhtejIPO#SMEIPO

Msafe Equipments IPO analysis. 1/3

Business: Height-safety gear (scaffolding/ladders) for infra, aviation etc.

Scale: 17 warehouses & 3 units in Greater Noida.

Edge: Dual-revenue model (Sales + Rental). Rentals bring in ~50% of revenue makes cash flow stickier.

#MSafeIPO#SMEIPO

3/3

✅ Apply: If you want a profitable infra proxy with decentlisting gain potential⚠️ Risk: Working capital is slightly heavy.

Verdict: A "safety-first" bet. Good for a listing pop, but also a decent long-term story in the infra boom. 💸

#IPOReview#Msafeipo

📈 Growth: PAT doubled to ₹13 Cr in FY25 (Revenue up 48% YoY). Valuation: Post-IPO P/E ~19x. For a company with a 34% ROCE, it’s priced quite reasonably compared to peers.

#msafeipo#Financials#IPOAnalysis

Shadowfax Final Take:

Listing Gains: CAUTION, for risk takers small apply. Long-Term: APPLY.

Best proxy for India’s Quick Commerce boom. Rule: It’s a marathon, not a sprint. Only apply if you can hold for 2+ years. Don't chase a 1-day pop here. #ShadowfaxIPO

Shadowfax IPO Analysis:

32% Revenue CAGR (FY25: ₹2,485 Cr). Profit Pivot: ₹21 Cr PAT in H1 FY26. Asset-Light: 60% Gross Margin via crowdsourced fleet.

Valuation: High and in line with peers like Delhivery.

Risk: 75% Rev from just 5 major clients.

#ShadowfaxIPO#IPOAlert