@wilson_trades@LambDownUnder And that’s where you get burned. You now have to declare that as income and pay tax at your marginal rate due to GDX turning over so much stock this FY. Had the distribution been smaller, you’d pay less tax as most of your investment is still in GDX

Why should labour income and capital gains be taxed the same? They shouldn't.

The Government has justified the increase in capital gains tax by stating that it “better aligns the tax treatment of labour income and asset income.” It is a seductive line, because it sounds like fairness. Surely all income should be treated the same, however it is earned? But that justification smuggles in an assumption the Government never defends: that a dollar of capital gain and a dollar of wages are the same thing, and that any difference in how they are taxed must be a loophole to be closed. They are not the same thing, and it is not a loophole. A dollar of wages and a dollar of capital gain are not the same dollar – they are earned differently, they carry different risks, and they reach the taxpayer by entirely different roads. The gap between them is not an oversight that crept into the system. It is a deliberate distinction that every serious tax system in the developed world recognises and builds around, for good reason. To tax the two identically is not the removal of an unfairness. It is the creation of one.

Consider what actually separates the two.

Investments are made using money that has already been taxed. A worker earns a wage and pays income tax on it. It is only after-tax dollars they have to invest with. When the return on that investment is then taxed again, the same pool of money has been taxed twice: once as it was earned, and again as it grew. Labour income is taxed once. Capital income is taxed on top of income that was already taxed. To “align” the rates is to ignore that the capital was only ever there because tax had already been paid on it.

The investor takes a risk the worker does not. A wage is contracted and reliable; you turn up, you are paid, and you do not hand back last month’s salary if the company has a bad quarter. An investment carries no such promise. The investor can lose part of their money, or all of it.

There is no guaranteed rate of return, let alone a positive one. A worker knows their wage in advance. An investor is guaranteed nothing. The return may be large, small, zero, or negative. The investment is a bet on an uncertain future, made with no assurance it will pay off at all. To tax the occasional win as though it were as safe and certain as a fortnightly pay packet is to tax a gamble as if it were a salary.

A capital gain accrues over many years but is taxed in a single one. A wage is smooth – earned and taxed in the year it is received. A capital gain is lumpy. It can build silently over a decade and then be realised all at once, in the single year the asset is sold. Taxing that entire decade’s accrual as though it were one year’s income pushes the gain into the highest brackets and assesses it at a rate it never would have attracted had it been earned evenly along the way.

Investing requires the patient deferral of consumption. Every dollar invested is a dollar deliberately not spent. The investor forgoes the holiday, the car, the comfort they could have enjoyed today, and instead sets the money aside in the hope it might be worth more tomorrow. Taxing the reward for that patience at the same rate as ordinary income is, in plain terms, a tax on saving.

And here is the point the “alignment” case never mentions at all. Labour income arrives gift-wrapped in the most extensive system of protection in the country. A worker is guaranteed a minimum wage, paid annual leave and sick leave, public holidays, superannuation contributions, redundancy entitlements, protection from unfair dismissal, and the cover of workers’ compensation if they are injured on the job. An entire body of law exists to put a floor under labour income and to shift much of its risk onto employers and the state. Capital income comes with none of this. There is no minimum return, no paid leave, no compensation when a venture fails, no tribunal that will order an investor’s lost money restored. If the company collapses, the capital is simply gone. To tax these two streams “the same” is to ask the investor – who bears the entire downside alone, with nothing and no one to catch them – to pay at the identical rate to the worker, whose downside is broadly carried by the law and the public purse. That is not equal treatment of equals. It is equal tax on profoundly unequal risk.

The conclusion follows plainly. The gap between the taxation of labour and capital is not a loophole that crept into the system by accident. It is a deliberate and well-founded feature, reflecting the double taxation, the risk, the uncertainty, the lumpiness and the deferred consumption that distinguish a capital gain from a wage.

Under Labor's new capital gains tax, if you're on the top tax rate, have a 6% mortgage and 2.5% inflation, you need to earn 9.1% investing - no small feat - just to break even with putting your money in a mortgage offset account. That's before you are compensated one cent for the risk you took, the double taxation, the time and effort.

Say you want to make at least 3% after tax above putting money in your offset account. A modest benefit. You would need to make 14.76% in the market. Do that consistently and you would be ranked amongst the greatest investors of all time. That's right - Labor's hurdle for investing as an Australian is you need to be amongst the greatest investors of all time. So if you're John Templeton or Walter Schloss, no worries.

@chrisbrycki@1stlevelthinker You didn’t specify how much better of an ETF investor would be in this case Chris - feels like you missed a trick. Wrap the 4 stocks in an ETF and the tax paid on a real economic gain of $47k

Is $22,090. A lot less than the $32,900 if held separately…

One of the biggest tax changes in decades will be announced in next week’s Federal Budget. The widely expected CGT changes won’t just affect wealthy investors or property owners... they affect anyone trying to build long term wealth through shares, investment property or building a business.

To help Australians understand the potential impact, we’ve built a CGT calculator that estimates how much better or worse off people could be under the proposed rules: https://t.co/WFVQzYuMnt

A few examples from the calculator:

• An ETF investor growing $100k over 10 years could end up with around $26k less after tax

• A property investor could lose more than $50k in after tax wealth

• A founder building and selling a business for $1m could lose more than $225k

If you materially reduce the after-tax reward for taking long term risks, fewer people will invest in businesses and productive assets. Over time that means less investment and innovation, fewer startups, lower productivity growth and ultimately fewer jobs in Australia. I discussed this in The Australian last week. https://t.co/2XmT26CTsd

Instead, more money gets pushed into the family home, super or cash sitting in the bank.

That’s why entrepreneurs and business leaders including @PaulBassat, @GeoffWilsonWAM, @leighjasper, @matt_barrie, @lux_schwab, @lukeanear, @Bron_LeGrice, @MJBiercuk and @craigRblair have all raised concerns about the broader economic consequences these changes could create.

We thought if people could properly quantify what these changes might cost them over time, it would make the broader economic impact much harder to ignore.

The calculator is designed to help Australians model different scenarios before any final rules are announced: https://t.co/WFVQzYuMnt

Theft from aspirational Australians will be delivered in the budget next week. Young Aussie puts in $10k, compounds at 15% for 50 years → $10.84 million.

Inflation-indexed cost base: just $44k. Current CGT: $2.63M tax.

Labor’s new proposal: $5.23M tax.

They want to seize HALF your life’s work.

This isn’t tax reform — it’s theft from aspirational Australia.

Stop punishing success. #TaxRaid #AussieDreamKiller

@galumay@misskylie77@AusSuper You mean like this? https://t.co/4PM8YEu3i4

Credit is currently sitting at 3% of their exposure so hardly anything to worry about?

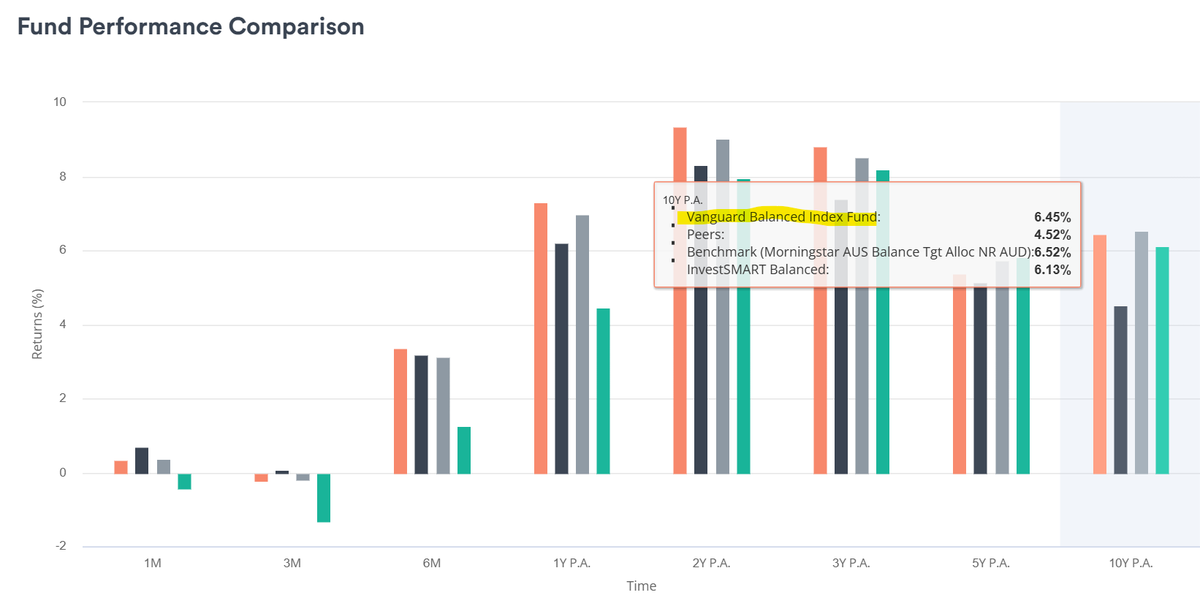

@galumay@misskylie77@AusSuper Think you’ll find this has already happened… The M* growth target runs at 70% growth assets. AusSuper balanced closer to 80% growth assets, so clearly taken some markdowns in the last few years (well publicised) https://t.co/3fms41abe1

So I expect an Aussie large cap strategy with a very strong record to pick up a lot of the low hanging fruit in this space.

TL;DR Market is sleeping on the immense opportunity that Plato have ahead of themselves and will become the next “Magellan” of the funds managementindustry

Significant new position in $PNI.AX on the basis that the Plato Global Alpha Fund ($PGA1.AX) becomes the next Magellan Global Fund in the industry. And their soon to be released Aussie equivalent goes on to do the same in Aus equities. 1/n

Any previous mention of. There is a gaping opportunity in Aussie large caps for allocators, with perennial favourites (Bennelong, Hyperion, Fidelity, DNR etc) all having a very tough time of it at the moment. Allocators have been heavily favouring passive in this asset class 6/n