🚀 IPO Update from Sushil Finance - CSM TECHNOLOGIES LIMITED

💻 Business Overview

CSM Technologies Limited, incorporated in 1998, is a Bhubaneswar-based IT solutions company specializing in GovTech solutions and digital transformation services.

With over 27 years of experience, the company designs, develops, and implements customized e-governance platforms and digital infrastructure solutions for both government and private sector clients.

🏛️ Key Sectors Served

The company operates across 10 business verticals and provides technology solutions for:

• Mining

• Agriculture

• Healthcare

• Education

• Tourism

• Other public service sectors

🌐 Strong Geographic Presence

While headquartered in Odisha, CSM Technologies has expanded its operations to:

• 20 cities across India

• Presence in 14 countries including:

▪️ Kenya

▪️ Ethiopia

▪️ USA

▪️ Canada

⚙️ Business Model

The company follows a project-driven model focused on:

• Large-scale technology implementations

• Digital governance solutions

• Public service delivery enhancement

• Data-driven decision-making platforms

Its expertise in executing mission-critical digital infrastructure projects has enabled it to build long-standing relationships with government departments and institutional clients.

🌟 HIGHLIGHTS

1️⃣ Deep sectoral expertise across a diversified range of industries

2️⃣ Proprietary technology innovations and patented solutions developed in-house

3️⃣ Extensive geographic footprint with scalable operations across India and international markets

4️⃣ Established presence in a high-entry-barrier GovTech industry

5️⃣ Experienced promoters and senior management team with strong domain expertise

🚢 Did you know that Waterways Leisure Tourism(Cordelia Cruises) is India's only scaled domestic ocean cruise operator?

Is this a voyage worth joining?

📖 Read our detailed IPO analysis: https://t.co/qSeM39myor

📌 Research Disclaimer: https://t.co/FJ0rDsbyqx

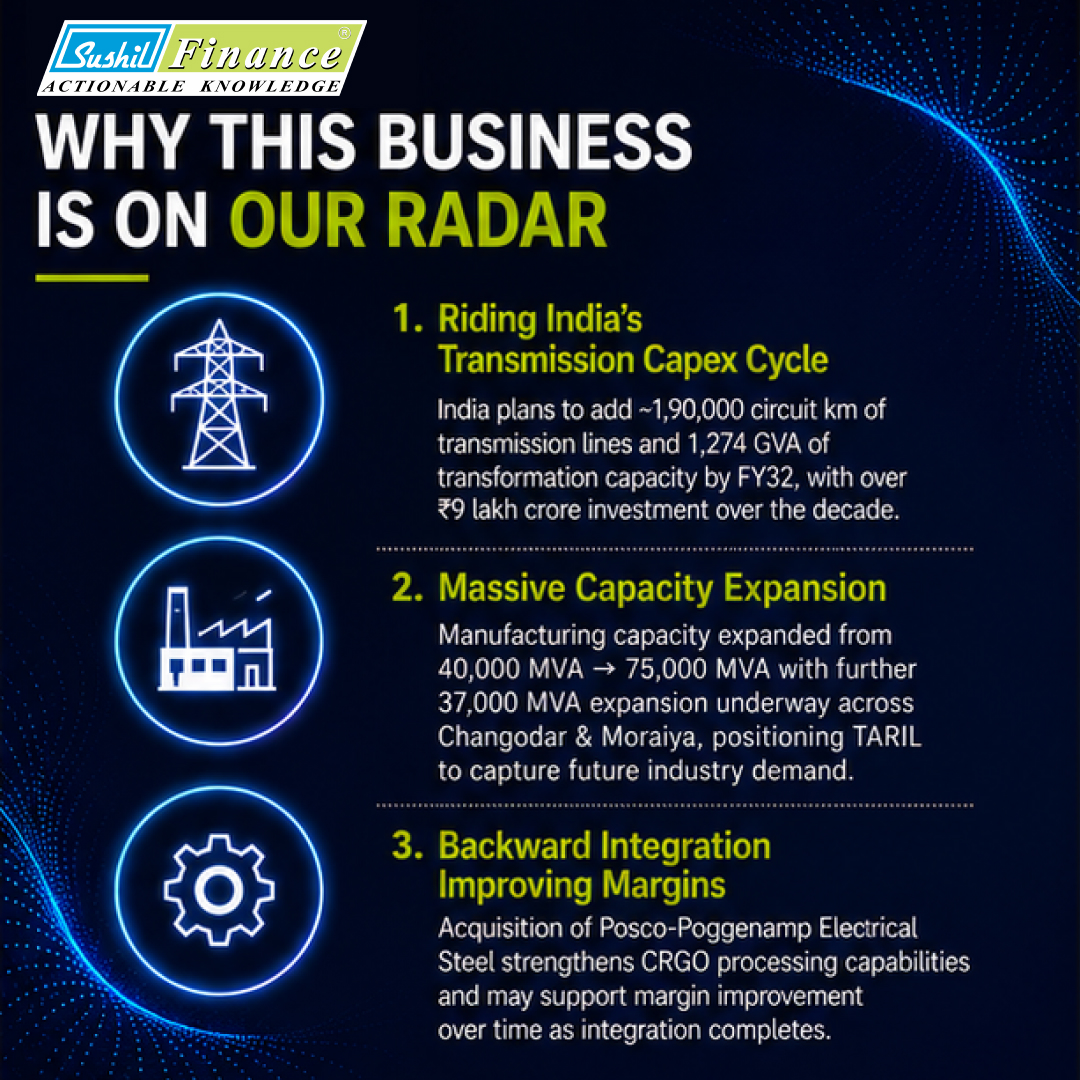

📢 New Report Alert – Transformers and Rectifiers (India) Ltd

Transformers and Rectifiers (India) Limited, or TARIL, is an Indian power equipment manufacturer focused on transformers and reactors used by utilities, industrial customers, and export clients Founded in 1981 and headquartered in Ahmedabad, the company has built a meaningful presence in India’s transformer market over the years Its capabilities today span a wide range of products, including power, furnace, rectifier, distribution, and specialty transformers along with reactors used across grid and industrial applications.

We expect TARIL to deliver 67% growth in Revenues to Rs. 4226.5 crore in FY29E from Rs. 2508.8 crore in FY26. This growth is majorly driven by the structural tailwinds of the Indian power industry and its supply gap. Furthermore, the company’s move towards backward integration through acquisition and capex increases EBITDA margins. The stable order book shows the way for growth and consistent revenue for the company. We estimate the EBITDA and PAT margins to be 16.4% and 10% respectively by FY29E. Our estimated EPS is Rs. 10.2, Rs. 11.2 and Rs 14.1 for FY27E, FY28E and FY29E respectively. We assign a P/E multiple of 35x to arrive at the target price of Rs. 492, which is an upside of ~37% from its last closing price at Rs. 358. We initiate coverage on TARIL with a BUY rating, over an investment horizon of 24-30 months.

📩 Comment "TARIL" to get the full report

🔗 For the Disclaimer, check our Link-in-Bio

.

.

.

.

.

.

.

.

.

.

.

.

.

#stockreccomendation #topstocks #stockmarkettip

🚀 IPO Update from Sushil Finance - WATERWAYS LEISURE TOURISM LIMITED (Cordelia Cruises)

🚢 Business Overview

Waterways Leisure Tourism Limited operates Cordelia Cruises, India's only scaled domestic ocean cruise operator.

⚓ The company operates the MV Empress, a 796-cabin cruise ship serving popular routes such as:

• Mumbai – Goa – Mumbai

• Mumbai – Lakshadweep

• Chennai – Sri Lanka

📊 Since inception:

• 7,30,819+ guests served

• 3,21,292 nautical miles covered

🎭 Unique India-Focused Cruise Experience

Cordelia offers a distinctly Indian cruise experience featuring:

• Bollywood-themed live entertainment

• Balle Balle

• Razzmatazz

• Indian Cinemagic

• Burlesque The Bollywood Way

🎤 Supported by 85+ onboard performers.

🍽 Onboard Facilities Include

• Indian & Jain Cuisine

• Casino

• Spa & Wellness Centre

• Rock Climbing Wall

• Children's Academy

• MICE & Corporate Event Facilities

🎉 The company also hosts chartered events and entertainment cruises, including the popular Sunburn x Cordelia Cruise Festival.

🚀 Growth Strategy

IPO proceeds will be utilized towards charter payments for two additional cruise vessels:

🛳 Norwegian Sky

• Capacity: 2,004 Guests

• Expected Delivery: August 2026

🛳 Norwegian Sun

• Capacity: 1,936 Guests

• Expected Delivery: November 2027

Following deployment of these vessels, total passenger capacity is expected to increase from 796 berths to approximately 4,736 berths across three cruise ships.

🌟 HIGHLIGHTS

1️⃣ Pioneer and dominant player in India's ocean cruise industry

2️⃣ Authentic India-focused cruise experience with extensive onboard amenities

3️⃣ Strong direct booking mix with over 62% bookings coming directly from customers

4️⃣ Asset-light business model with outsourced operations

5️⃣ Experienced management team with deep industry and regulatory expertise

🚀 IPO Update from Sushil Finance - ADVIT JEWELS LIMITED

💎 Business Overview

Advit Jewels Limited, operating under the heritage brand "Rambhajo Since 1921", is a Jaipur-based manufacturer and retailer of handcrafted fine jewellery specializing in:

✨ Kundan Jewellery

✨ Polki Jewellery

✨ Diamond Jewellery

✨ Studded Jewellery

With a legacy spanning over 100 years, the company combines traditional craftsmanship with modern manufacturing technologies.

🏭 Integrated Manufacturing Facility

The company operates a 6,450 sq. ft. facility in Jaipur where the entire production process is managed in-house.

🔧 Manufacturing capabilities include:

• CAD Design

• 3D Printing

• Laser Cutting

• CVD Testing

👨🎨 Supported by 185 skilled artisans, the company offers a portfolio of 2,000+ unique jewellery designs.

💍 Product Range Includes:

• Necklace Sets

• Bangles & Bracelets

• Earrings

• Pendants

• Rings

• Bridal Jewellery

🌍 Market Presence

The company primarily follows a B2B business model, supplying jewellery retailers across 18 states in India while simultaneously expanding its direct-to-consumer presence.

🌐 Recently, Advit Jewels commenced exports to:

• United States

• Hong Kong

📈 Financial Performance

• Revenue increased from ₹ 46.60 Cr. in FY23 to ₹ 124.94 Cr. in FY25

• EBITDA Margins remained strong at approximately 29–30%

The IPO is a 100% Fresh Issue and follows a successful pre-IPO placement that raised ₹ 22.90 Cr.

🌟 HIGHLIGHTS

1️⃣ Organized manufacturing operations under one roof

2️⃣ Strong design capabilities with diversified product offerings across customer segments

3️⃣ Robust operational systems and risk management framework

4️⃣ Experienced leadership team with proven execution capabilities

5️⃣ Strong commitment to quality and craftsmanship

🚀 IPO Update from Sushil Finance - TURTLEMINT FINTECH SOLUTIONS LIMITED

🏢 Business Overview

Turtlemint is a technology-driven insurance distribution platform founded in 2015. The company connects customers, insurance advisors (Digital Partners), and insurers through a scalable digital ecosystem.

🌐 As of December 2025, Turtlemint operates India's largest certified PoSP (Point-of-Sale Person) network among its peers.

📊 Platform Scale

* 6,31,885 Digital Partners

* 5,07,124 PoSPs

* 45 Insurance Partners

* Presence across 19,171 pin codes

* Coverage of ~98% of India

🛡️ The platform primarily distributes:

* Health Insurance

* Life Insurance

* Motor Insurance

It also offers:

* Mutual Funds

* Loans

* Credit Cards

* Deposit Products

📈 Growth Highlights

* Platform Premium grew at a CAGR of 33.3% from ₹ 6,989 Cr. (FY20) to ₹ 29,459 Cr. (FY25)

* Platform Premium of ₹ 26,316 Cr. in 9M FY26

* Facilitated 21.87 million insurance policies between April 2022 and December 2025

* Generated cumulative Platform Premium exceeding ₹ 1 lakh crore

🏆 Strong Presence in Bharat Markets

Approximately 75.1% of Platform Premium in 9M FY26 came from B30+ markets, significantly higher than the industry average of 50–60%.

📈 Financial Snapshot (FY25)

* Revenue from Operations: ₹ 7,003 Cr.

* YoY Revenue Growth: 24.1%

⚠️ However, the company remains loss-making:

* Proforma Loss: ₹ 2,026 Cr.

* Adjusted EBITDA: -₹ 1,863 Cr.

✅ Service EBITDA Margin improved to 11.9% in FY25, indicating improving operational efficiency and unit economics.

🌟 HIGHLIGHTS

1️⃣ Strong positioning in the PoSP ecosystem with scalable pan-India distribution

2️⃣ Diversified and granular Digital Partner network supported by technology-driven training

3️⃣ Long-term partnerships with multiple insurance companies

4️⃣ Improving unit economics driven by strong earnings growth, partner retention, and operating leverage

5️⃣ Strong network effects, experienced promoters, and backing from marquee investors

📢 Initiating Coverage – Granules India Ltd.

Granules is currently positioned at a highly lucrative inflection point, undergoing a structural transformation from high volume, low margin manufacturer to a high-margin complex finished dosages, controlled substances and peptide Contract Development and Manufacturing Organization (CDMO). Going forward, we expect the company to deliver an EPS of Rs.35.7 in FY28; assigning a target multiple of 27x, we arrive at a target price of Rs.963 showcasing an upside potential of 27% from current levels with an investment horizon of 18-24 months.

📩 Comment "GRANULES" to get the full report

🔗 For the Disclaimer, check our Link-in-Bio

.

.

.

.

.

.

.

.

.

.

.

.

.

#stockreccomendation #topstocks #stockmarkettip

🚀 All You Need to Know About the HEXAGON NUTRITION LIMITED IPO

🥗 Business Overview

Hexagon Nutrition Limited is a Mumbai-based, research-driven nutrition company founded in 1993 . The company has evolved into a fully integrated nutrition enterprise with capabilities spanning research, product development, manufacturing, and marketing .

The business operates across three key segments :

🔹 Branded Nutrition Products (B2C)

Includes popular brands such as:

* Pentasure

* Obesigo

* Pediagold

* Nutrone

🔹 Premix Formulations (B2B2C)

Supplies customized micronutrient premixes to leading Indian and multinational FMCG companies.

🔹 ESG-Focused Nutrition Solutions

Includes:

* Ready-to-Use Foods (RUFs)

* Micronutrient Powders (MNPs)

These products are supplied through UN agencies and government health ministries globally .

🏭 Manufacturing Footprint

The company operates 4 manufacturing facilities :

* Nashik (India)

* Chennai (India)

* Thoothukudi (India)

* Tashkent (Uzbekistan)

All facilities are accredited with certifications such as:

✔️ FSSC 22000

✔️ GMP

✔️ ISO 9001:2015

✔️ Halal

🌍 Global Presence

* Products exported to 75+ countries

* Supported by 20 regional distributors across:

▪️ Americas

▪️ Southeast Asia

▪️ Africa

▪️ Middle East

🇮🇳 Domestic Reach

* 350+ non-exclusive distributors

* 160+ sales professionals

* Engagement with ~20,000 healthcare professionals

📊 Financial Snapshot (9M FY26)

* Revenue from Operations: ~₹ 267.6 Cr.

Revenue Mix:

* Premix Formulations – ~51%

* Branded Nutrition Products – ~30%

* ESG Nutrition Segment – ~18%

🌟 HIGHLIGHTS

1️⃣ One of India's largest micronutrient premix players and a leading licensed MNP supplier under UN programmes

2️⃣ Diversified business model across B2C nutrition, B2B2C premixes, and ESG-focused therapeutic nutrition

3️⃣ Revenue grew from ₹ 278.5 Cr. (FY23) to ₹ 324.9 Cr. (FY25); EBITDA margin improved from 6.2% to 12.3%

4️⃣ Products exported to 75+ countries through a global distribution network

5️⃣ Promoter-led company with 30–40+ years of industry experience and an active R&D pipeline of 9 products

🚨 This IPO is riding India's sustainability and recycling boom... but it's also raising a major question for investors.

CMR Green Technologies is one of India's largest non-ferrous metal recyclers, serving leading automotive brands and benefiting from strong industry tailwinds.

But here's the catch: the company won't receive a single rupee from the IPO.

What does that mean for investors?

📖 Read our complete IPO analysis:

👉 https://t.co/O8iVmq9WyF

Our View: Cautious ⚖️

📌 Research Disclaimer : https://t.co/6OPLEyXPwZ

🚀 All You Need to Know About the CMR GREEN TECHNOLOGIES LIMITED IPO

♻️ Business Overview

CMR Green Technologies Limited is India's leading non-ferrous metal recycler in terms of installed capacity and holds the highest market share in the Indian secondary aluminium market by revenue among its peer group (FY2025).

🏭 The company operates 13 recycling facilities across India with a combined production capacity of 615,150 MTPA.

🔩 Its product portfolio includes:

* Recycled Aluminium Alloys (Ingot & Liquid)

* Zinc Alloy Ingots

* Dross Products

* Furnace-Ready Scrap of Stainless Steel, Copper, Brass, Zinc, Lead & Magnesium

🚗 The company primarily serves leading automotive OEMs and Tier-1 suppliers including:

* Maruti Suzuki

* Honda

* Bajaj Auto

* Hero MotoCorp

* Royal Enfield

📊 Financial Highlights

* FY2025 Revenue: ₹ 6,665 Cr.

* 9M FY26 Revenue: ₹ 6,276 Cr.

* FY2025 EBITDA: ₹ 304 Cr.

* FY2025 PAT: ₹ 155 Cr.

* Net Debt/Equity: 0.58x

📈 The company has delivered a strong Revenue CAGR of ~23% from FY2007 to FY2025.

🚘 Aluminium and Zinc Alloys contribute approximately 81% of revenue, while the automotive sector accounts for around 83% of total revenue.

🌍 With a large-scale recycling platform, strong sourcing capabilities, and established customer relationships, CMR is well-positioned to benefit from the growing demand for sustainable and circular manufacturing solutions.

🌟 HIGHLIGHTS

1️⃣ Unrivalled market leadership with high entry barriers

2️⃣ Exclusive liquid aluminium supplier with patented technology

3️⃣ Global and diversified raw material sourcing network

4️⃣ Long-term relationships with leading OEMs and Tier-1 customers

5️⃣ Strategic Japanese JV partnerships for technology and scale

📢 Re-Initiating Coverage – Ethos Ltd.

Ethos crossed the 100-boutique milestone post-year-end, with the 100th boutique opening in Indore on May 15,

2026, against 73 at end-FY2025.

We expect Ethos Limited to deliver revenue growth of approximately 138% by FY2029E over FY2025, driven by robust domestic luxury demand, aggressive store network expansion, and margin improvement supported by the India-Switzerland EFTA agreement now in force since October 2025. We estimate EBITDA and PAT margins to improve to approximately 14.2% and 7.4%, respectively, by FY2028E, reflecting operating leverage from store maturation and a favourable revenue mix shift toward exclusive brand partnerships. Our EPS estimates stand at Rs.53.5, Rs.67.8, and Rs.81.9 for FY2027E, FY2028E, and FY2029E, respectively.

Assigning a P/E multiple of 40x on FY2029E EPS, we arrive at a target price of Rs.3,274, implying an upside of ~35% from the current market price of Rs.2,459. We re-instate coverage on Ethos Limited with a BUY rating, with an investment horizon of 24– 30 months.

📩 Comment "ETHOS" to get the full report

🔗 For the Disclaimer, check our Link-in-Bio

.

.

.

.

.

.

.

.

.

.

.

.

.

#stockreccomendation #topstocks #stockmarkettip

📢 Initiating Coverage – Affle 3I Ltd .

Advertisers Only Pay When It Works: A Rare and Powerful Business Model: Affle’s core business model, Cost

Per Converted User (CPCU), charges advertisers only when a measurable conversion occurs, such as an app

install, purchase, signup, or transaction, making ad spends outcome-driven and highly measurable.

Going forward, we expect the company to deliver an EPS of ~Rs.52 in FY28E; assigning a target multiple of 39x, we arrive at a target price of ~Rs.2,033, showcasing an upside potential of 38% from current levels. Hence we initiate coverage on Affle 3i Ltd. with a BUY rating, over an investment horizon of 18 – 24 months.

📩 Comment "AFFLE" to get the full report

🔗 For the Disclaimer, check our Link-in-Bio

.

.

.

.

.

.

.

.

.

.

.

.

.

#stockreccomendation #topstocks #stockmarkettip

📢 Initiating Coverage – MASTEK LTD.

Mastek's Oracle practice spans 2,000+ certified consultants and 1,300+ implementations across 40 countries,

with independent recognition from Gartner, Everest Group, ISG, and Forrester, a combination few mid-sized

Indian IT peers can match.

We expect Mastek Ltd. to deliver 27% growth in Revenues to Rs.4691.8 crore in FY29E from Rs.3698.8 crore in FY26. This growth is majorly driven by the AI led growth with their revenue model transition, its specialization in Oracle Cloud and Salesforce certifications. Furthermore, the company’s presence and relationship with the UK Public Sector has high entry barriers. We estimate the EBITDA and PAT margins to be 16.4% and 11.6% respectively by FY29E. Our estimated EPS is Rs.144.2, Rs. 158.2 and Rs 176.1 for FY27E, FY28E and FY29E respectively. We assign a P/E multiple of 13x to arrive at the target price of Rs. 2290, which is an upside of ~37% from its last closing price at Rs. 1674. We initiate coverage on Mastek Ltd. with a BUY rating, over an investment horizon of 24-30 months.

📩 Comment "MASTEK" to get the full report

🔗 For the Disclaimer, check our Link-in-Bio

.

.

.

.

.

.

.

.

.

.

.

.

.

#stockreccomendation #topstocks #stockmarkettip

📢 Q4 FY26 Results Update – Kajaria Ceramics Ltd.

Kajaria Ceramics Ltd. recently announced its performance for the quarter ended March 31, 2026. Following are the key highlights.

With the cost optimization measures by the company and improvement in consumer demand, we expect the bottomline to grow faster clip, at 22% CAGR in FY25-28, with FY28E EPS to be Rs. 39.8. We arrive at a Target Price of Rs. 1,650, showcasing an upside potential of 55% from current levels with an investment horizon of 18-24 months, with a BUY rating on the stock.

📩 Comment "KAJARIA" to get the full report

🔗 For the Disclaimer, check our Link-in-Bio

.

.

.

.

.

.

.

.

.

.

.

.

.

#stockreccomendation #topstocks #stockmarkettip

📈 India’s tech sector gets a new trading opportunity on the exchange floor.

Introducing BSE Focused IT Index Options - designed to offer exposure to India’s leading technology companies through a single index-based derivative product. 💻⚡

🗓 Launching from 11th May 2026

📅 Monthly Expiry: Last Thursday of every month

#BSE #StockMarket #Derivatives #IndexOptions #ITSector #TechStocks #Trading #IndianMarkets #MarketUpdate #OptionsTrading

This IPO isn’t a typical stock… 👀

✔️ Premium office parks in Bengaluru

✔️ Tenants like Google, Amazon, Nvidia

✔️ 98.8% occupancy

Sounds solid, right?

But here’s what investors must understand before applying.

We’ve broken it all down.

👉 Read full Bagmane Prime Office REIT IPO analysis before you invest:

🔗 https://t.co/77qPYhUy5f

📌 Research Disclaimer : https://t.co/6OPLEyXPwZ

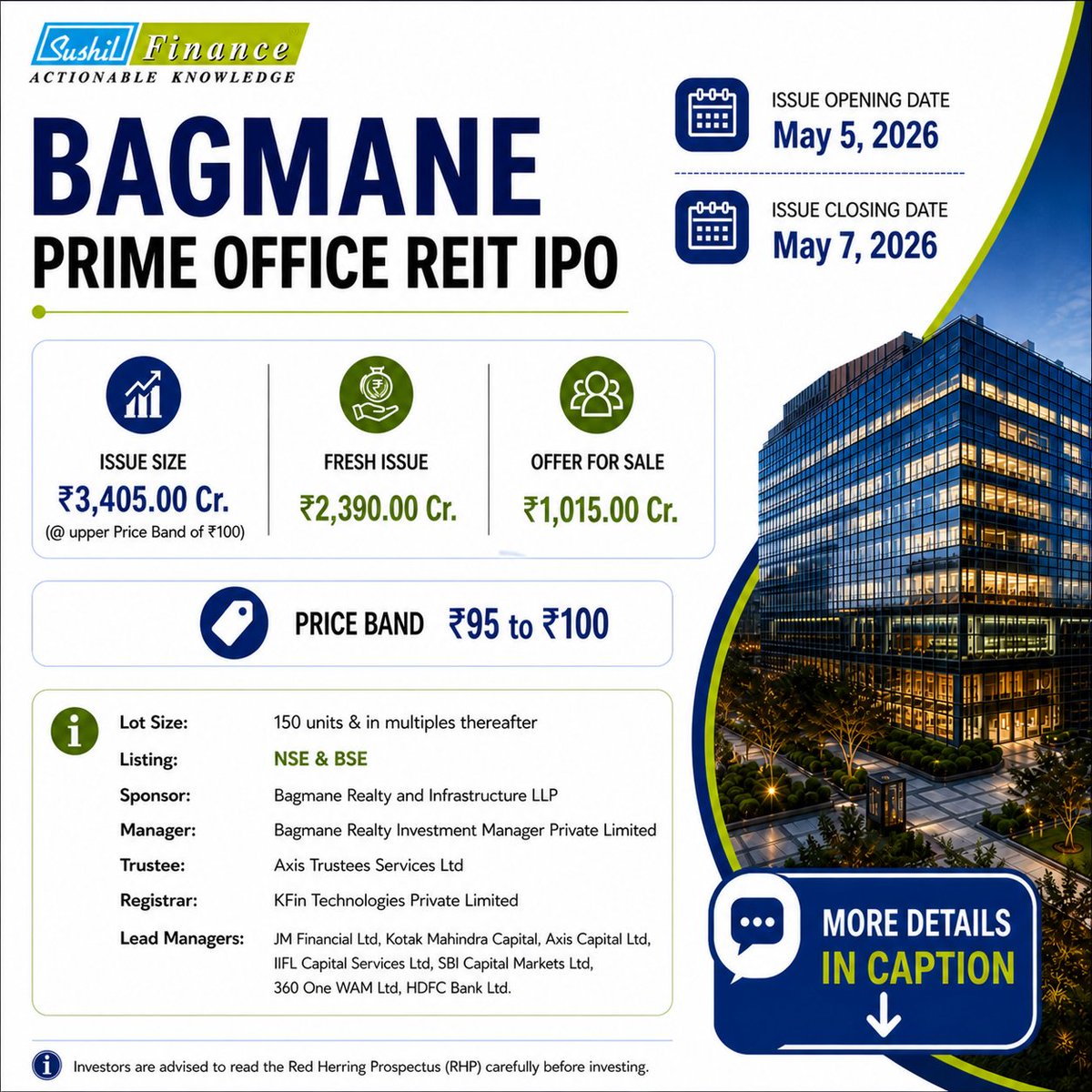

All You Need to Know About the Bagmane Prime Office REIT

🏢 Business Overview

Bagmane Prime Office REIT is a real estate investment trust focused on owning and managing premium Grade A+ office parks in Bengaluru.

Backed by the Bagmane Group (with ~30 years of experience), the REIT has built a strong portfolio of high-quality commercial assets.

📊 Portfolio Strength

* Total Leasable Area: ~19.6 million sq. ft.

* 6 premium business parks across Bengaluru

* Located in top micro-markets:

– Outer Ring Road (ORR)

– Secondary Business District (SBD City)

📈 Occupancy: 98.8% (very strong)

🗓️ WALE: 7.4 years (long-term lease visibility)

🌍 Tenant Profile

The REIT has a high-quality tenant base, including:

🌐 Google

🌐 Amazon

🌐 Nvidia

🌐 Volvo

* ~98.7% rentals from foreign-headquartered MNCs & GCCs

👉 Indicates strong stability and premium positioning

⚡ Additional Assets & Value Drivers

* Solar power capacity: 164.4 MW ☀️

* 2 under-construction hotels (607 keys) 🏨

📈 Growth Drivers

* Built-to-Suit (BTS) developments

* Contractual rental escalations

* Mark-to-market upside (~17.6% higher than current rents)

⭐ Investment Highlights

1️⃣ Strong relationships with global MNC & GCC tenants

2️⃣ Premium, hard-to-replicate office assets

3️⃣ Strategic presence in Bengaluru’s top commercial hubs

4️⃣ Integrated infrastructure with sustainable energy assets

5️⃣ Long lease tenure ensuring stable cash flows

6️⃣ Strong growth visibility through rental upside

📢 Initiating Coverage – Greaves Cotton Limited.

We expect Greaves Cotton Limited to deliver healthy revenue growth over FY2025–FY2028E, driven by scale-up in the electric mobility segment, steady performance in the core engineering business, and execution under the https://t.co/D0Z6GQDzZI framework. The EV business is expected to contribute a higher share of incremental revenues, supported by distribution expansion and improving adoption in last-mile mobility, while the legacy business continues to provide stability and cash flows. We estimate EBITDA and PAT margins to gradually improve over the medium term, led by operating leverage in the EV segment, cost optimization, and a stable contribution from the core business. Our EPS estimates stand at Rs.5.1, Rs.5.7, and Rs.5.7 for FY2026E, FY2027E, and FY2028E, respectively. Assigning a P/E multiple of 36x on FY2028E EPS, we arrive at a target price of Rs.204, implying an upside of ~23% from the CMP of Rs.166, we initiate coverage on Greaves Cotton Limited with a BUY

rating, with an investment horizon of 24–30 months.

📩 Comment "GREAVES" to get the full report

🔗 For the Disclaimer, check our Link-in-Bio

.

.

.

.

.

.

.

.

.

.

.

.

.

#stockreccomendation #topstocks #stockmarkettip

🚨 New IPO Alert!

A fast-growing digital lending company is entering the market 💰

But… is it really worth investing in? 🤔

👉 Don’t invest before reading this expert analysis because 🧠 Smart investors research first, invest later!

🔗 Read before you invest : https://t.co/X9PYKagZaX

📌 Research Disclaimer : https://t.co/6OPLEyXPwZ

All You Need to Know About the ONEMI TECHNOLOGY SOLUTIONS LIMITED IPO

💻 Business Overview

OnEMI Technology Solutions Limited, operating under the flagship brand Kissht, is a technology-enabled digital lending platform focused on providing fast, accessible, and personalized credit solutions.

Established in 2016, the company primarily targets young, digitally active individuals from India’s emerging middle class—segments often underserved by traditional banking due to limited credit history.

💰 Product & Business Model

* Core offering: Unsecured Personal Loans

* Recently expanded into:

– Loans Against Property (LAP) (secured lending)

These cater to both:

✔️ Personal consumption

✔️ Business expansion needs

📊 Scale & Reach

* AUM: ₹ 59,557.53 million (as of Dec 31, 2025)

* Registered Users: 63.73 million

📲 Strong customer acquisition via:

* Digital marketing

* E-commerce integrations

* Unique Credit QR O2O model

* Network of 52,000+ merchant partners

🤖 Technology Edge

The company operates on a cloud-native, AI & ML-driven platform that manages:

* Customer acquisition

* Digital onboarding

* Real-time underwriting

* Automated collections

This enables high scalability and faster credit delivery.

🏦 Funding & Structure

* On-book lending via RBI-regulated subsidiary

👉 Si Creva Capital Services Pvt. Ltd.

* Off-book lending through 47 institutional partners

Ensures a diversified and scalable liability model

📈 Growth & Strategy

* AUM CAGR: 79.53% (FY23–FY25)

* Future focus:

– Expansion into insurance & savings products

– Building a full-stack financial services platform

⭐ Highlights

1️⃣ Large customer base through diversified acquisition strategy

2️⃣ Strong risk management driving asset quality

3️⃣ Access to diversified funding sources

4️⃣ Scalable AI-driven technology platform

5️⃣ Experienced founders backed by marquee investors