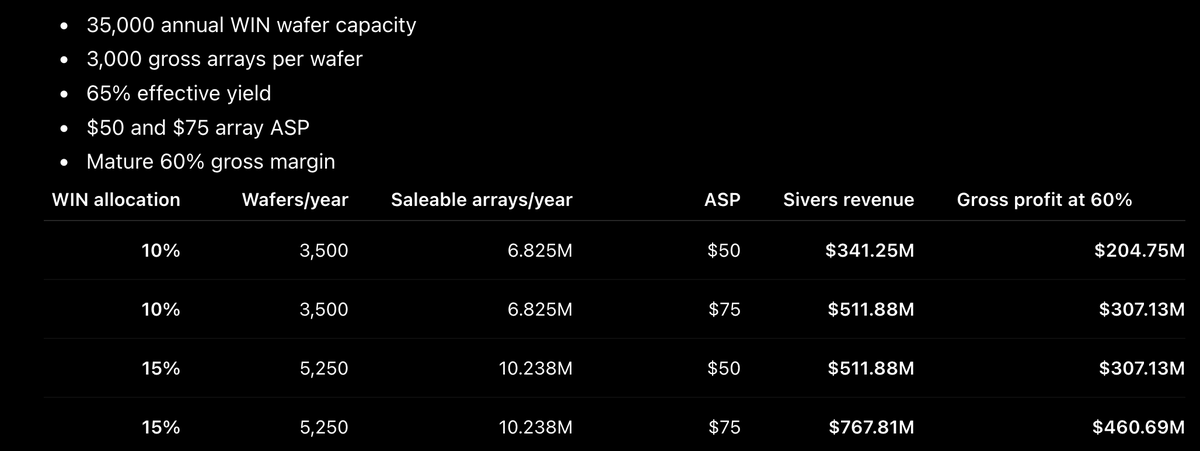

Lot of people were curious about $SIVE capacity volume ramp modeling through fab-light (Win Semi + others):

Using 10% of Win's wafer capacity as a low-end allocation (65% yield assumption, $50-$75 ASP):

Sivers would support $341-$512M worth of annual array revenue. Given upper end of managements 50-60%+ gross margin target, would be roughly:

$205–307M of annual gross profit.

Against Sivers current ~$1.1B MC, would be ~:

3.6–5.4× MC/gross profit if this capacity scenario plays out in 2028.

And at 15% would be $307–461M in gross profit (2.4–3.6× MC/gross profit)

Sivers CEO also replied that they're working with more fabs for capacity. And from an older deck, there looks to be more qualifications since 2024.

So capacity targets might be larger than what's stated here as CPO takes off.

I also expect to see revenue pipeline projections hiked in future quarters, as more qualification suppliers to into HVM.

_

As for demand side, CW also happens to be very bottlenecked.

Lumentum are buying CW off the open market due to EML obligations from their ER transcript.

And $AMD are signing LTAs to secure CW capacity (from Trendforce). So when Sivers is ramping with $GFS, $JBL, Ayar, $POET, O-NET and others...

Given the current constraints, it's highly likely any independent qualified capacity that comes online would be absorbed.

And as a cherry on top, Morgan Stanley named $SIVE (~$1.1B) as one of the three leading CPO laser players .

Alongside $55B+ players Coherent and Lumentum in their recent note for a reason...

_

TLDR: Sivers only needs a low end allocation from Win to make substantial gross income relative to current valuations.

I think the largest revenue upside that isn't modeled in if they TAM expansion with M&A after US NASDAQ listing.

By copying the Lumentum playbook with Cloud Light to build out entire transceiver modules or with optical engines.

My head gasket is gone. Destroyed. I had no injury / injuries going into the fight. I was throwing kicks, planted and jumping, all throughout camp as well as backstage before the fight. This came out of nowhere. I am beyond dark here. I can only describe it as hell.

$SIVE is the most compelling CPO/photonics exposure to me.

Addressing the disinformation: I haven’t sold and don’t plan to sell a single share.

I do think this ends up the next $80B+ $LITE one day from ~$2.1B.

And I personally have plans to acquire more ownership + support their M&A prospects.

I believe earnings transcripts will be strongly positive.

As in the part few months we’ve discovered:

> AlChip/Amazon private placements, which is positive for Ayar -> $SIVE implying Trainium 4 design in

> Wiwynn + Ayar CPO scale up

> $JBL 1.6T optical transceiver ramp with Sivers incoming faster than markets expected (with relatively dramatic moat + demand as much as they can produce)

> O-Net scaling up ELS efforts with $SIVE

> $YSS acquisition of $SIVE allspace lead partner, designing Sivers into Space defense primes

> New CHIPS ACT funding for $SIVE

> $POET H2 volume ramp and their new $50m -> $500m order (with $SIVE as light source)

> information discovery around $AAPL using $SIVE lasers for next gen consumer devices

> information discovery around links to Lightelligence (went public $10B+ MC) + Lightmatter as likely customers.

> Celestial volume ramp with $MRVL indicators.

> new customers working on TFLN with $SIVE like Lightium

> $AMD going with $GFS for CPO, and GFS listing sivers as one of two laser suppliers

> Ayar removing $MTSI / $LITE from their website and signaling $SIVE as primary source/sole source

> Ayar raising $500m for volume ramp (intel, Mediatek, Nvidia, amd etc)

> pluggable TAM expansion signaled from 2025 annual report

> Nasdaq listing expected soon

> MSCI small cap index / Nasdaq omx inclusion, making Blackrock, Vanguard and others passive buyers

> M&A signaled from 2025 annual report + 2 new board members that have experience in that area

> $NOK as likely customer from 2025 annual report.

> $LITE getting cw bottlenecked from EML contracts, $SIVE signaling capacity agreements in place with Win, making the a likely bottleneck owner + chokepoint in CPO sector.

All of this market research was done before earnings.

Any results is just confirmation of supply chain mapping done.

I don’t think anyone cares about former quarter revenue since $SIVE is an exceptionally compelling 2027 long, especially H2 onward.

Only thing I’m looking at are:

> TAM expansion of the overall photonics supercycle (eg. optical engine, ELS, pluggables) either from M&A or developments

> volume ramp expectations from existing companies

> Nasdaq listing timelines for more liquidity to support their M&A efforts

> any new customers signaled for CPO/Pluggables