@DavidNdii vanity and spurious metrics don’t change reality. Anyone with children or close family in a public uni knows the facts(real facts). Since the new funding model was introduced, it’s a mess.

THE PEOPLE HAVE SPOKEN.

You asked. You shared. You demanded it.

So we're bringing it back. The Gallery of Ruto's Lies returns for a special re-air today—the Eighth Day.

🕤 9:30 PM

Don't miss it. Only on KTN.

#ChekiKTN#FactsFirst

Gives new meaning to “light as a feather.”

Pre-order your lightweight, smart, screenless Google #FitbitAir starting at $99.99¹: https://t.co/p4rzwfiAAY

Available May 26.

¹Price varies depending on territory.

The Finance Bill, 2026 was published on 30th April and is now before Parliament and every Kenyan deserves to know what is in it.

The government targets Ksh3.63 trillion in revenue for 2026/27 and a wider budget deficit of 5.3% of GDP in the 2026/27 fiscal year (July-June) up from 4.7% in 2025/26. These are not unreasonable fiscal objectives but the manner in which the burden of achieving them is distributed is a cause for serious concern.

On tax filing timelines, the Bill moves the income tax return deadline to April 30th which is two months earlier than the current June 30th and compresses nil return filing to January 31st. This reduces the time available for audit completion, cash flow planning and compliance. For small businesses and individual traders, this is not administrative reform. It is an additional compliance cost they can ill afford.

On mitumba, the Bill inserts a new Section 12H into the Income Tax Act which deems profit at 5% of customs value payable upfront before goods are released by KRA as a final tax. A trader importing a bale worth Ksh1 million pays Ksh50,000 regardless of whether they make a profit or a loss. I cannot in good conscience describe this as equitable.

The Bill increases residential rental income tax from 7.5% to 10%. Absent a serious enforcement framework, this will drive non-compliance rather than revenue. The government must fix the enforcement gap before it increases the rate. One without the other is burden-shifting.

On digital financial services, the Bill removes existing VAT exemptions on money transfers and payment processing. These are the tools of financial inclusion that millions of Kenyans including the very people this government says it wants to reach rely on daily. Making them more expensive will not serve the objective of a broader tax base.

By including interchange and merchant service fees within the definition of management or professional fees for withholding tax purposes, the Bill introduces a compliance burden into automated banking processes. That burden will be passed on to businesses and ultimately to consumers.

The amendment to Section 24 of the Income Tax Act empowers KRA to deem at least 60% of a company's undistributed income as dividends for tax purposes. This fails to account for legitimate decisions on reinvestment, working capital and business growth. It is a retrogressive measure that sends the wrong signal to the investors Kenya needs.

A 25% excise duty on telephones for cellular and wireless networks is proposed. A phone is not a luxury. It is how Kenyans bank, communicate, conduct business and access government services. Parliament must interrogate this carefully.

On PAYE, Kenyans were led to expect relief and a restructuring of the tax bands to ease the burden on salaried workers. That proposal does not appear in this Bill. That is not a minor omission. An explanation is owed to every employed Kenyan who was waiting for it.

To be fair, the Bill is not without merit. The reduction of corporate tax for non-resident companies from 37.5% to 30% improves our investment climate. The extension of the tax amnesty to cover liabilities up to 31st December 2025 provides a genuine and welcome pathway to compliance. VAT exemptions on electric buses, bicycles, dialysers, animal feed raw materials and PPP infrastructure are sensible measures. The clarity introduced on trust taxation ensuring beneficiaries are not taxed on income already taxed at the trust level and the recognition of gratuity contributions as exempt income are also steps in the right direction.

Be that as it may, we cannot afford a repeat of June 2024. Parliament must discharge its oversight role with the seriousness this moment demands. They should not merely rubber-stamp what the Treasury has placed before it. Every clause must be scrutinised. Every punitive or ambiguous provision must be rejected or amended.

#FinanceBill2026 #PublicParticipation

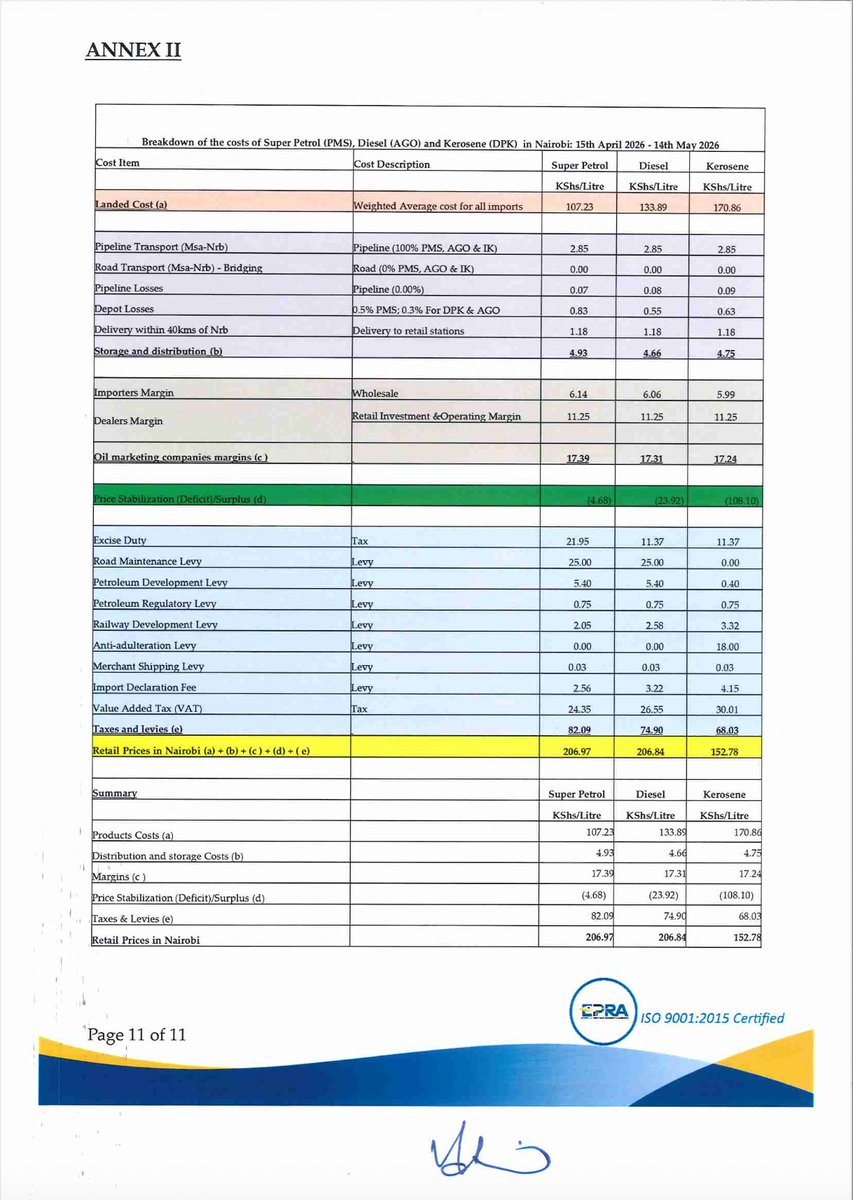

Quite a loaded release on Kenya's April 15th through May 14th pump price cycle:

1. Super Petrol increases by Kes 28.69/litre to Kes 206.97

2. Diesel increases by Kes 40.30/litre to Kes 206.84

3. Price of Kerosene remains unchanged

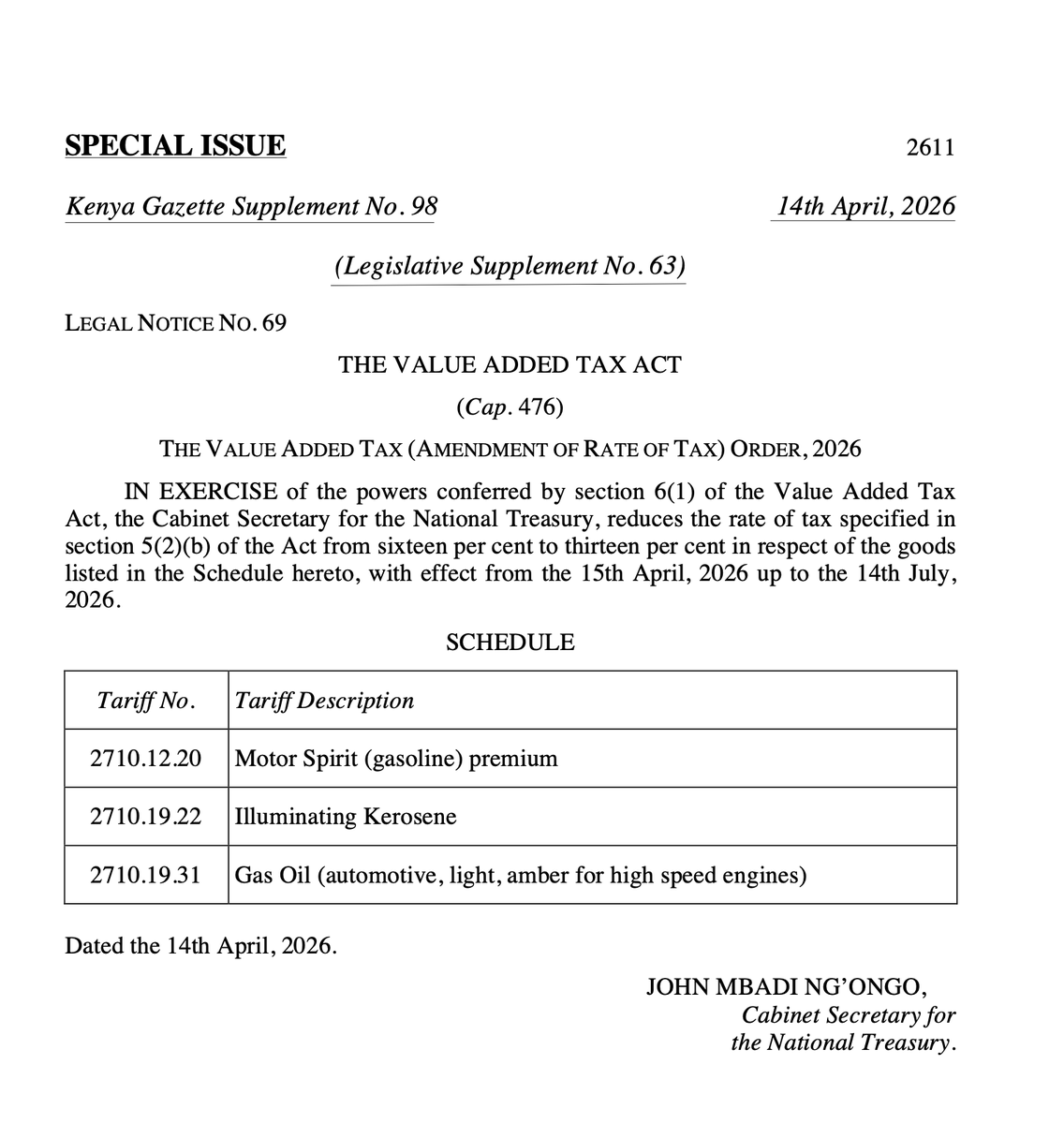

4. Value Added Tax on Super Petrol, Kerosene & Diesel have been reduced to 13.0% from 16.0%

5. GOK plans to use Kes 6.2 billion worth of Petroleum Development Levy to smoothen out the prices

I am the only person in my family that can torrent. My parents couldn't and my children don't have to. All this knowledge will die with me. Like tears in rain.