Senior Economist. Fed watcher at heart. Big fan of NIPA data. Vigilant about the US business cycle. Watching corporate and consumer debt (all opinions are mine)

US: Michigan 1Y ahead inflation expectations still quite sticky at 4.7%.

It might tempt the Fed to stay hawkish/keep pushing up rates as they believe they need to get back "ahead of the curve", ie. move rates above consumers' expectations.

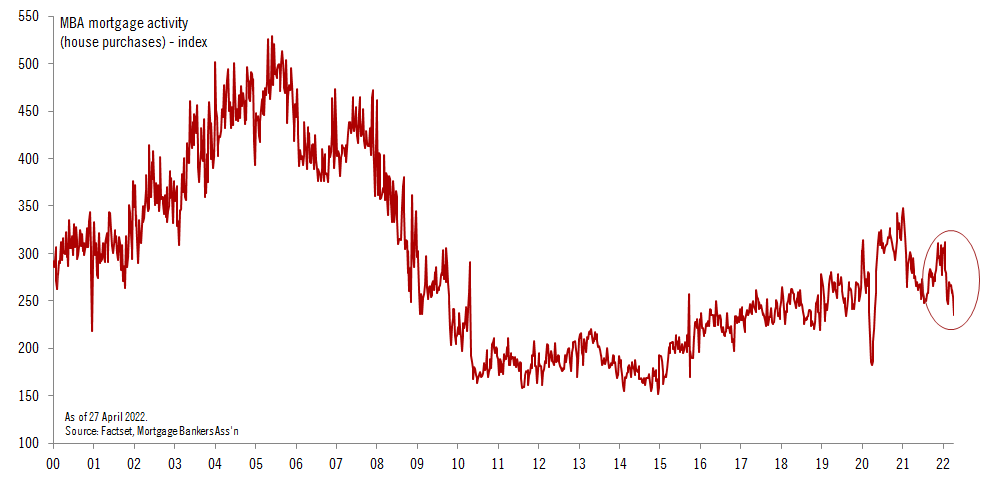

The laws of economics work: Sharply-rising US mortgage rates=>falling mortgage origination. And indeed, what a drop.

Housing sector is where one would expect the most immediate impact, but business investment and labour market may be next if Fed steps up further its hawkishness.

True, the Q4 ECI index abated a bit (1.0% q-o-q from 1.3% in Q3), but 'under the hood' some sectors including services are seeing massive wage pressure. Omicron is only likely to exacerbate the situation - let's see in 3 months' time.

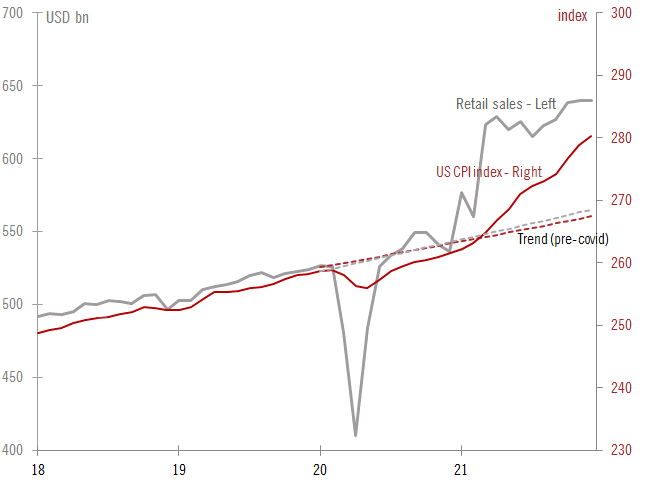

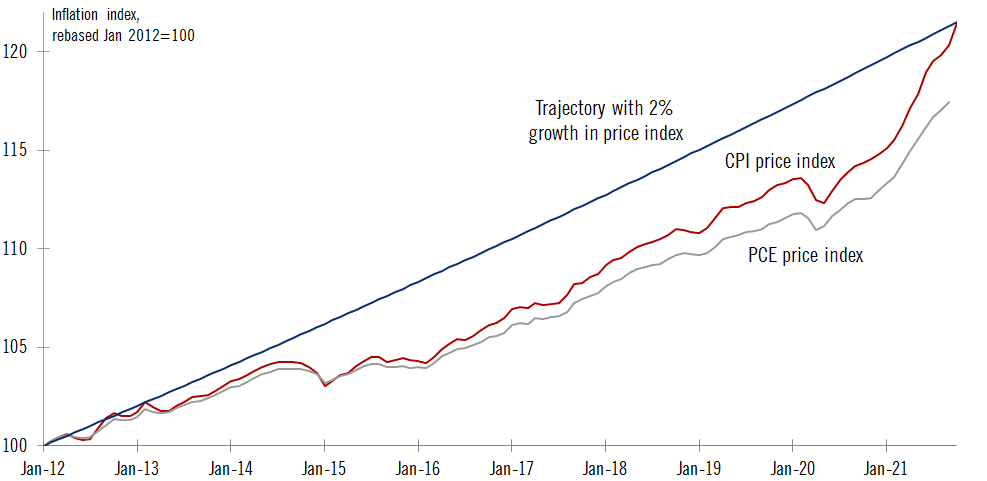

US CPI #inflation still mostly a function of disrupted supply chains (as we see in car prices), but we can't ignore strong US consumer demand too as a major additional driver (thanks to especially generous fiscal spending).

Graph below: retail sales (in level) vs. CPI index.

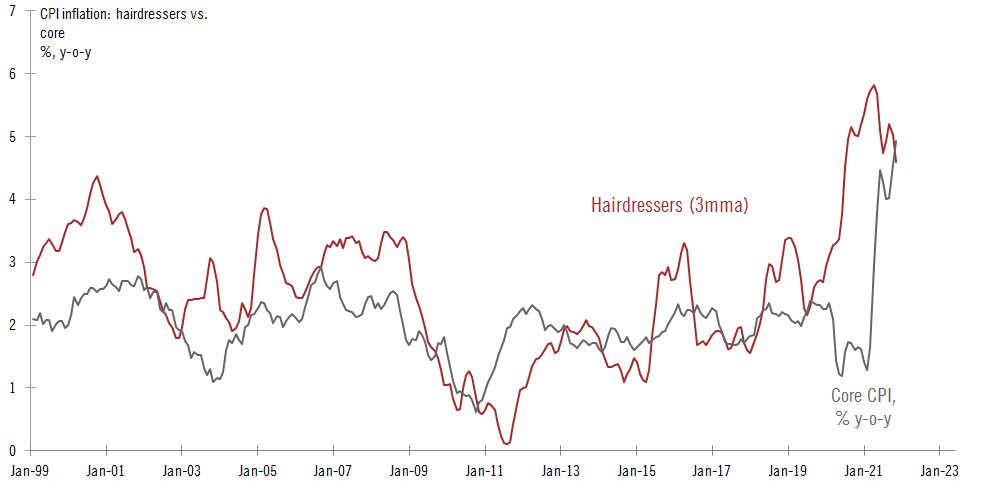

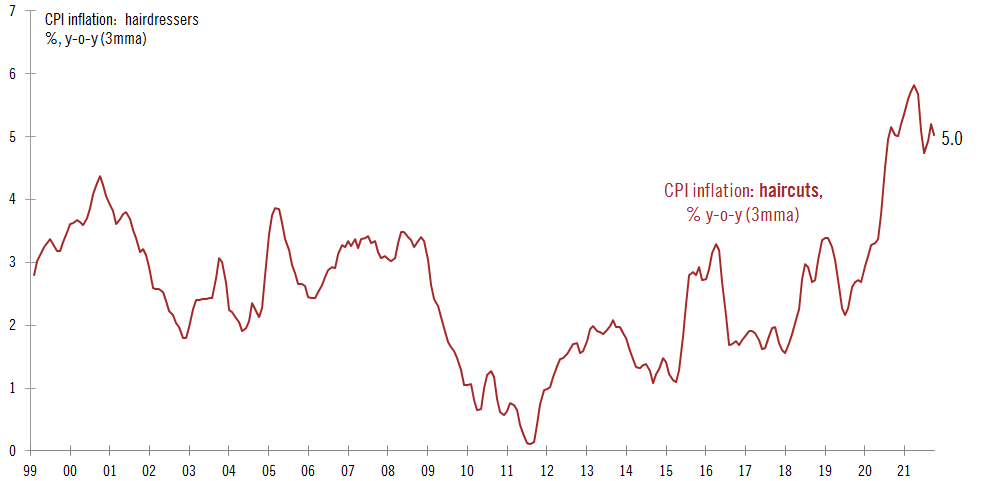

US inflation: Grist to the mill of 'Team Transitory', the haircut price index is already moderating. Peaked at 5.8% yoy (3mma) in April 2021.

4.6% yoy (3mma) in November 2021.

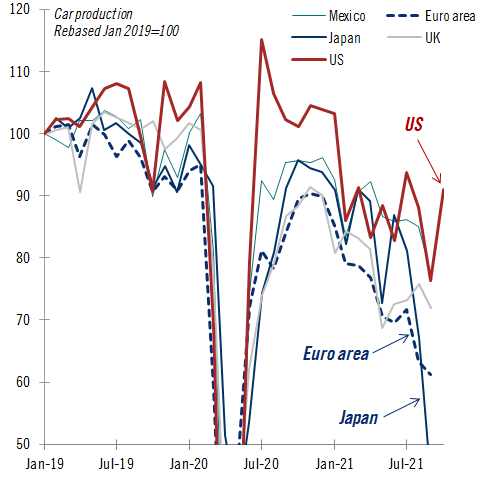

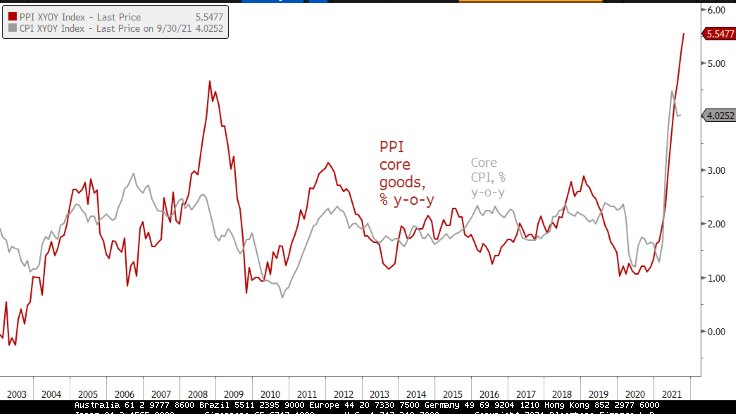

The sharp rebound in US car production in October may indicate we might be past the point of 'peak bottlenecks' and 'peak semi shortage' -- also at the global level.