Question: why wasn't Halaand's blatant shirt pulling (adding onto time wasted) not a yellow card offence? It would have been a 2nd yellow.

#LIVMCI#pgmol#epl#Liverpool#FPL#FPLCommunity

@Anirbban Have been following you passively. Not doing any trade. Just following. If I want to be active and subscribe, as complete novice to the market (even the language and abbreviations) where do you suggest I start?

@Rory_Talks_Ball So the ref called penalty, when Saka got the ball. Why shouldn't the ref take this into consideration when he is overturning an advantage?

@Arsenal_rep1 Question - Ref blows the whistle for penalty, when Saka had the ball and was onside. Why? And if he had to overturn, was this taken into consideration?

@ipo_mantra sir, why was there no post on Knowledge REIT? Was waiting for an update since REITs are something that I have no clue about. #firstquestion

@wild_haathi hello sir, I am messaging on behalf of my School - Nirmal Bhartia School (https://t.co/o3ffgMyqZ2) - we wanted to collaborate with you / WTI. Could we connect on call please?

@Anirbban

Recent follower here. Will you do an AMA session? Especially about abbreviations for an absolute novice. Or share some self-reading (not much of a visual or auditory learner). #AskAnirban

@Aunindyo2023 I remember when the Grd 8 went for their outstation trip on an overnight train, children were seeing a sleeper compartment for the first time, terribly confused on how to climb to the upper berth. Parents were more worried; more so because the train was from Nizamuddin.

🗝️NPS: Building Tomorrow's Stability Today - Pension for a Secure Retirement🧓👴

Brief History:

The National Pension Scheme was launched in India in 2004, initially for new government employees and later expanded to all citizens on a voluntary basis. The Pension Fund Regulatory and Development Authority (PFRDA) oversees the NPS and regulates the pension sector in India.

You can choose from various pension fund managers in India for your NPS investment:

1. 🌞 Birla Sunlife Pension Management Limited

2. 🏦 HDFC Pension Management Company Limited

3. 🏛️ ICICI Prudential Pension Funds Management Company Limited

4. 🏦 Kotak Mahindra Pension Fund Limited

5. 🏢 LIC Pension Fund Limited

6. 🔍 Reliance Capital Pension Fund Limited

7. 🏦 SBI Pension Funds Private Limited

8. 🌐 UTI Retirement Solutions Limited

After selecting a pension fund manager, you have two investment options: Active and Auto

The Active Choice: 😎

In this investment choice, the subscriber has the authority to actively decide how their contributions are invested. They get to pick the Pension Fund Manager, the types of assets (📈 stocks, 🏢 corporate debts, 🏦 government bonds, or alternative 💼 investments), and specify the percentage allocated to each.

It's like creating a personalized investment portfolio representing these diverse choices.

The active choice helps to choose from different % allocation of asset class -

Asset class E - Equity and related instruments. 🤑

Asset class C - Corporate debt and related instruments. 💶

Asset class G - Government Bonds and related instruments. 💸

Asset Class A - Alternative Investment Funds including instruments like CMBS, MBS, REITS, AIFs, Invlts etc. 💹

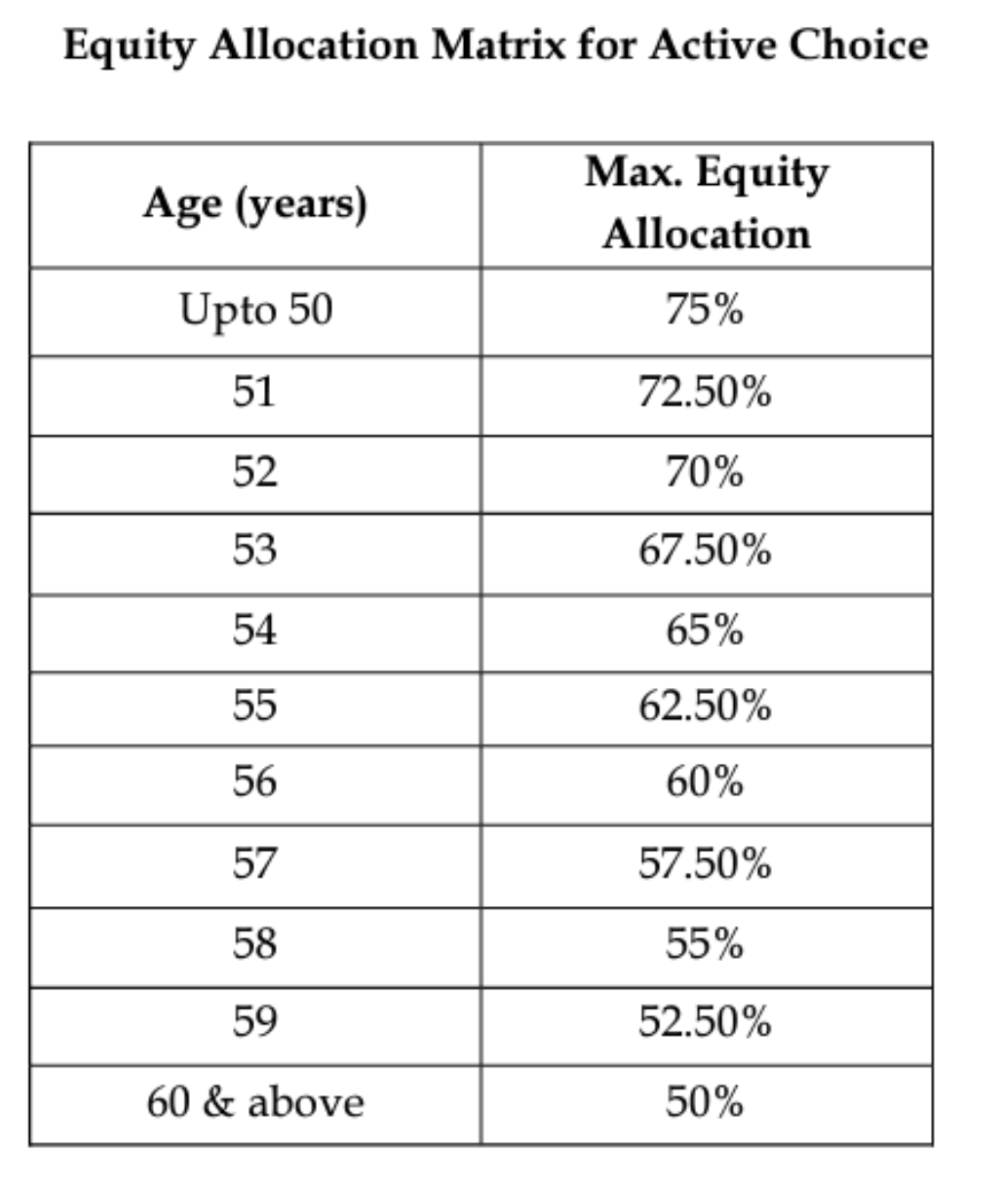

See below the maximum equity allocation allowed as per the age of subscriber -

The Auto Choice:🪙

Auto Choice suits those seeking a gradual reduction in risky investments as they age, trimming exposure to equity and corporate debt. Within 'Auto Choice,' three options cater to various risk appetites – Aggressive, Moderate, and Conservative. These funds adapt allocations to suit changing risk preferences, just like emojis adapt to express different feelings.

Tax Benefits & Withdrawal Details for NPS Subscribers:⬇️⭐

1️⃣Exclusive Tax Benefits for NPS Subscribers:

Under sections 80CCD (1B) and 80C of the Income Tax Act, 1961, NPS subscribers can enjoy significant tax benefits. They receive an additional deduction of up to Rs. 50,000 in their Tier I account under 80CCD (1B), in addition to the Rs. 1.5 lakh deduction available under 80C.

2️⃣Tax Benefits in the Corporate Sector:

For corporate subscribers, contributions made by employers (up to 10% of salary under 80CCD (2)) are deductible from taxable income.

Tax Implications upon Withdrawal EEE - Exempt, Exempt, Exempt

The other key investment options in EEE category we discussed in past -

🥇 PPF - https://t.co/zohOAcsYtL

🥈 SSY - https://t.co/z4bbh0Sl72

NPS follows an EEE tax structure:🎖️👩💻

Upon reaching 60 years of age:

- Maximum 60% of the corpus is tax-exempt upon withdrawal.

- The remaining 40% is mandatory to purchase an annuity, which becomes taxable income. This means the annuity payments received will be subject to taxation. #taxbenefits

Let's explore how a 25-year-old individual, consistently investing ₹10,000 per month, can leverage the compounding to build a substantial corpus. Assuming an average (ROI) of 10.5% over the investment period -🚀💰

⭐Investing ₹1,20,000 annually not only reduces taxable income but also harnesses the power of compounding! By consistently investing till 60, this generates an impressive corpus of ₹3,82,82,767. 💰

Excel sheet for your financial planning for retirement - https://t.co/Ufbr8qZeDP

⭐At 60, withdrawing more than ₹3 crores, where 60% is tax-free (totalling ₹2,29,69,660.2),remember the EEE benefit of NPS. 🏦

⭐The remaining 40% used for an annuity, estimated at 6%, brings forth a taxable yearly pension of ₹1,53,13,106.81 📈🔍 #nps

⭐ The monthly pension that comes out to be at the age of 60 will be ₹76,565.

Finally, we've assembled a collection of funds that have been around for at least a decade, along with their historical returns. Remember, past returns don't promise future outcomes, but they do paint a picture that can guide us. 📊🔍 We've curated a selection from ValueResearch

Thank you so much for reading! 📖📖

We teach Fundamental and Business analysis at SOIC :)

Over the past 3 years we have taught more than 10,000 students and spurred them on the journey of becoming a Complete Investor. #soic

Link to our SOIC Membership: https://t.co/H2p7Lxshos

Link for NPS Calculator: https://t.co/VkhwQR1rdR