China just cut Japan off again.

Dysprosium and terbium exports the magnets inside every EV motor have run at zero since January. Yttrium down 90%. The trigger: Takaichi's Taiwan remarks in November.

China makes 70% of rare earths and refines 90%. The leverage isn't the mining. It's the chokepoint.

Wrzucam kilka ciekawych wykresów, które mogą być przyczynkiem do dyskusji nad źródłami problemów eksportowych Niemiec (i UE) na tle Azji (w szczególności Chin). Również w nawiązaniu do "China shock 2.0"

Bill Gates just called AI the biggest technical thing of his entire life and said its influence is impossible to overstate.

the man who built Microsoft and lived through every tech wave of the last 50 years.

Bill Gates:

"there will be a frenzy. some companies will burn billions on data centers whose electricity is too expensive, and won't earn it back before the next generation of chips arrives"

everyone around him pushed him to stay quiet so the race wouldn't slow down, but he said it straight "this will hit the job market"

bookmark it and watch him break it down ↓

Folks say history never repeats. I say people’s behavior rarely misses beats.

T Minus 2 weeks to see what rhyme comes about this time.

If any at all, do we see another fall?

NDR's pattern matching tool shows that the NASDAQ has closely tracked the dotcom analog and is closer to 1998 than 2000. It still suggests near-term volatility ahead.

"A JPMorgan analysis last month found that more than 60% of data-center capacity planned for completion in 2027 isn’t yet under construction, and another 7% is delayed."

@wsj https://t.co/wN09gqgEc1

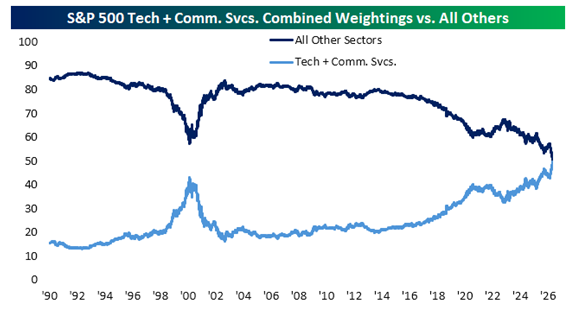

From @bespokeinvest:

Tech and Comm services now make up 49.6% of the S&P 500's market cap ... that is one percentage point less than the combined weight of all nine other sectors

⚠️This is INSANE:

Call options share has hit 70% of total US options market volume, the highest level since the MEME STOCK MANIA peak in 2021.

Over the last few weeks, the call options share has risen almost in a STRAIGHT LINE.

Overall, the total value of the S&P 500 call options traded has SURPASSED the S&P 500 market value by 300%.

Just 2 months ago, S&P 500 call options total notional value was 100% higher than the index market cap.

There is almost no appetite for put options. How does this end?

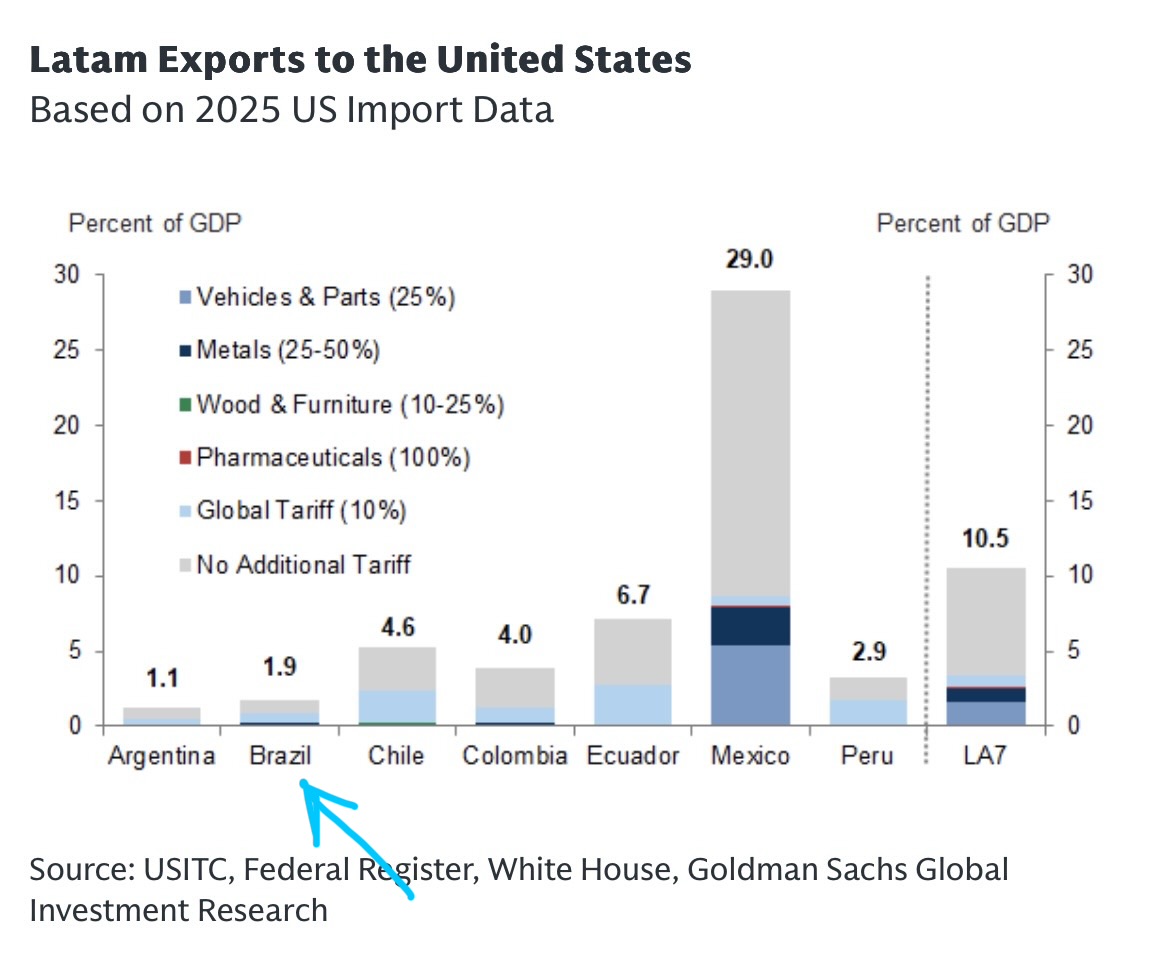

The 25% “replacement” tariff by the U.S. on Brazil’s exports (Section 301) will boost the effective tariff rate from ~10% to low teens, but the key number to keep in mind is that Brazil’s exports to the U.S. are <2% of GDP, so the overall macro impact will be limited (chart - GS)

The Iran war is accelerating dedollarization

CIPS is seeing RMB volumes surge.

- avg daily RMB transactions have 2x'd in the last 2 yrs

- +50% during the war

Non-stop sanctions have increased the risk of using the SWIFT system/USD.

🔴FOMO appears to have taken over the US stock market:

The 5-day moving average of the CBOE Equity Put/Call ratio is down to 0.43, the lowest level since the MEME STOCK MANIA of 2021.

In other words, the last time this ratio was this low was just before the 2022 bear market, when the S&P 500 subsequently fell -27%.

A low put/call ratio means investors are purchasing far more bullish call options than bearish put options.

This signals extreme confidence and a near-complete absence of hedging activity.

When positioning becomes heavily one-sided, markets have historically become more vulnerable to sharp reversals.

Cena technologii AI maleje w tempie 94 proc. rocznie, czyli czas potrzebny na spadek ceny o połowę to ok. 2,5 miesiąca. W przypadku rewolucji komputerowej było to ok. 4 lata, a rewolucji Internetowej 3 lata. Tempo deflacji jest dziś dużo większe niż podczas każdej poprzedniej fali innowacji.

Speculative bullish US Dollar bets are surging:

Long speculative positioning in the US Dollar is up to +$16.5 billion, the highest since February 2025.

This captures hedge funds and asset managers that take positions based on price trends and macro views rather than hedging needs.

Bullish positioning has TRIPLED over the last 2 weeks.

This also marks the 11th consecutive week of net long positioning, the longest streak since the 2024-2025 period.

Meanwhile, the US Dollar index is up +3% since late January, as the US economy has remained more resilient than other major economies amid the Iran War and global commodity supply disruptions.

Investor demand for the US Dollar is strong.

Most measures of labor market tightness still looser than they were pre-COVID, ranging from 1.5 standard deviations lower to 0.3 standard deviations higher. Of course, we don't know if things were neutral or loose or tight back then--I suspect tight already.