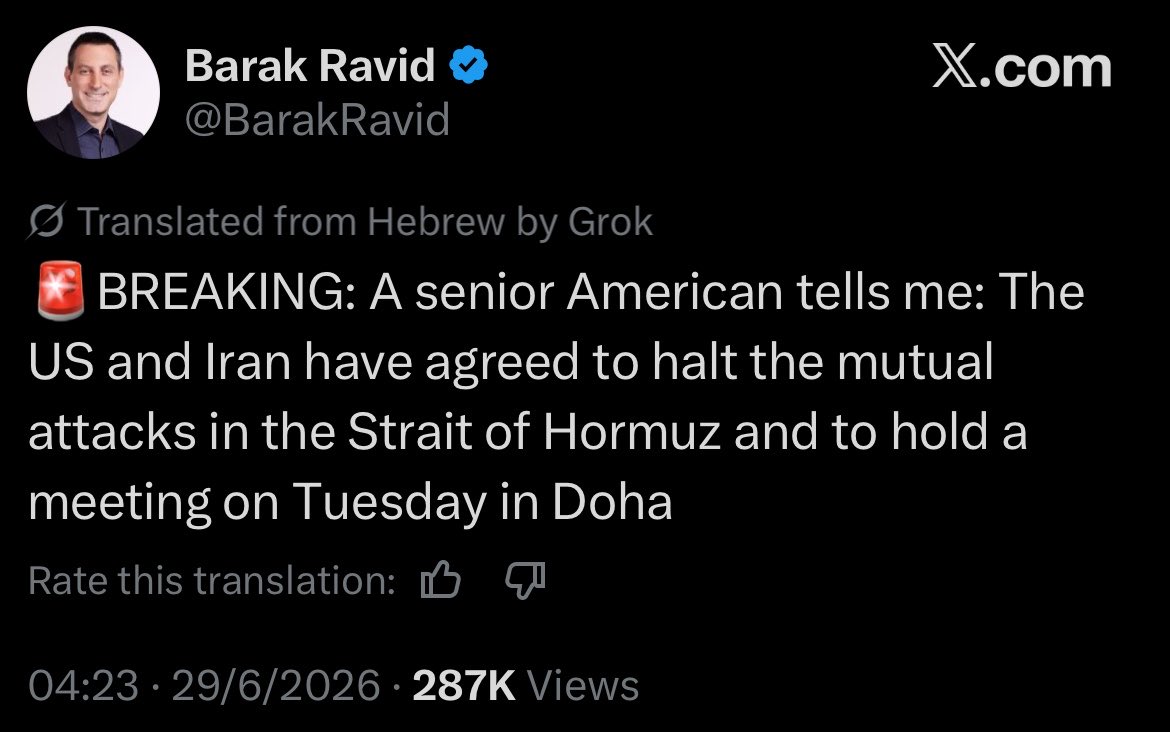

🇺🇸 🇮🇷 BREAKING: Negotiations between the U.S. and Islamic Republic have been cancelled

Meanwhile, the U.S. has launched its largest military deployment towards Iran.

More on Tousi TV later today…

US strikes Iran for breaking the ceasefire. Iran’s response? Bombing civilians in Bahrain and Kuwait. 🇧🇭🇰🇼

What kind of unhinged mentality is this? Can't face a superpower, so you target innocent Arab neighbors? Absolutely cowardly and pathetic.

KEY LIQUIDITY GAUGE TURNS NEGATIVE, FLASHING WARNING FOR U.S. STOCKS

The G10 Excess Liquidity Leading Indicator has fallen into negative territory for the first time since the 2021 inflation shock, signaling tighter global liquidity conditions. Because the indicator has historically led the S&P 500 by roughly six months, the shift is being closely watched as a potential warning of increased downside risk for U.S. equities if liquidity continues to deteriorate.

BREAKING: China imported +163 tonnes of gold in May, the largest monthly import since March 2024.

This marks the 3rd consecutive month with gold imports exceeding +150 tonnes.

As a result, in the first 5 months of 2026, total gold imports rose +76% YoY, to +692 tonnes.

This has been driven by strong retail demand for physical bullion bars and gold accumulation plans, low-cost products that allow investors to build up gold holdings gradually over time.

Meanwhile, the People's Bank of China added +10 tonnes of gold to its official gold reserves in May, its 19th consecutive monthly purchase, bringing total holdings to a record 2,331 tonnes.

China’s demand for gold remains strong.

Iran is growing frustrated:

💰 It got ZERO money yet

🛢️ Oil sanction relief is being proved meaningless (no new country willing to buy their oil)

🇴🇲 Ships are crossing the Omani side of Hormuz

🇱🇧 Lebanon signs agreement with Israel to disarm Iran's Hezbollah

1970s vs. Today📈📉

When you measure today’s inflation using the exact 1980 methodology (accounting for surging mortgage rates and direct housing costs instead of modern rent calculations), the structural parallels are undeniable:

The Yield Curve : In both eras, aggressive central bank rate hikes forced deep, prolonged 10Y-2Y inversions.

Today, just like the mid-70s, the curve has un-inverted (+0.31%) as monetary policy hits a hard ceiling. The Inflation Double-Hump : Under the old math, our 2022 post-COVID inflation peak didn't stop at 9%..it actually surged to 13.1%, eclipsing the first 1974 oil shock wave. Today's "inflation echo" sits at a true cost-of-living contraction of 8.8%, driven by rising global energy blockades.

⚠️ The Cracking Foundation: The dangerous divergence.

The grey GDP bars. While headline GDP still shows a fragile 2.1% growth, it is heavily distorted by trillion-dollar deficit spending. Stripping away the government debt injection reveals that private-sector demand is choking under the weight of an 8.8% real inflation rate.

In 1974, it took time for the economy to completely break under the pressure...today's data suggests we are on that exact same trajectory.

We are living through a 1970s inflation shock, and the illusion of a resilient economy is rapidly running out of time.

For one's private perusal

Enjoy.