“The blockchain solved cross-border payments, and anyone still struggling just hasn’t adopted them yet.”

This is basically nonsense. A common sentiment, and not entirely unjustifiable, but basically nonsense.

Sit in any payments company pitch in 2026 and you'll hear "instant blockchain settlement" within the first five minutes. People nod along because it’s partially true. We all pretend that moving stablecoins between wallets was the thing that needed solving.

But we all know there is more to it than that.

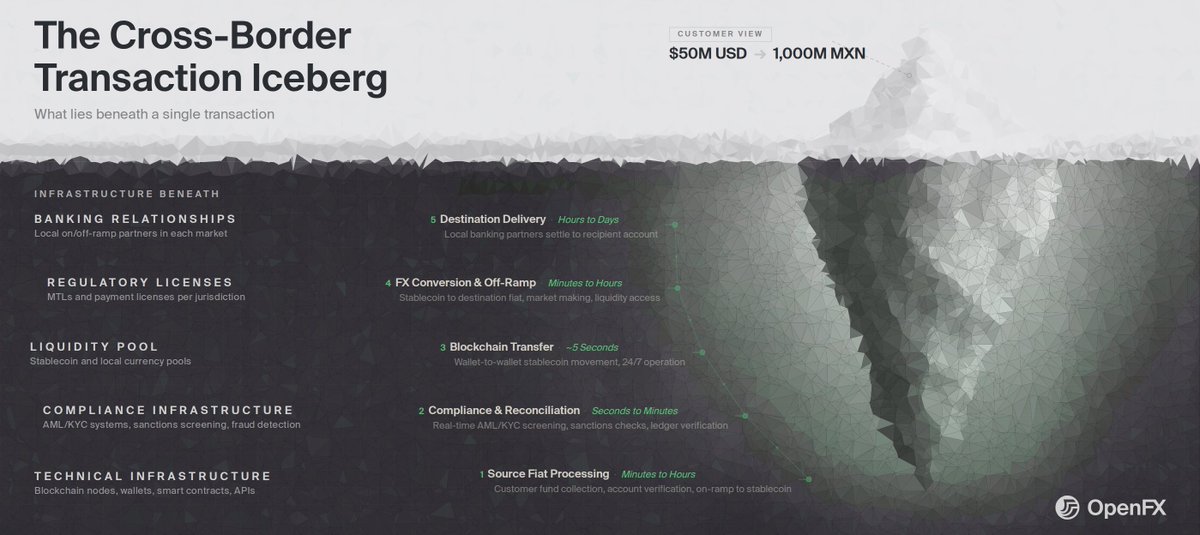

If you've ever actually tried to get $50 million through an exotic corridor on a Saturday night, you know the blockchain transfer is the least of your worries. Maybe 1% of the problem.

Here's what everyone knows but rarely talks about in the marketing copy:

Before that five-second transfer can happen, you need to clear that $50M through domestic banking rails. Run compliance screening. Handle the edge cases that trigger manual review. Get the money on-chain in the first place.

After that five-second transfer, you need liquidity in the target currency. Not thin liquidity that slips when you execute at size, but actual depth. That makes banking partners willing to take your calls after getting home from their kid’s soccer game.

Then you need to navigate local payment rails that work differently in every jurisdiction. Then you need to land the funds in a bank account that's willing to receive them.

The blockchain transfer sits in the middle of all of this – fast, commoditized and largely irrelevant.

Exotic corridors don't fail on-chain. They fail at the off-ramp. They fail because not many people have those kinds of banking relationships. They fail because liquidity doesn't exist at the depth you need between BRL and AED. They fail because for a long time everyone was worried about moving G3 dollars a micro-second faster, and almost no one focused on building rails the rest of the world could use.

Here at OpenFX we say that we want to "move money like data.”

But what does that mean?

That means caring about every part of the transaction – the iceberg, above and below the surface.

It also means caring more about emerging markets and exotic corridors, where these problems are even more acutely felt.

Blockchain as a selling proposition is over. Wallet-to-wallet transfers are fully commoditized.That part of the game has been won, what matters now is whether the money wallets move actually lands in the account your supplier can access, in the currency they need, on the timeline you promised.

That's an operations problem. An infrastructure problem. A relationships problem.

The kind of hard problem we were built to solve.

Look guys, it's actually really straightforward, a bunch of people staked their ETH on the Ethereum blockchain to earn yield, except they didn't want their capital to be locked up, so they actually staked with a liquid staking protocol called Lido who provided them a liquid staking receipt token called stETH, except they decided to juice their yield further by depositing their stETH receipt tokens into a restaking protocol called Eigenlayer, except they didn't want to lock up their capital, so they actually restaked with a liquid restaking protocol called KelpDAO who provided them with a liquid restaking receipt token called rsETH, except they decided to juice their yield further by depositing their rsETH tokens into a lending protocol called Aave so that they could open a leveraged looping position that borrows ETH against the rsETH collateral and restakes the ETH into rsETH which is then deposited as collateral, except it turns out rsETH used a cross-chain bridge called LayerZero that was hacked by north koreans causing rsETH to become undercollateralized and now these looping positions are stuck and unprofitable, and everyone is pointing fingers at each other, and also DeFi is a very serious industry

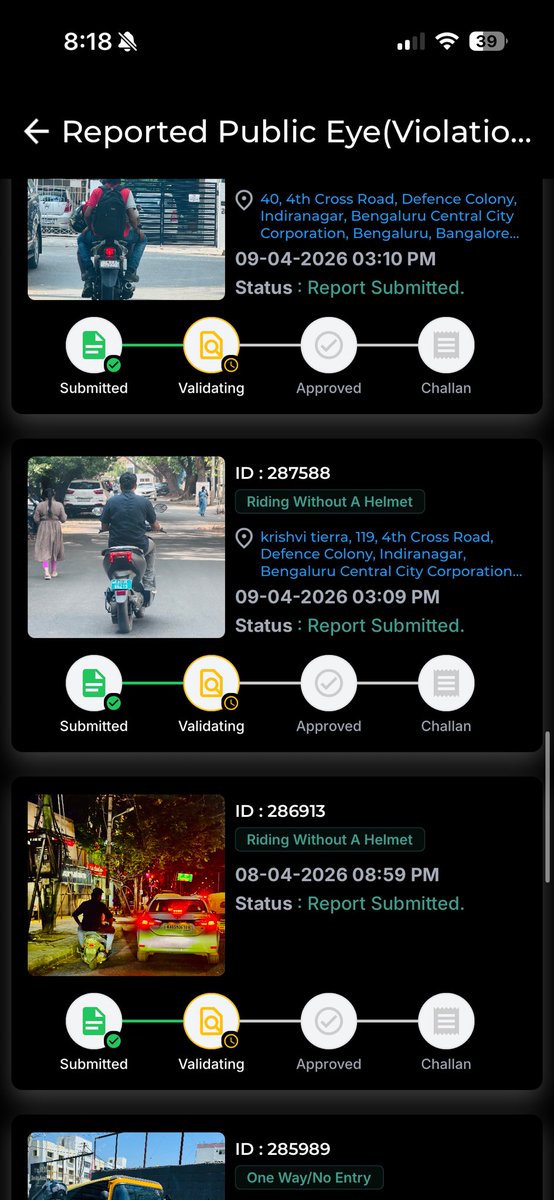

Loved how they respect traffic rules, basic safety, honouring traffic lights.

Fyi for -

@blrcitytraffic@BlrCityPolice@Jointcptraffic

Compliant uploaded multiple times on ASTraM App but no action on any report.

According to J.P Morgan, in 2024 there was over $200 trillion in annual cross-border payment volume. And it's expected to surpass $300 trillion within the next several years.

@openfx_ is tackling one of the largest market opportunities that exits.

Don't miss my interview with @prabhakar2reddy to learn more about OpenFX and how he see's OpenFX changing the way money moves around the world.

We came out of stealth nine months ago at $8B in volume. As of February we crossed $45B. Revenue is up 10x.

This week we raised a $94M Series A.

@Accel, @atomico, @FactionVC, @northzoneVC, @M13Company, @PanteraCapital, some of the biggest names on both sides of finance chose to back us.

You might be wondering why.

1/ yesterday, the largest position in hash3 announced $94m in funding

openfx provides fx infra for real-time cross-border payments and has reached $50B of annualized tpv within 22 months of launch

hash3 has quadrupled down since seed. some reasons why you should pay attention

There are two ways to touch 8 billion lives: acquire 8 billion individual customers, or build the infrastructure for the institutions that already serve them.

We chose the latter.

Today we're announcing OpenFX’s $94M Series A from @Accel, @atomico, @FactionVC, @M13Company , @northzoneVC, @PanteraCapital, and with support from existing investors @flybridge and @hash3xyz.

🧠 GRPO vs PPO — what's actually different?

1️⃣ Dynamic KL Penalty (w₁ · D_KL):

GRPO adapts how hard it punishes policy drift using a tunable weight w₁.

PPO uses a fixed KL or ignores it entirely — GRPO makes regularization smarter.

2️⃣ Explicit KL Regularization:

PPO indirectly controls change via the clipped loss.

GRPO directly adds KL divergence as a penalty term, making updates more aware of past behavior.

3️⃣ Fine-Grained Control:

GRPO separates exploration-exploitation tradeoff via w₁, letting you tune learning style.

PPO’s clip ratio is coarse and static — GRPO gives you a finer steering wheel.

🎯 Bottom line: GRPO = PPO with knobs that let you feel the road.

🧠 GRPO vs PPO — what's actually different?

1️⃣ Dynamic KL Penalty (w₁ · D_KL):

GRPO adapts how hard it punishes policy drift using a tunable weight w₁.

PPO uses a fixed KL or ignores it entirely — GRPO makes regularization smarter.

2️⃣ Explicit KL Regularization:

PPO indirectly controls change via the clipped loss.

GRPO directly adds KL divergence as a penalty term, making updates more aware of past behavior.

3️⃣ Fine-Grained Control:

GRPO separates exploration-exploitation tradeoff via w₁, letting you tune learning style.

PPO’s clip ratio is coarse and static — GRPO gives you a finer steering wheel.

🎯 Bottom line: GRPO = PPO with knobs that let you feel the road.