Companies that raced to put AI tools in the hands of their workers are starting to rein in their use, as the cost of deploying the technology at scale begins to test corporate budgets. https://t.co/Dr2rwpEBlc

"bubble concentrations" of the US stock market in the spring of this year, shown by Michael Harnett at the Bank of America. More featured on today's Chartbook Top Links in the comment below.

The situation with oil is worse than you think.

The oil wells of Iran, Iraq, Kuwait and the UAE are not like a garden hose. They are mature, low-pressure reservoirs that require precise gas injection to maintain flow. Once that flow stops, water encroachment -- what engineers call water coning -- traps oil behind barriers of saltwater that are nearly impossible to reverse. Worse, paraffin waxes and asphaltenes precipitate inside the wellbore tubing, clogging the rock pores with solid deposits.

This is not theory; it is basic petroleum physics. The recent Israeli strike on Iran's South Pars gas field -- the largest in the world -- caused a lasting shock to the entire regional energy system. When the field was hit, the pressure dropped across hundreds of wells. Even if peace breaks out tomorrow, those wells will never produce at their former rates without expensive re-drilling that takes years. The same applies to Qatar's Ras Laffan LNG complex, which was struck by Iranian missiles in retaliation. These are not temporary shutdowns; they are permanent fractures in the energy backbone of civilization.

Industry studies show that even short shutdowns of five days to a few weeks cause flow rate losses of 20-30%. The wells in Kuwait never fully recovered after the Desert Storm fires, and that was with only a few months of disruption. Now we are looking at months of no production, with many fields flaring gas instead of exporting it.

The Strait of Hormuz closure has already removed a significant share of global energy, and rising energy costs are triggering cascading impacts across industries, including food and transportation. Every day the strait remains closed, the invisible tax on global oil supply grows larger -- not just from lost barrels, but from the permanent impairment of the reservoirs themselves. The world could lose 4 to 6 million barrels per day of capacity even after the strait reopens, and that means higher prices for years.

Read the full article here:

No Way Out: Why Permanent Damage to Persian Gulf Oil Wells Begins Now

https://t.co/2ZkeNCib95

🛢️ JP Morgan Warns Oil Market Out of Balance, Prices Must Rise

🔸The closure of the Strait of Hormuz, through which roughly 20% of the world’s oil flows, has removed 13.7 million barrels per day from global supply in April alone. A JP Morgan research note warns the market has no good way to replace it.

🔸Normally, spare production capacity in Saudi Arabia and the UAE acts as the market’s shock absorber. But that buffer has effectively been removed, eliminating the system’s first line of defense.

🔸With spare capacity unavailable, markets turned to inventories

➤ Global stockpiles are now being drained at ~7.1 mbd in April, an extraordinary pace, according to the note.

🔸Meanwhile, demand is collapsing because supply simply isn’t reaching users — “forced demand destruction.”The hardest hit sectors include:

▪️ Petrochemical plants across Asia are shutting down or slashing output as LPG, ethane, and naphtha flows from the Gulf collapse

▪️ Airline jet fuel costs account for 11% of total demand loss, with Middle East routes largely grounded and margins under pressure

🔸Even after accounting for falling demand and emergency reserve releases, JP Morgan says a gap of 2.3 million barrels per day remains with no clear fix.

🔸U.S. shale is the only large, flexible supply source left, but it can’t scale fast enough. JPM stresses shale needs 3–6 months for meaningful output gains, and 6–12 months for large increases. That’s too slow for a shock happening now.

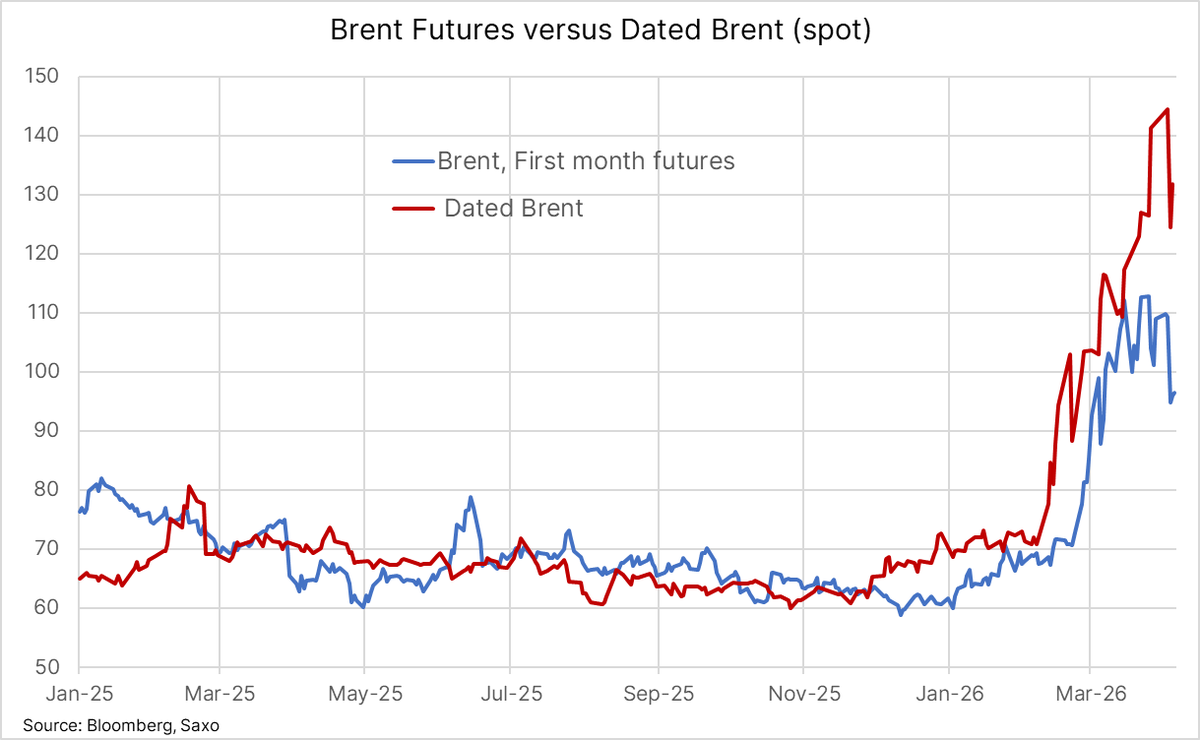

🔸Brent prices diverged in April, with futures averaging about $99.7 per barrel while physical “dated Brent” rose to $121.6, signaling tighter real-world supply. The note concludes prices are high, but likely not high enough yet to fully reflect the shortage.

@Big_Orrin@Nowyoutellme4 The main problem is the assumption that financial markets will always incorporate all information in an unbiased way, and thus are best placed for price discovery. Physical markets bank on this. Yet in reality that is not the case due to various biases and speculation or panic.

@Big_Orrin@Nowyoutellme4 But is not the fact that the physical oil market price is much higher than the front paper oil price demonstrating that physical buyers ignore the paper price when not representative? Problem is then: what is the point of the paper price if ignored...

When a private credit manager writes a report titled “Private Credit: An Honest Assessment”, you pay attention.

Sona just did. 17 pages. It is the bluntest insider critique of the asset class I have read.

Here is what matters for you 🧵

In appreciate all your questions about disconnect between physical and financial markets. My answers are summarized in this short paper.

#oott

https://t.co/QukGUcPRbV

North Sea crude prices for immediate delivery continue to highlight mounting stress in the physical market, as European and Asian refiners scramble to secure cargoes to replace volumes lost during the month-long blockade of the Strait of Hormuz.

Dated Brent—a key benchmark for physical North Sea shipments—has moved sharply into focus given the signal it provides on overall market tightness. It rose 7% yesterday to USD 132, while the June Brent futures contract lingered around USD 95, underscoring the growing dislocation between prompt supply and forward pricing.

Data from LSEG, cited by the Financial Times, show Forties Blend—another marker for immediate delivery—trading close to USD 147 per barrel on Thursday, further highlighting the acute strain in spot markets.

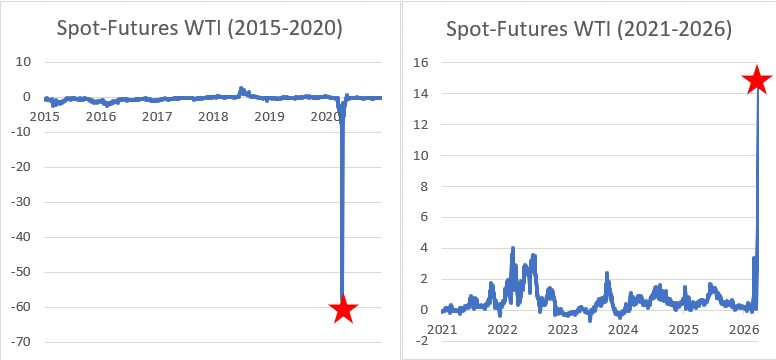

My model of the squeeze is now completed with a great case study: Time spreads are just derivatives of stochastic inventories with boundaries given by tank-tops and stock-out. Covid gave us one, last week gave the other - the rest is just algebra.

#oott

https://t.co/IupMqy0Apm

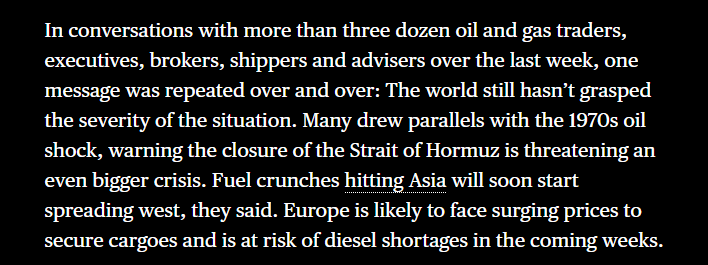

The biggest oil supply shock in history has reached the one-month mark

And the energy industry is warning that the crisis is only beginning 👇⚠️

https://t.co/AZ661hxNtt