Sydney has been the most unaffordable housing market in AUS most of the last 30 yrs.

Now Brisbane is very rapidly catching up.

This hasn’t happened since the mining boom & GFC 2007-2009.

2.1 avg incomes are required in both capitals to comfortably service a typical mortgage.

Heading into 2026, thanks to rapid dwelling price growth, rising interest rates and only modest income growth, it now takes over 1.8 average incomes to comfortably service a mortgage on a median priced dwelling.

Housing affordability in Australia is at its worst in over 30 years.

Unfortunately, we don't know exactly when housing was less affordable than now, because our data only goes back to 1994.

Recent headwinds (interest rates, Iran, Budget) threaten this new trend:

- Inflation & interest rate pressures could ease but at the cost of higher unemployment

- Or the public sector may step in again as the prime growth engine, keeping inflation & interest rates elevated

Since the GFC, the public sector has been creating jobs around four times faster than the private sector.

Heading into 2026, things were looking more optimistic for those wanting the private sector to return as the prime engine of economic growth in Australia ...

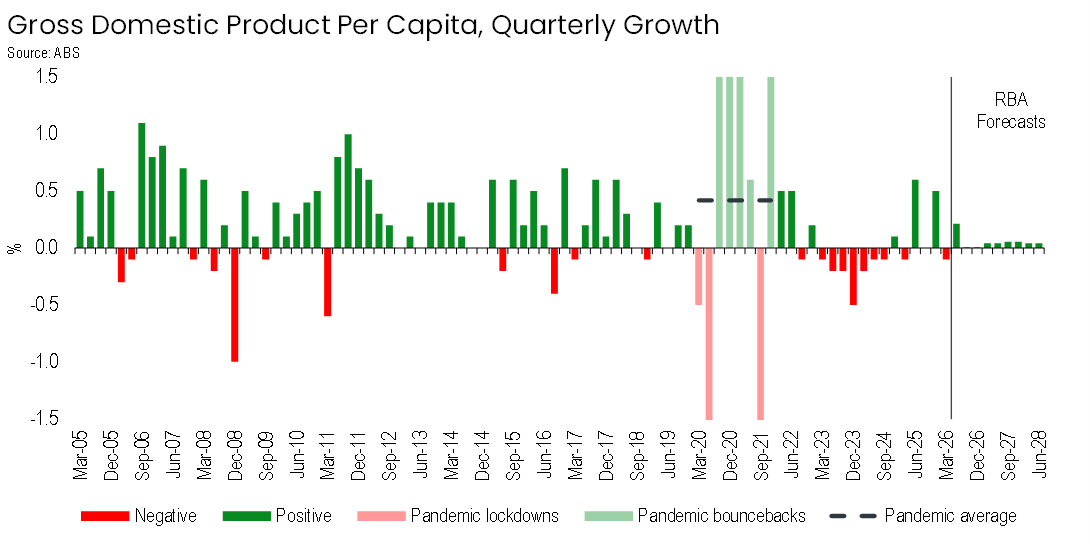

Australians are individually 2.4 per cent ‘poorer’ than their pre-pandemic trajectory would have projected (which was already a weak trajectory).

Based on RBA forecasts, they’ll be 3.8 per cent ‘poorer’ than this trajectory by mid-2028.

A few 'interesting' insights from this week's AUS GDP data:

The data centre boom is largely imported so it's impact on GDP is muted (at least for now).

AUS is back in ‘per-capita’ recession, with only 4 of the last 15 quarters showing positive per-capita GDP growth

And based on RBA forecasts, per-capita GDP will be just a rounding error about zero over the next couple of years.

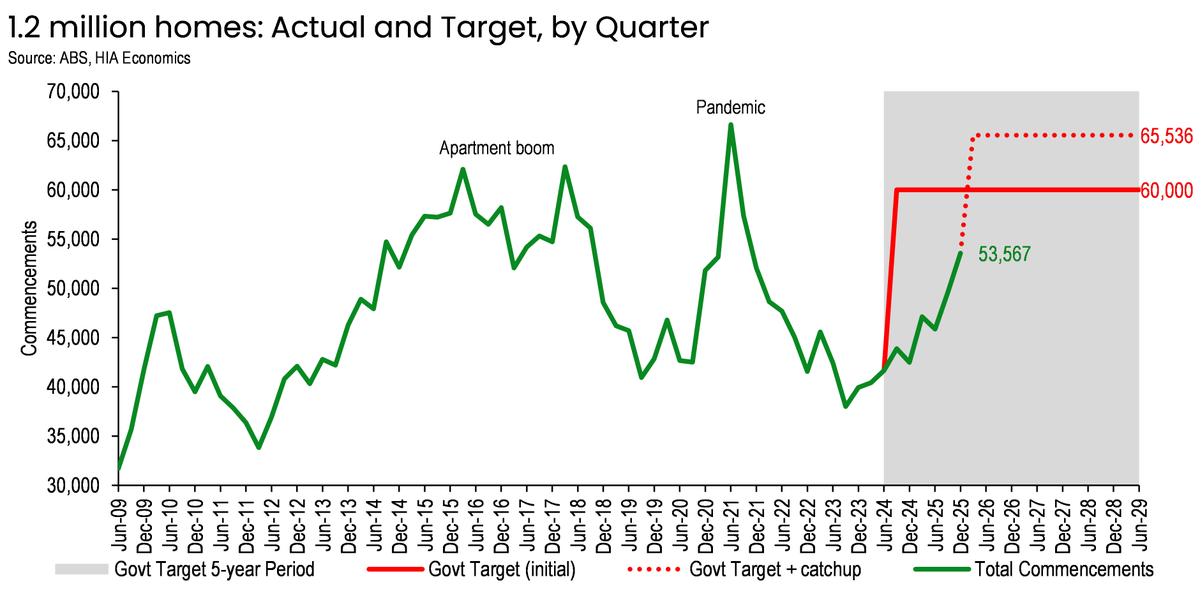

Nice surge in commencements in 2025, driven by higher density housing (apts, units, townhouses, etc)

Still a bit of catchup to reach govt's target of 60k per qtr between Jul-2024 and Jun-2029 (now >65k per qtr required)

That's before addressing a pre-existing 2m homes shortage.

With interest rates on the way up again, policymakers need to find other ways to reduce the cost of bringing new homes to market:

- Lower taxes

- Faster land release & fairly-funded infrastructure, especially transport and utilities

- Streamline planning & approvals processes

Well now, that's interesting!

Almost $100 million worth of 'prefabricated buildings' imported into Australia in February.

Is the granny flats boom here?

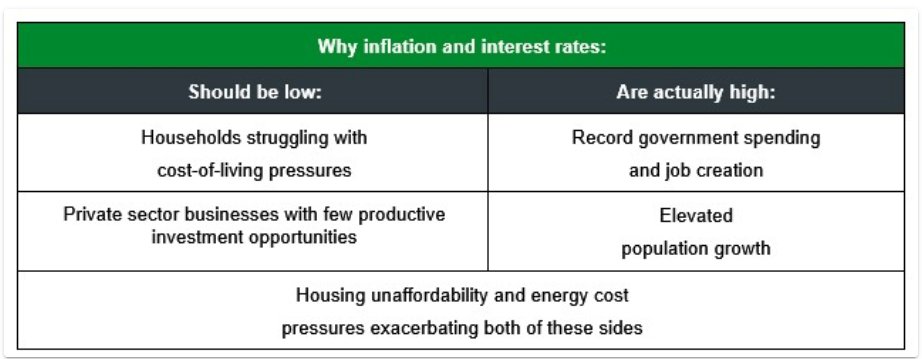

Today's RBA decision to hike was split 5:4.

Nonetheless, it reinforces Australia's dangerous dichotomy:

Households and businesses will be even more constrained.

The variables actually driving inflation - govt, population growth, housing and energy costs - will remain.

The myth that AUS has enough housing - that investors just own too much of it - needs to be confronted and debunked because it is worsening the housing & homelessness crisis across the country.

We absolutely have a housing shortage & we need more.

https://t.co/lxxZ76sa0g

The no. of households is what matters for housing demand, not just population growth.

Investors don't add to housing demand, they add to supply.

We would not have 1% rental vacancy rates if there were 'too many investors'.