Check out my Senior Season #footballhighlight#ohiofooball

RB: 29 TDs, 1,639 yards, 8.8 yards per carry. 🏈

2nd Team all Ohio Division 5 🥈

1st Team All District Southwest Ohio Division 5 🥇

1st Team All League X2 🥇

https://t.co/zO2E3E04Hy

What sensible forward thinking cutting edge leading nation is having a DEBATE on whether or not there should be VOTER ID?!?!!!! Like?!?!? They’re actually fighting NOT to have ppl present ID while voting for your leaders!!!!! Do you get it?!?!!!! Do you get it now?!?!!!

Brokers continue to spread the narrative of tariffs causing inflation.

Tariffs may affect some individual prices (if they are entirely produced in one nation and with inelastic demand, which is exceedingly rare) but not aggregate prices.

Inflation is the loss of purchasing power of the currency manifested in the rise of aggregate prices denominated in that currency. This is only caused by currency printing.

Graph via JP Morgan.

It is difficult to eliminate the Income Tax and offset the receipts with tariffs, but the Trump administration certainly has ample room to simplify and reduce the Income Tax brackets if government spending is curbed.

via Statista and Bloomberg

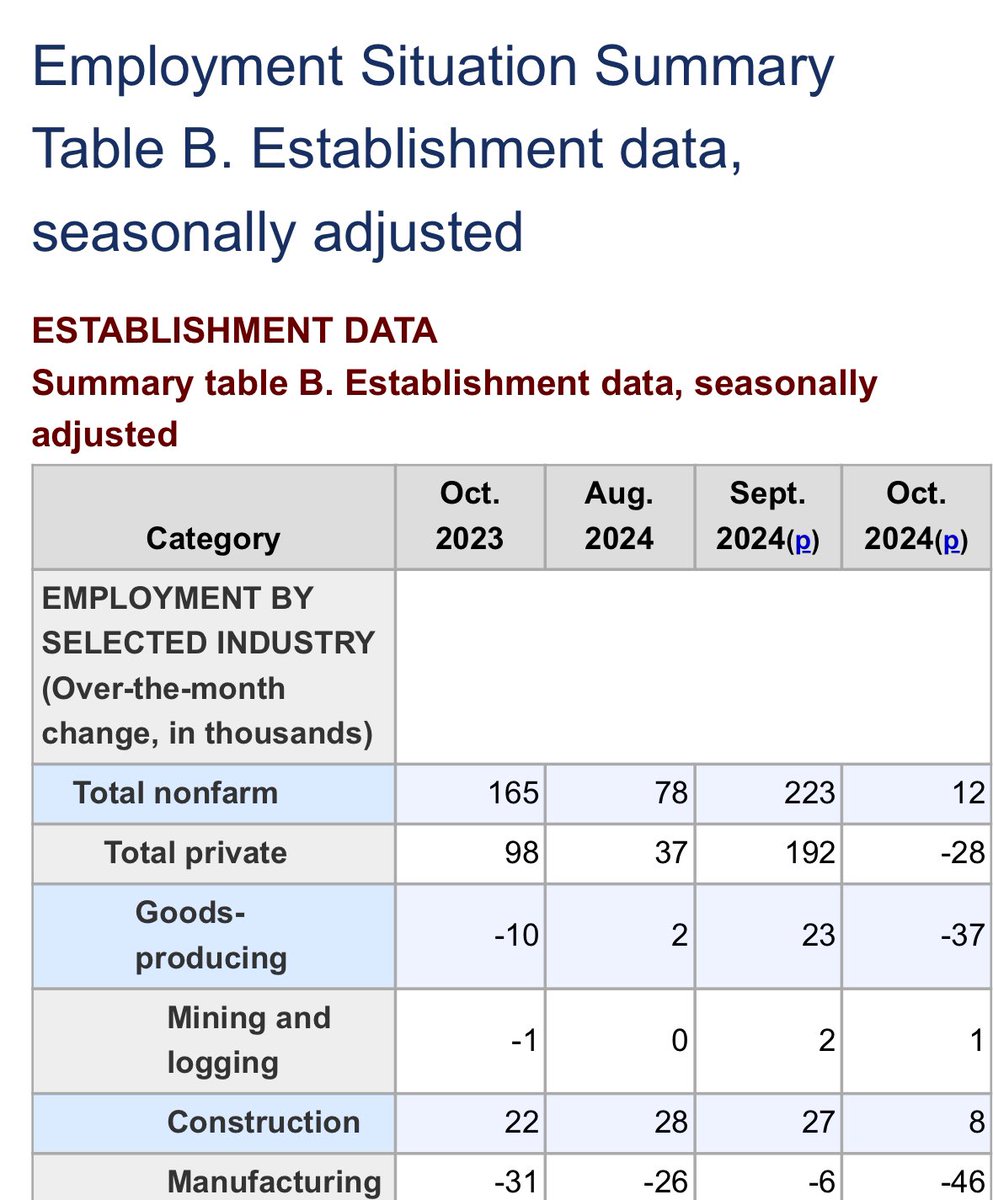

🚨WEAK US JOBS REPORT🚨

This was a very weak jobs report contributed to in part by strikes and hurricanes but there remain underlying weaknesses as noted below.

The establishment report shows the private sector lost 28K jobs last month, which was influenced by strikes and hurricanes, total jobs were revised down by 112K over the previous two months, and 3-month average of just 67K in the private sector.

The household report shows the labor force declined by 220K last month, employment down 368K, and unemployment up 150K, which is why the unemployment rate stayed the same at 4.1%.

The labor force participation rate declined to 62.6% and is at the lowest rate since briefly in 2015 or 1978, excluding the COVID lockdown period.

Average weekly earnings are up 4% over the last year and have outpaced inflation in recent months but the losses in purchasing power for years has burdened Americans today and will continue to do so, as inflation-adjusted average weekly earnings are down about 3% since January 2021.

Details in pics or source here: https://t.co/iyjegF0Itn #jobsreport #economy

Excessive debt is driving the U.S. recovery.

Insane deficit spending is the norm.

In the case of the euro area, stagnation is the norm even with massive debt-fueled stimulus.

Graph via JP Morgan.

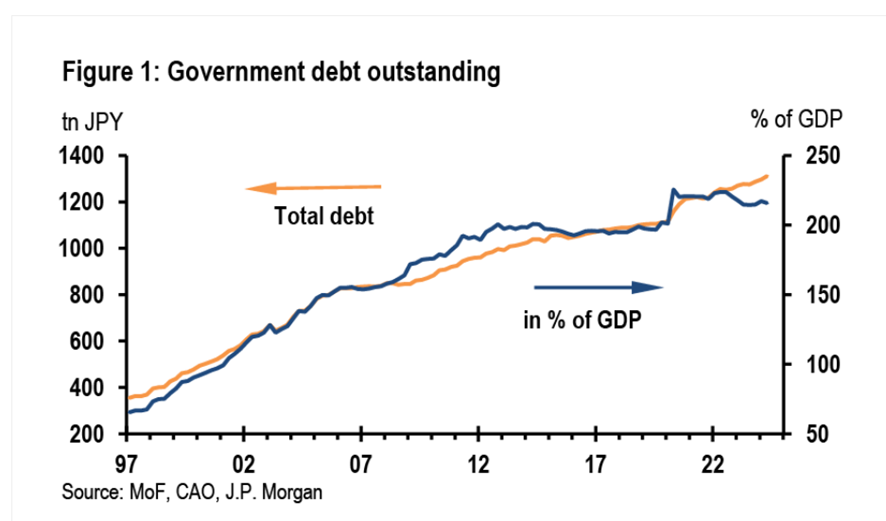

Japan is the perfect example of the failure of Keynesian policies.

More government spending only generates more debt and stagnation, and with years of printing, the yen's value has been obliterated.

Graphs JP Morgan and Bloomberg

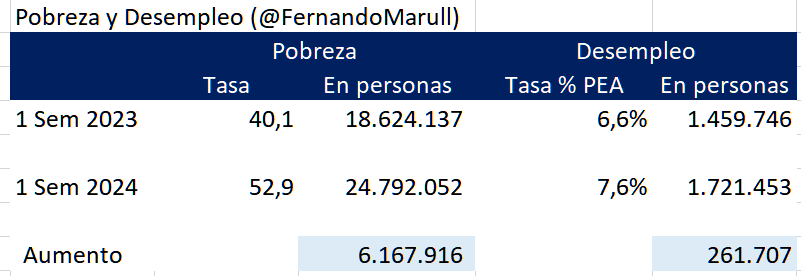

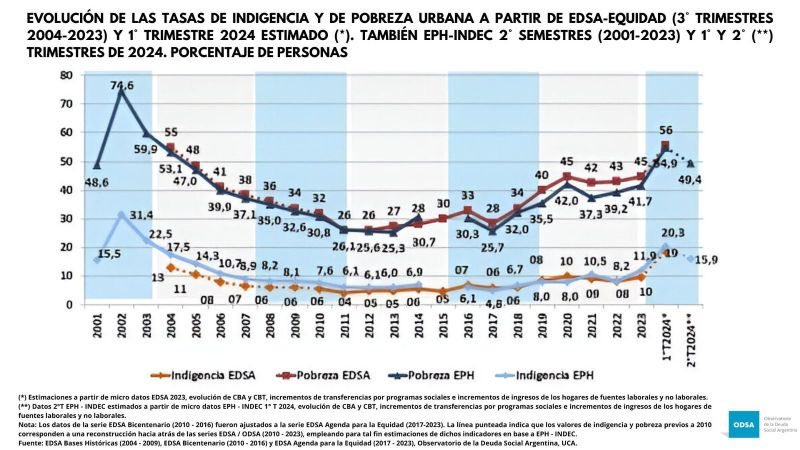

Argentina.

The socialist MMT crowd that has discovered poverty now never talked about the constant rise in impoverishment during the years of socialist government. Furthermore, they ignore that poverty started to decrease in the second quarter of 2024 when Milei's policies started to be in place.

https://t.co/jFpHY6EuJE

@JMilei

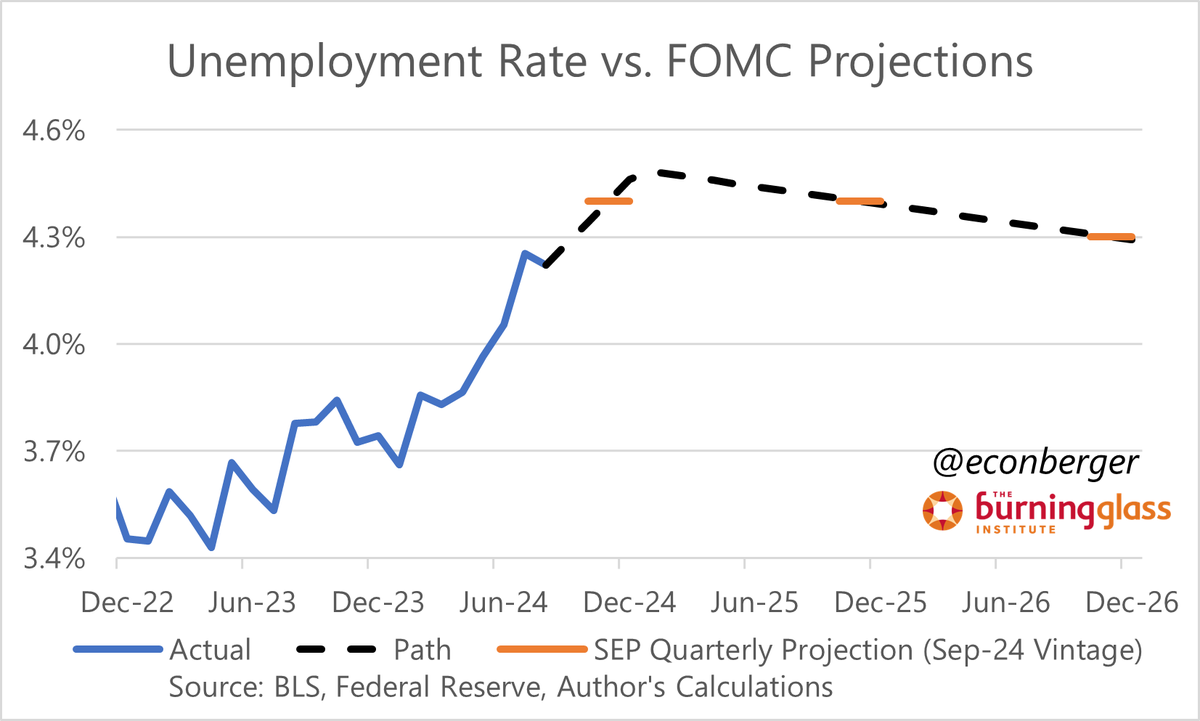

There's a "race" underway between monetary policy easing & ongoing labor market cooling dynamics.

Monetary policy will "win" in the end, but probably not before the US labor market experiences a little more pain.

The Fed told us their projected "splits", this chart tracks them.

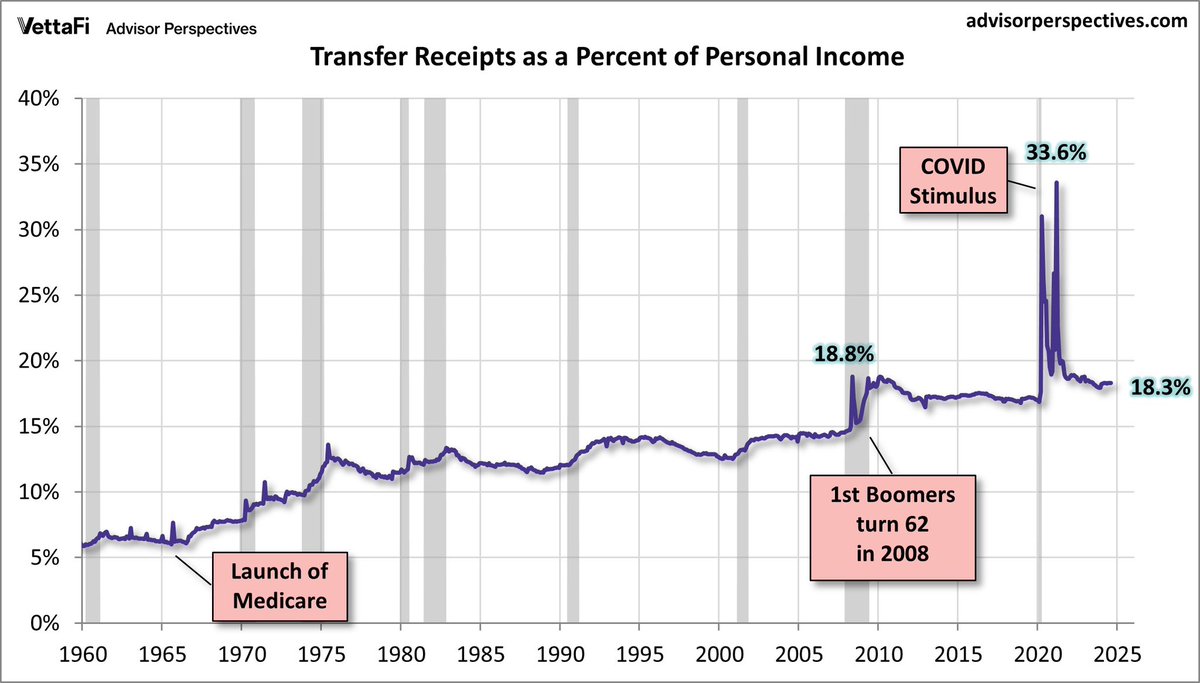

Transfer Receipts - These are benefits received for no direct services performed. They include Social Security, Medicare & Medicaid, Unemployment Assistance, etc.

If the economy is so strong, then why are Transfer Receipts still at the high levels seen during the GFC? 👇🏼

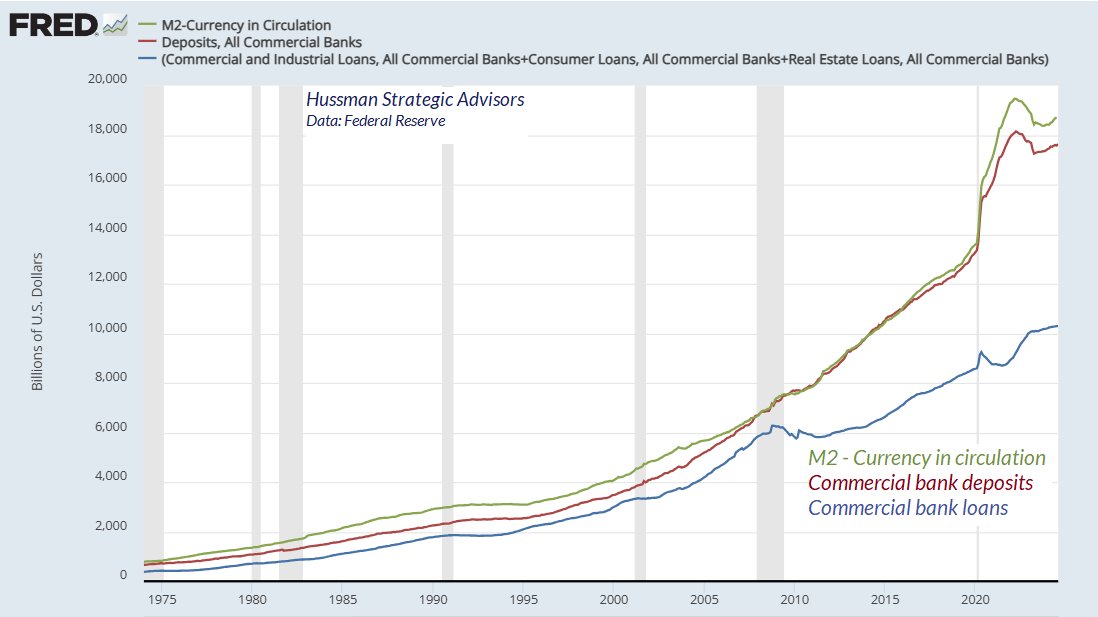

Be careful about interpreting M2 as if it means the same as it did before QE. Historically, "deposit creation" was virtually identical to "loan creation." Growth in M2 was a reflection of intermediation.

QE created a gap of excess reserves someone has to hold, now earning 4.9%.

The long-term quarterly chart suggests that oil may be establishing a historical support level after breaking through a major resistance in 2021.

This development is significant and could set the stage for oil prices to find a bottom, despite concerns about elections.

Moreover, investors are currently holding one of the lowest long positions in WTI contracts in the past decade.

This suggests that positioning is skewed, potentially paving the way for a notable reversal in the recent decline in energy prices.

Finally, the Fed’s recent decision to further ease monetary conditions, despite financial conditions already being at two-year lows, could intensify inflationary pressures in my view.

As a reminder:

It’s worth noting that oil prices and the breakeven rate are closely aligned, which is logical given that energy prices significantly influence inflation expectations over time.

Disclosure:

Crescat may or may not hold positions at any given time in the securities herein. This is not a recommendation or endorsement to buy or sell any security or other financial instrument. West Texas Intermediate (WTI - Cushing) represents a crude stream produced in Texas and southern Oklahoma which serves as a reference or "marker" for pricing a number of other crude streams and which is traded in the domestic spot market at Cushing, Oklahoma.

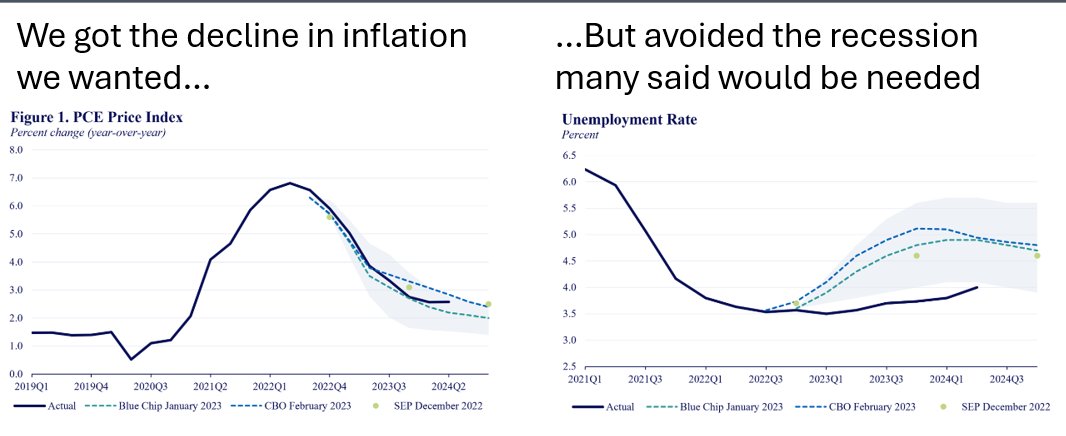

Real Median Household Income Increased in 2023 for First Time Since 2019

@adamtaggart@tyillc@mtmalinen@jimiuorio

Last week the Census Department released real median household income for 2023. Let’s investigate.

https://t.co/DjIPMSuSRg

🔥FED WILL CUT RATES ON WEDNESDAY FOR THE 1ST TIME IN 4.5 YEARS🔥

Stocks usually fall ~15% within 12 months following the 1st cut if there is a recession.

If no recession, stocks rise by >10%.

Key caveat is, that we will know if there was a recession a few months after the cut

From the Fed's perspective, Friday's fed fund futures close was about the worst possible: 49% probability of a 50 bps cut/51% probability of a 25 bps cut (chart). This is literally one tick from maximum uncertainty (50/50).

About half of Wall Street will be disappointed/surprised if this holds through Wednesday.

The Fed designed forward guidance (them what will happen before you do it) to prevent this exact scenario.

So, expect one of two things ...

1. A story that "clarifies" how much the Fed will cut on the 18th. Probably Monday morning.

2. No clarity will lead to a discussion that forward guidance is dead. Markets will have to adjust to a world of less Fed clarity by putting larger risk premiums and higher volatility into markets that discount what the Fed intends to do. This means the funding markets.

I expect #1. But if we get #2, I hope Powell addresses it directly in his presser on Wednesday.

Updated from monthly comment - Order surplus gauge still right at the threshold of prior recessions. Other leading measures near thresholds as well, but my view is we'd still need more deterioration in the data to expect a downturn with confidence.

More: https://t.co/l65KqpxY5R