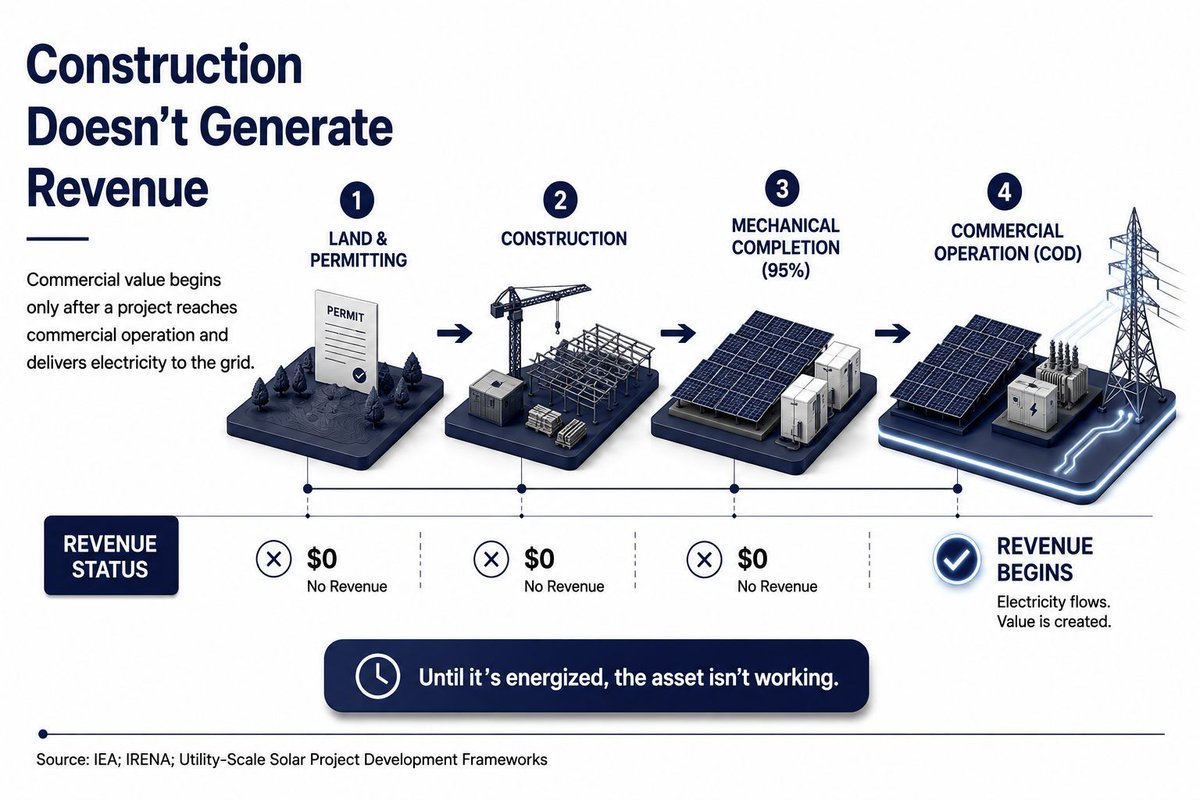

Everyone focuses on securing land, permits and financing for utility-scale solar. Commercial operation is often decided by execution. A project that's 95% complete generates the same revenue as one that's 50% complete. Until it's energized, the asset isn't working.

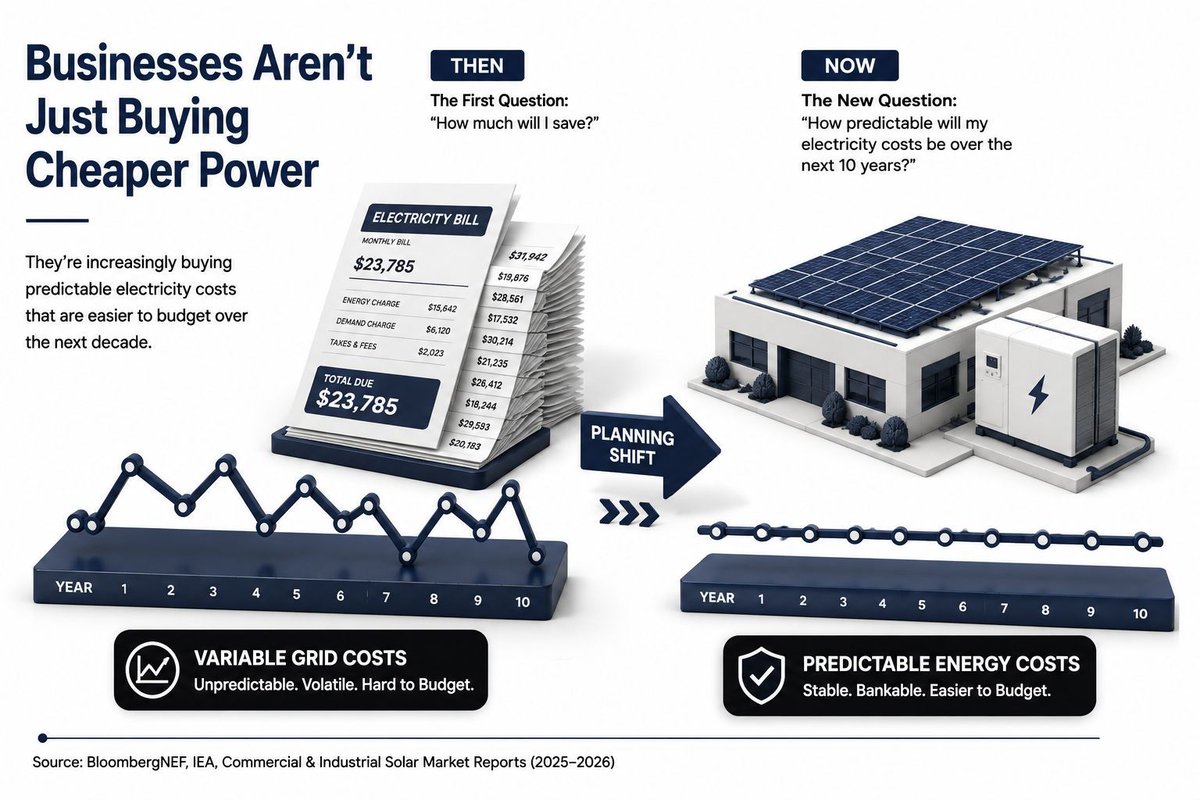

Interesting to see how commercial solar conversations have changed. A few years ago, the first question was, "How much will I save?" Now it's increasingly, "How predictable will my electricity costs be over the next 10 years?" Energy pricing is becoming part of financial planning

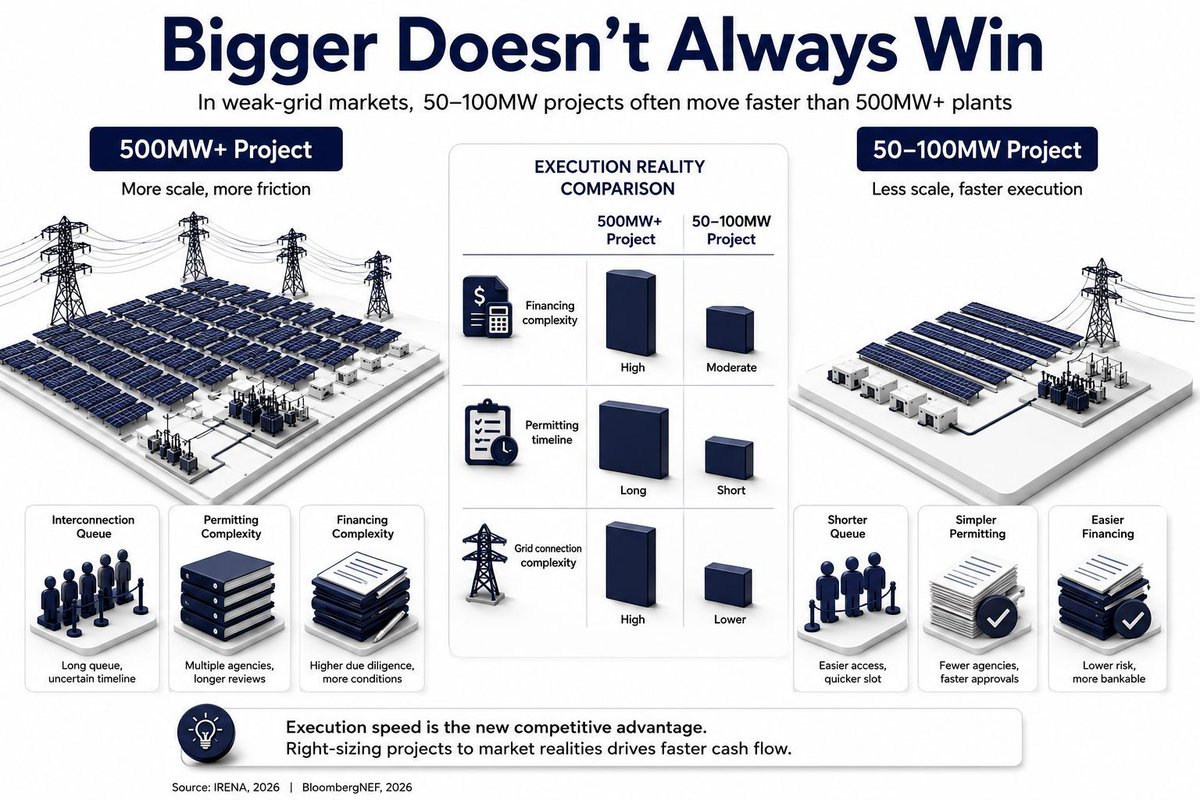

Everyone talks about building bigger solar farms. The harder question is whether bigger projects still deliver the best returns. In many markets, a 50–100MW project can reach commercial operation and generate revenue long before a 500MW project clears interconnection hurdles.

Battery storage costs have fallen by more than 90% since 2010, but the more interesting number is duration. Utilities are increasingly specifying 4–8 hour systems because the value is shifting from storing excess solar to covering the evening peak. Availability not just capacity.

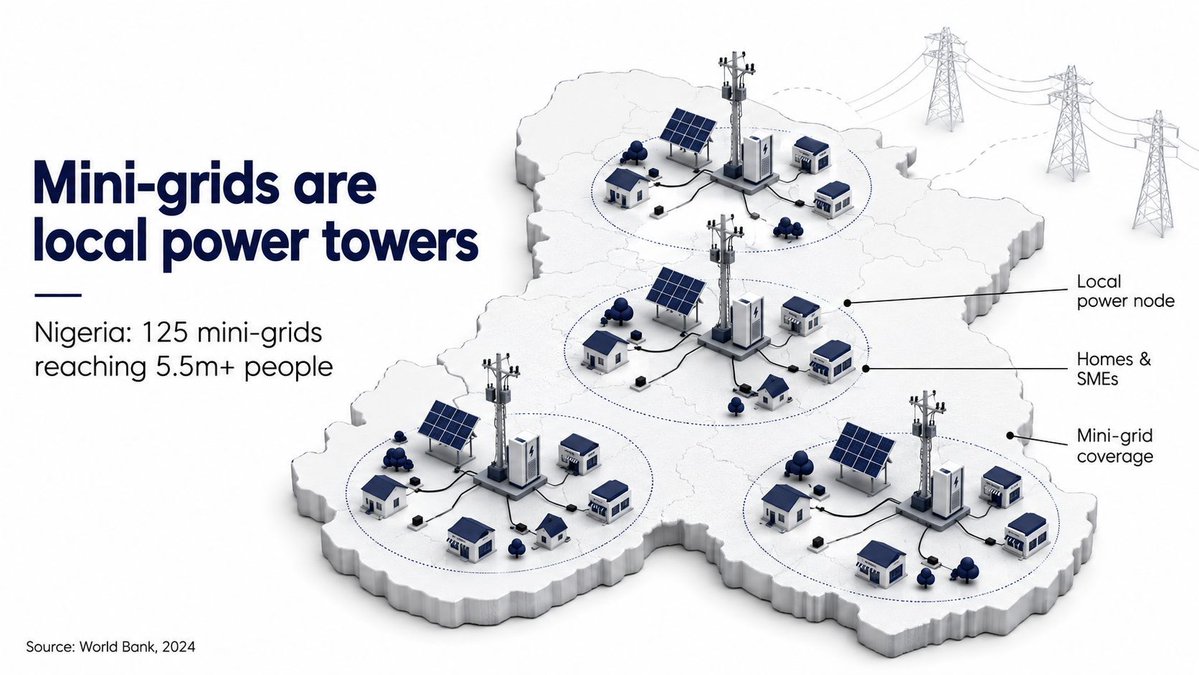

Mini-grids are starting to look like telecom towers for power. You don't wait for one national network to reach every village; you build local nodes where demand already exists. Nigeria's 125 mini-grids (as at 2024) reaching 5.5m+ people is the model getting harder to ignore.

It changes how developers sequence capital deployment and equipment ordering, even when project scale hasn’t changed much. The interesting part is how quietly this is reshaping what “bankable” actually looks like in the region.

West African renewable procurement has started to show a subtle shift in timing expectations. More tenders are being structured around staged delivery milestones rather than single COD dates, especially where FX exposure and offtaker credit risk sit high.

Interesting to see how storage tenders are evolving. It used to be enough to ask, “How many MWh can this battery store?” Now buyers are asking a different question: “How fast can it respond when the grid wobbles?” Inertia and ramp rate are quietly becoming bankable assets.

Going solar for a business is starting to look less like an eco-trend and more like an insurance policy against energy price spikes. Companies are locking in power costs for the next decade or more. Design for certainty, not just savings, changes how you build it.

Notice how many smaller solar projects are entering the pipeline lately? There’s a reason. Massive utility-scale projects look great on paper, but they break the local grid. Under 100MW is the cheat code for getting projects funded and connected.

In the energy world, bigger is no longer automatically better. While official government pipelines are still chasing mega-projects, developers are quietly building smaller power plants.

The countries winning the big energy investments aren't just building more power plants - they’re building smart, tough grids that won't collapse during peak periods and system disturbances.

Think of a country's power grid like a smartphone. You don't just want a bigger battery (more generation); you want software that doesn't crash when you open 10 apps at once (resilience).

The real battle today is the delivery infrastructure - can the grid actually wheel additional the power generated, and will developers get paid securely? That's where the smart money is looking.

The narrative around investing in African electricity infrastructure has completely flipped. It used to be: "More people = more power needed."

This is not the full picture as demand alone was never the bottleneck.

A few years ago, solar manufacturing was a scale game. Lowest cost won. Today, execution certainty matters more. Buyers increasingly care about supply chain resilience, traceability and warranty confidence, not just the cheapest module.

Renewable energy targets keep getting bigger on paper, which sounds great, but policy ambition alone doesn’t unlock capital. Investors are increasingly pricing regulatory consistency, payment security and FX convertibility ahead of headline capacity targets.

Cheaper solar modules should make commercial rooftop projects an easy yes, right? Not always. For many C&I projects, the real constraint now is roof suitability. Weak structural load capacity, aging roofs and retrofit costs are quietly killing deals before pricing even matters.

Bigger utility-scale projects are often assumed to deliver better economics because of scale. But in many emerging markets, 50–100MW projects are increasingly easier to finance, permit and energize than 500MW+ plants. Bigger isn’t always more bankable.