@thomaseisenhuth Absolut richtig. Leider sind diesbezüglich viele eher bildungsresistent. Dennoch bemerke ich im privaten österreichisch / deutschen Umfeld immer positivere Stimmung betreffend Atomenergie. Manchmal blicken wir doch über unseren Tellerrand!

⏰READ THIS

Galway Metals (TSXV: $GWM.v - OTC: $GAYMF)

DEEPDIVE INTO WHY I MADE IT MY SHORT TERM BIGGEST POSITION.

--------------------------------

Galway Metals controls two 100%-owned Canadian assets:

Clarence Stream (New Brunswick) - an open‑pitable #gold system with a 2022 NI 43‑101 resource of ~2.26 Moz Au (Indicated + Inferred) at ~2–2.6 g/t, plus antimony credits. Since that MRE, Galway has reported numerous strong intercepts (esp. at the Southwest/Stewart area and North Zone) that look additive to near‑surface ounces. I know because I have backtracked every single newsflow they have had since 2022 this week.

Estrades (Québec) - a past‑producing, gold‑rich polymetallic VMS deposit with a Dec 2024 resource update and substantially improved metallurgical recoveries (notably for gold).

The bonus that people are missing here is that Estrades is one of the highest-grade undeveloped silver-rich polymetallic VMS resources in Canada, grading roughly 500 g/t AgEq on average in the resource, with recent drill holes returning 1,000–1,500 g/t AgEq over multi-metre intercepts. (Upside potential is huge here)

Average resource grade: ~500 g/t AgEq (11 g/t AuEq).

Typical high-grade shoots: 800–1,400 g/t AgEq.

Historic production: 172 g/t Ag (silver-dominant).

You cant find many better #Silver bonuses than this.

While the company’s focus remains Clarence Stream (FLAGSHIP), Estrades adds optionality and potential for a small, high‑margin restart scenario if studies are positive. I bet they will, as they stopped producing many many years ago for the simple reason that metalprices back than wasn't attractive enough, guess what, now they are.

Why it’s interesting now:

(i) active drilling at Clarence Stream with clear step‑out success along a 65‑km trend;

(ii) company guidance to start an updated Clarence Stream MRE in early 2026;

(iii) a clean cap table (no debt), meaningful insider ownership, and consistent insider buying over 2023–2025; and

(iv) ~$8M cash mid‑2025 to keep the drills turning.

------------------------------------------

Galway stands out as a district-scale Canadian gold growth story with a credible path to well above 3 Moz at Clarence Stream, supported by consistent drilling success, strong insider alignment, and a valuable secondary asset in the high-grade Estrades polymetallic project.

Near-term catalysts include continued step-out intercepts, the launch of the 2026 updated MRE, and the initiation of the first PEA on Clarence Stream, which is expected to outline a robust open-pit operation with meaningful antimony by-product credits.

If the upcoming MRE successfully captures even a fraction of the post-2022 drilling - potentially adding several hundred thousand new ounces or even millions - the company could see a significant valuation re-rating, especially when paired with improved metallurgical recoveries and the parallel Estrades scoping study.

Note: Backtracking their newsflow since 2022, it's highly likely the updated MRE will add the word "million" ounces in the update, hence a huge oppertunity for us here.

Since the 2022 MRE, Galway’s continuous drilling at Clarence Stream has consistently delivered higher gold grades, broader intercepts, and deeper extensions, confirming strong continuity and growth potential. The Southwest–Stewart corridor has expanded significantly with multiple high-grade hits and wider zones than modeled in the last MRE, while the North Zone also continues to thicken at depth. Importantly, mineralization at Clarence Stream remains open in all directions - along strike, down dip, and between deposits - supporting the potential for a much larger resource footprint in the upcoming 2026 update.

Since 2022, Galway has repeatedly delivered

(i) thicker mineralized intervals in the SW/Stewart area and

(ii) higher‑grade shoots both there and at the North Zone.

These trends typically translate into pit‑additive ounces and selective underground growth once drill density supports wireframing. The company’s own slides now frame the SW deposit as >650 m longer to the north (Stewart) and highlight pit‑connectivity potential.

On a simple EV/oz basis, Galway trades at a deep discount to Québec peers and even to other developers in Canada. A large part of the gap is stage (no PEA yet), but the discount appears wider than stage alone would justify if Clarence Stream can demonstrate robust economics.

PS: The PEA is expected around the corner..

Galway Metals is currently trading at about US$21 per ounce of gold in the ground (EV/oz ≈ $21 / oz Au).

-------------------------------------

Capital Structure, Liquidity & Ownership (mid‑2025)

Shares outstanding: ~108M

Options: ~4.9M

Warrants: ~10.0M (bulk issued in 2024 financings; two‑year half‑warrants mostly at $0.60–$0.70 strike)

Debt: $0

Cash: ~$8.2M (mid‑June 2025)

Mgmt/Insiders/Family ownership: ~20%

Notable holders: Extract Exploration Fund, VanEck, CDPQ, Schroders, Canada Life, Mackenzie, plus CEO Robert Hinchcliffe.

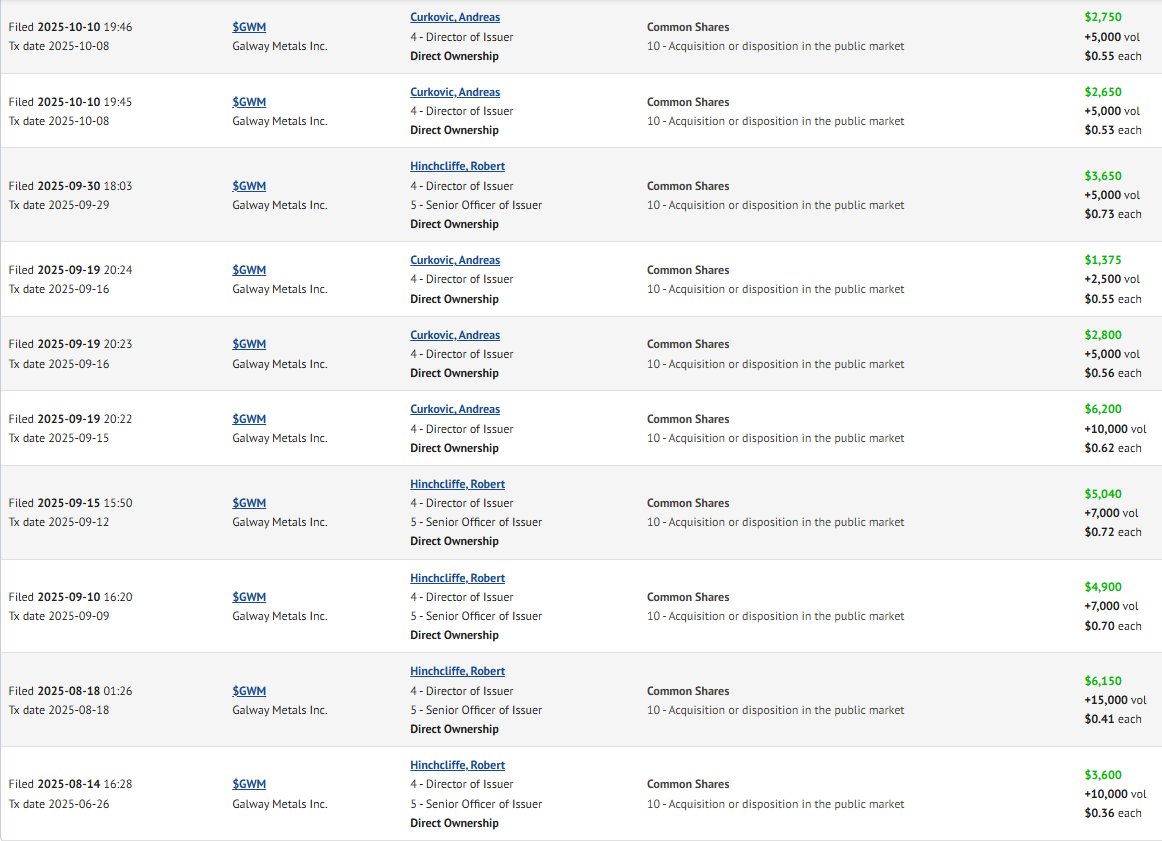

Insider buying: The CEO has been a persistent open‑market buyer in 2023–2025 (multi‑million shares cumulatively). This is an unusually strong alignment signal for a junior. Fact is, the whole board is buying basically every month during 2025 almost.

----------------------------------------

EV/oz Re-Rate Math - What a 3–5 Moz updated MRE could mean(now we talking only Clarence Stream here):

Today (2.26 Moz, EV ≈ US$47M): ~US$21/oz.

At 3.0 Moz (same EV): ~US$16/oz. If the market begins valuing Galway at even US$40–60/oz (still below Québec peers), the equity could 2–3× from here.

At 4.0 Moz: ~US$12/oz at current EV; at a US$50/oz peer multiple, implied EV ~US$200M+.

At 5.0 Moz: ~US$9–10/oz at current EV; at US$50–80/oz (typical PEA-stage range), implied EV US$250–400M.

Here is our opportunity:

If Galway can prove a 3+ Moz resource and deliver a strong PEA, the stock could re-rate sharply toward peer valuation levels even before full feasibility. And tracking their assay newsflow since 2022, im confident that will be the case. Now add current metal prices. We have the PERFECT STORM OPPORTUNITY TO MAKE EASY MONEY HERE IS MY BELIEF.

-------------------------------------

So.... The PEA currently underway is for Estrades, led by BBA Engineering, and is expected for completion in Q4 2025. Early work already indicates a meaningful economic uplift driven by major metallurgical improvements:

Gold recovery: 86.6% (↑31%)

Silver recovery: ~45% (↑9%)

Copper recovery: ~95%, with clean concentrates

Zinc and lead recoveries also improved

These upgrades significantly strengthen Estrades’ economics and support the case for a small, high-margin restart. The Dec 2024 resource update already showed a 17% increase in Indicated tonnage and 22% in Inferred, even before new drilling results.

Exploration upside remains massive - Estrades covers 31 km along the Casa Berardi Fault and 17 km on the Newiska Horizon, both highly prospective for further gold and VMS discoveries. Areas like Newiska West and Copper East are still largely untested and could add substantial new tonnage. 👀👀

Meanwhile, at Clarence Stream, the company plans to start its updated MRE in Q1 2026, which will incorporate over three years of high-grade drilling results. This is two massive triggers that can valueshoot this stock enormously!

-----------------------------------------

Now to my favorite part of this setup:

The stock has recently been a victim of one single aggressive seller, who has been unloading shares non-stop over the past 2–3 weeks, keeping a lid on the breakout and pushing the price down from $0.78 to $0.55.

The good news? That kind of persistent selling pressure doesn’t last forever - and judging by the huge volume and strong accumulation seen this past week, it looks like the market has finally absorbed his entire position. (Just look at the volume spikes.)

Since no insider selling above 9.9% ownership has been flagged, this seller likely held below the insider threshold, meaning the recent trading volume has probably cleared him out completely.

With a +11.48% close yesterday and around +10% thursday despite weak sentiment across the mining sector, it looks like we smashed that actor and from here I believe it’s go time for this stock. It's like @AllStreetsWolf usually says "volume precedes price". Fact is, this week was the strongest weekly volume EVER in the companies history. That says something 😉Maybe it says that @RockBtmEntries is rich as I believe he also was loading up this week ? 👀

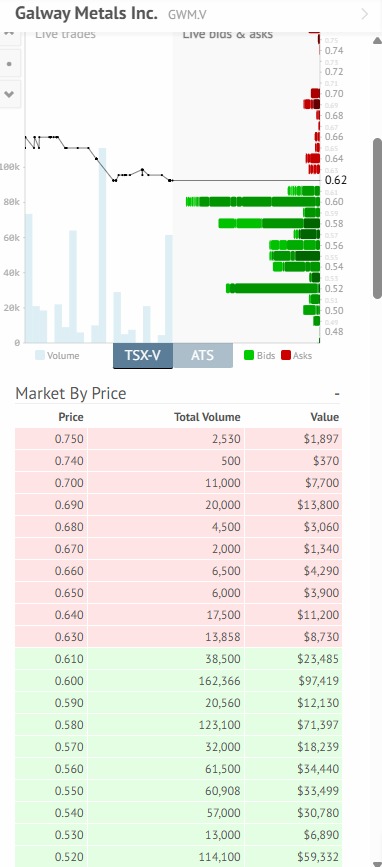

- Now also add that the orderbook is looking extremly strong, actually the best book right now of all the stocks im tracking for intermediate big upside potential. You guys know by now I use orderbooks alot in my decision making... I know my books. (See picture #2 of this post for how the orderbook looked yday before it closed at $0.68...

There is alot of firepower that want in here, and that has been just standing and fishing shares from this anon seller at these low levels, with him gone now (most likely) there is a big chance this firepower just have to chase price higher and higher from here. Because with the upcoming updated MRE and PEA, smart money knows a re-rate is incoming for this stock. This should be a 3-5x play coming 6months. Yes im dead serious, I expect 300-500%+ here.

So to summarize:

-We have the perfect storm forming with the most value-creating news catalysts in the company’s history coming up (MRE + PEA).

-We just had the highest weekly trading volume ever recorded for the company.

-The anonymous seller who’s been holding the stock down has now been mostly, if not fully, cleared out - like a balloon finally released from underwater.

-We’re in a rising metals environment, especially for #Gold and #Silver.

-The orderbook looks extremely strong, showing limited downside and huge upside potential. 🚀

-And to top it off, the chart looks absolutely explosive right now.

-Oh yes, there is NON STOP insider buying here month after month, (see pic nr #3 as an example).

I rest my case.

This, in my opinion, is one of the best near-term setup (3–6 months) in the sector - and what I stated above is exactly why I made it my largest short-term position in the portfolio.

LFG #GAYMF (if you know you know)

As always, this is no financial advice, always DYODD. Im simple showcasing why im loading up here.

Remember to retweet to get the case on the map, this is a gift to anyone reading it.

Cheers,

Ape