TokenInsight is the most trusted institution for professional crypto ratings and research. Delivering crypto data & market intelligence to crypto participants.

Today’s U.S. equity selloff, led by memory, semiconductors, and the broader AI supply chain, partly validated the framework we discussed in this article earlier.

The market is starting to reprice the AI capex cycle: suppliers have enjoyed strong near-term revenue, while investors are becoming more sensitive to future free cash flow, ROIC, and valuation discipline.

When crowded AI-linked trades start to unwind, the move can quickly shift from a fundamental reset to a positioning-driven deleveraging risk.

OUSD's current threat was never to displace the network; it is to hand distribution channels a bargaining anchor and thereby compress Circle's retained margin. Starting from the 10-Q, Circle's business model can be distilled into a single chain:

USDC in circulation × reserve yield = reserve income; distribution costs are then deducted, and what remains is Circle's retained profit.

The central question is this: under a trend of rising distribution-partner leverage, will the portion Circle keeps of every dollar of reserve income be systematically compressed? Consider Circle's revenue structure as a public company: reserve income was still 94% of total revenue in Q1, and retained profit only materializes after distribution costs are deducted. OUSD's yield-sharing model is, in essence, the institutionalization of an already-underway trend — rising distribution-partner leverage.

We’ve had lots of questions from our investor community looking for thoughts on OUSD, and so I thought I’d share my direct views here for anyone.

Stablecoin networks are platform and network effect businesses that are established over a long period of time, tend towards winner-take-most market structures, and resemble other internet platform utility markets. There are several layers that drive this.

First, stablecoin networks effectively act as public protocols and software layers on the internet and their network strength is a matter of the number and range of applications and services that integrate to the network. Every time a developer or service provider integrates to the network, it brings more network effects. This attracts more developers and adds more utility and more network effects. This then drives demand for the digital currency itself, which then reinforces these network effects through liquidity network effects.

We have realized this at a massive scale with the USDC network today — thousands upon thousands of services integrate with our network, which in turn provides immense utility not just to each application, but to users as a whole who benefit massively from the reach and interoperability that exists. This drives user and developer preference further. We’ve invested in building that ecosystem over nearly a decade, and now it’s accelerating as mainstream institutions come onto the network, connecting their customers and users.

We add to that utility by building software stacks that further expand and strengthen the network — protocols like CCTP and Gateway, which promote interoperability, safety and liquidity around the world. This expands the target surface area for app builders and developers, making it easy for them to tap into the liquidity and network effects that already exist. We are now seeing that stack get pulled into all kinds of chains, permissioned L2s, networks being built by governments, and so much more.

The second layer is that of liquidity network effects. This is fundamental. Liquidity begets liquidity. For a stablecoin to achieve scale and utility, it needs to be highly liquid, both on a primary basis (e.g., through all the major financial market centers in the world, with world class direct banking liquidity) and on a secondary basis both by being available and tradeable for retail and institutional clients in every geography and against every fiat instrument in the world. People who want to access and move value need to be able to easily get in and out of that digital currency. Here, we’ve invested nearly a decade in building out that liquidity, and it is now entrenched in exchanges, DeFI venues, and with PSPs, payments firms, regional exchanges, and so many others. Establishing these liquidity network effects also involves building global regulatory infrastructure and ensuring that the stablecoin is available under various regimes around the world. Today, USDC is in the top 3 most liquid digital assets in the world, and it falls off sharply after that. BTC, USDT and USDC have extraordinary liquidity. The closest other dollar stables are like 10x smaller and that liquidity tends to be concentrated in promotional books in a single exchange, whereas USDC liquidity is dispersed widely across dozens and dozens of surfaces. Building this liquidity has been a nearly decade-long task that we continue.

A third layer of network strength comes from the deep integration with the policy and regulatory environment — in many cases, years of effort to build licensing (e.g., USDC is the only large global stablecoin currently available in all of Europe or Japan), and more regimes for stablecoins are coming online, with Circle leading the way in ensuring that USDC is officially recognized, registered, licensed and accepted in the most important markets in the world. On the back of this is the work of building global banking, reserve management and treasury and liquidity management that can operate this on a nearly 24/7 basis in markets and banking systems globally. This globalization effort is a massive investment that we have made over the years.

All of these investments by Circle and our global ecosystem of thousands of partners have delivered the net result of providing the world’s most trusted and available digital dollar infrastructure—a utility that any user, developer, or business can freely and easily tap into. And we do not intend to slow down.

All of this compounds and shows in the numbers. In Q1 2026, according to third-party analysts (Artemis) who track stablecoin adoption, USDC handled nearly $30T in onchain transactions, representing 80% of all dollar stablecoin transactions on blockchains. USDT handled the remaining 20% of transactions. All of the combined remaining dollar stablecoins handled a total of 0% of transactions (i.e., < 0.5%). While other stablecoins may have some circulation, most of that is through promotions and incentives, the actual usage is extremely limited—because of the extremely limited liquidity and network utility that exists for these coins.

But my thoughts on the competitive landscape are not just about the strength of our network—there are also considerations around any new initiative.

Several perspectives and positioning have been shared about how something like OUSD improves on something like USDC.

1) Free mint and burn. The argument suggests that existing stablecoins charge burn fees, and payments firms should not need to pay these (despite the fact that the entire payment industry is built on small bps fees on various ingress and egress points on their networks). There are structural market realities built around the fact that some stablecoins impose very large redemption fees and have limited redemption facilities – the impact of this is that stablecoins with strong redemption facilities, good liquidity and no fees become the offramp for their competitor stablecoins. It may seem easy to say one will offer unlimited and free redeems, however market reality likely forces other behavior. This can be addressed – and is addressed by Circle – through contractual mechanisms vs. a blanket fee exemption.

2) Everybody wins and shares. While this sounds good in principle, the reality of the market and market opportunity is quite different. Today, Circle shares the majority of its income with its distribution partners, and we continue to lean hard into expanding those partnerships with leading companies across every sector of the market. However, we also retain significant income that allows us to invest in the massive market infrastructure that makes this such a powerful and valuable utility for the world to build on. Giving away all the income is a recipe for starving an infrastructure, systematically underinvesting and ensuring that your platform will remain limited in scope.

Furthermore, Circle believes that the future stablecoin market is likely several orders of magnitude larger than it is today. We’re actively bringing partners into the USDC ecosystem through a diverse and growing set of partnership models that span our work with exchanges, custodians, payments firms, asset issuers and more. We are excited to continue to build with a “big tent mentality” where the entire ecosystem can grow value together.

3) A consortium where everybody has a voice. Perhaps I have a cynical view, but the track record of consortium products achieving scale, P/M Fit or even basic product agility is absolutely dismal, and while there are examples of financial consortia that operate utilities, they are predictably slow moving. Large groups of large companies coordinate poorly, have misaligned incentives, slow things down and rarely create the space for real durable innovation and competitiveness. They also typically, out of their own self-interest, starve the consortium itself on an operating basis. We actually tried this in the early days of USDC, and even with a very small group, ran into endless challenges and complexity. Smaller, tighter strategic collaborations and commercial partnership arrangements with product and platform builders that can drive forward independently will almost always outcompete large consortiums. But oftentimes when these get formed, everyone feels like they should put their logo on the list, kiss the ring, and make noise about openness. But typically those same firms will turn to their operating units and make the best decisions for their customers, which often means partnering with the market leader and building durable win-win partnerships.

There’s also been a bunch of commentary on Circle's partnership with Coinbase and what this all means. Our stablecoin partnership with Coinbase remains as strong as ever, and I think we both see that enormous opportunity ahead to expand the USDC network.

A final comment: Circle remains committed to supporting a wide range of different products and infrastructures, even when we might compete with different aspects of those partners’ products in other areas of our business. With OUSD, we work closely with many of the founding members, and we expect that those same members will remain large USDC partners and customers. At the same time, as Circle has diversified our product and platform stack, expanding across Arc, CCTP, CPN, StableFX, Agent Stack and many other areas, we continue to expand the partnerships and collaboration with many other stablecoin issuers — dozens of them — to help them launch on Arc, leverage our interoperability infrastructure, get supported in our Wallets and become settlement and FX options on CPN and StableFX.

We are huge believers in growth in the stablecoin ecosystem and welcome OUSD as a new member of the community!

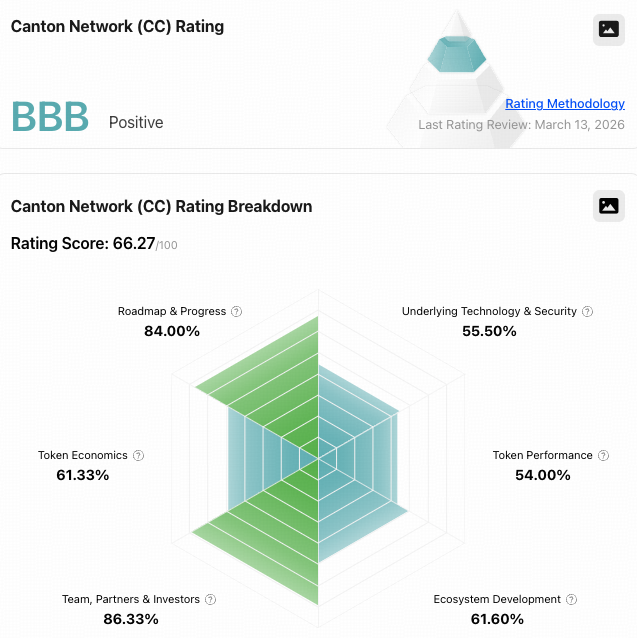

#TokenInsight Rating Monthly Review: Jun 2026

In June, we released and updated new ratings for 4 projects, including DeFi, Layer-2 and confidential computing network. The details are as follows:

@ethena ethereum:0x57e114b691db790c35207b2e685d4a43181e6061 - BBB Stable

@Optimism optimism:native - BBB Stable

@Arcium solana:ARXwZkNAtzPfdcoqQiduJn8EPv9fKiDfGn2KyggyDrFs - BBB Stable

@quantnetwork ethereum:0x4a220e6096b25eadb88358cb44068a3248254675 - BB Stable

More details 👇https://t.co/nzdGKVyUp3

#rating

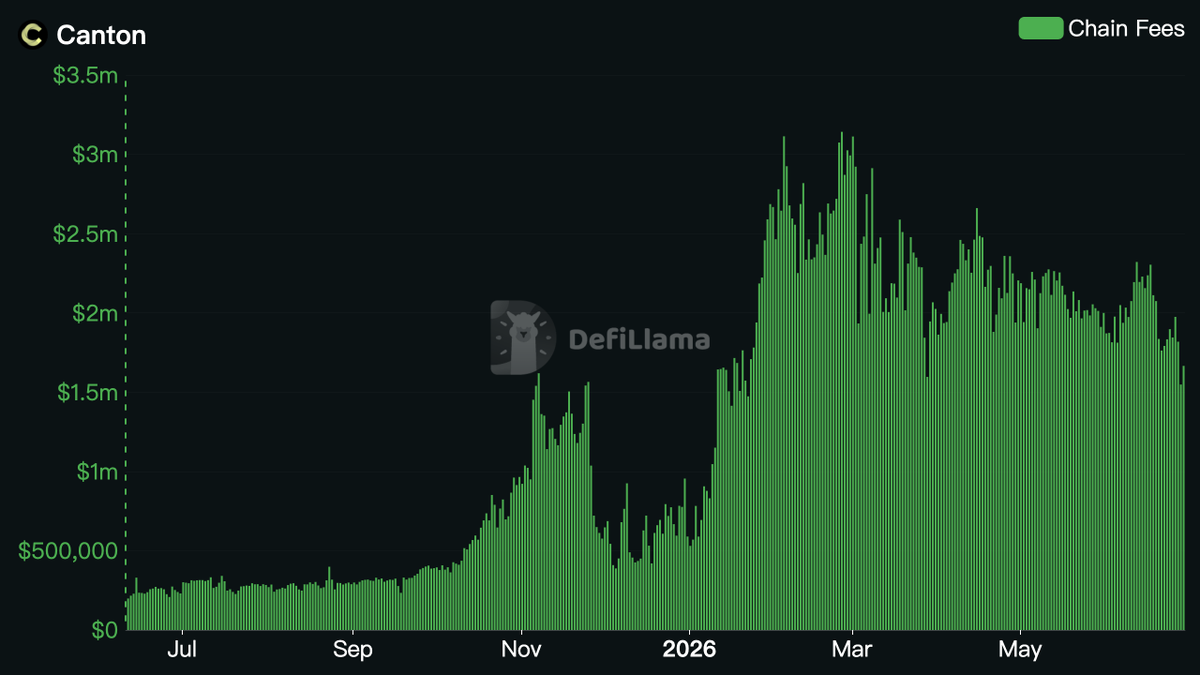

Canton Network’s (@CantonNetwork ) on-chain revenue is one of the most interesting parts of the canton-network:native thesis.

According to @DefiLlama, Canton is currently generating roughly $1.7M+ in daily fees, with around $57M in fees over the past 30 days.

That is a meaningful number for a Layer 1, especially one positioned around institutional finance, privacy-preserving settlement, and real-world assets.

But there is an important nuance.

Canton’s fees are not just protocol revenue in the traditional sense. The fees paid in canton-network:native are burned. This means network usage creates direct buy-and-burn pressure on canton-network:native.

In simple terms:

More usage → more fees → more canton-network:native burned.

That is the attractive side of the model.

However, the other side of the equation is token issuance.

DefiLlama also shows that Canton’s token incentives remain high. In recent data, daily token incentives have been higher than daily fees. So while the burn mechanism is real and meaningful, the network may not yet be in a net deflationary state.

That burn-versus-mint balance is the core of Canton Coin’s economics.

At current levels, Canton already has strong fee generation compared with most RWA-themed crypto networks. But for canton-network:native to justify a much stronger valuation, investors need to see sustained growth in daily fees, improving burn/mint dynamics, and broader usage of the Global Synchronizer by real institutional applications.

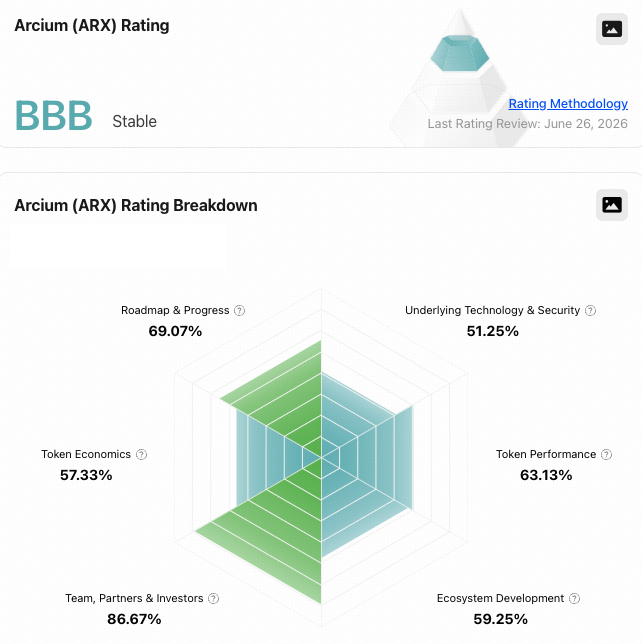

TokenInsight officially releases the rating for solana:ARXwZkNAtzPfdcoqQiduJn8EPv9fKiDfGn2KyggyDrFs !

Arcium (@Arcium) is a confidential computing network for Solana that enables private, verifiable computation using MPC, with computation coordinated on Solana and executed by decentralized Arx node operators.

Rating: BBB

Outlook: Stable

See more details on the token page 👉

https://t.co/VkqsI410Xa

June 23: @Ripple secured a preliminary CASP "Green Light" from Luxembourg's CSSF — eight days before MiCA's hard July 1 deadline. Combined with its existing EMI, Ripple can now offer collect/exchange/pay-out across all 30 EEA countries through one integration. RLUSD gets a real EU runway.

By mid-June, major EU-facing exchanges had already restricted or delisted USDT and other non-MiCA compliant stablecoins for EEA users.

EU has used MiCA to do what no US law has — partition the stablecoin universe by regulatory posture. Tether's dominance was always partly an artifact of who didn't have to choose. Now compliant issuers (Circle, Ripple, EU-licensed entrants) inherit a structurally bigger share of every euro-denominated flow.

Rates were held at 3.50–3.75%, largely in line with market expectations. The damage was the dot plot: median year-end rate jumped to 3.8% from 3.4% in March. Cuts didn't get pushed out — they got erased, and a hike is now on the table.

For a market that had spent six months trading off a "pivot is coming" thesis, this is a regime change, not a wobble. Liquidity-sensitive assets (BTC, ETH, long-duration alt L1s) rerate first; we got it within minutes — $2T wiped across equities, metals and crypto.

Powell-era forward guidance was about smoothing. Warsh's first meaningful signal is about credibility — the Fed is willing to look stubborn on inflation to anchor expectations. That's a higher real-rate path. Real rates are crypto's gravity. Until 5y TIPS roll over, every rally is supply, not demand.

In ~3 weeks @The_DTCC begins limited production trades of tokenized Russell 1000 equities, major ETFs, and US Treasuries on-chain. 50+ firms in the pilot: BlackRock, Goldman, JPMorgan, Circle, Ondo, Ripple Prime. Full service launch October 2026.

This is the plumbing of equity markets quietly forking onto blockchain settlement while the retail conversation argues about memecoins. The institutions building this pipe — BlackRock with BUIDL, JPM with OnChain Liquidity-Token MMF — are the ones to follow. The RWA TAM is one of the most under-priced narrative in the sector.

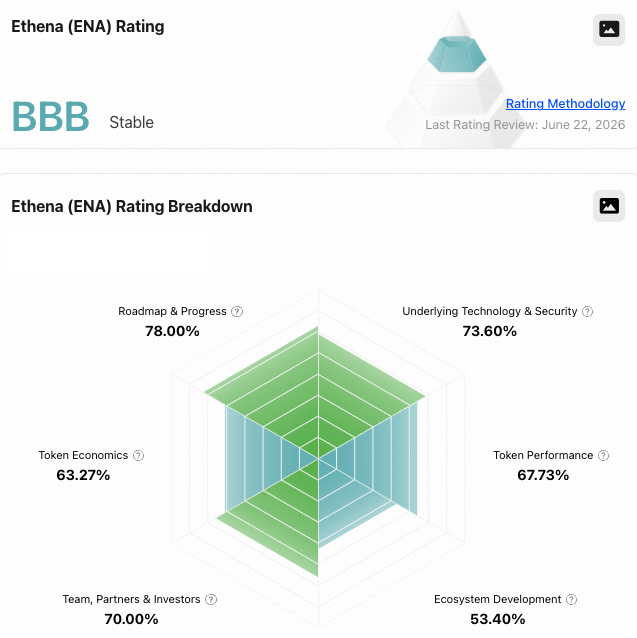

TokenInsight officially updates the rating for

ethereum:0x57e114b691db790c35207b2e685d4a43181e6061 !

Ethena (@ethena) is a synthetic dollar protocol built on Ethereum that provides a crypto-native solution for money not reliant on traditional banking system infrastructure, alongside a globally accessible dollar-denominated rewards instrument known as the “Internet Bond.”

Rating: BBB

Outlook: Stable

See more details on the token page https://t.co/9mKNAfvDf9

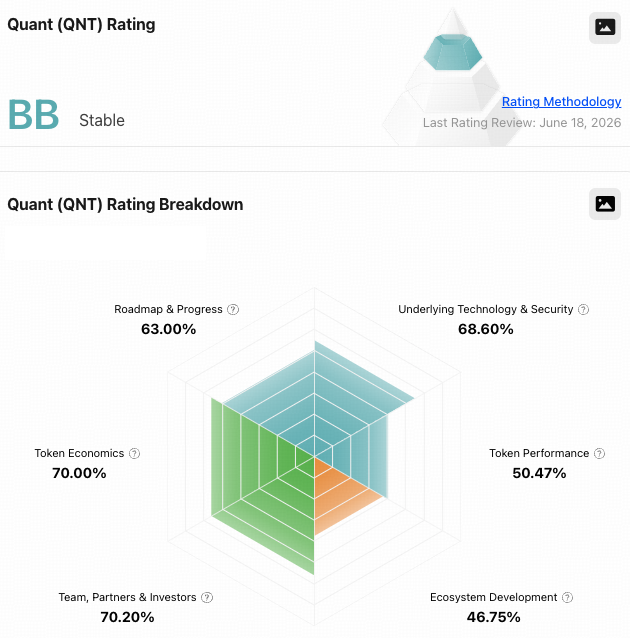

TokenInsight officially updates the rating for ethereum:0x4a220e6096b25eadb88358cb44068a3248254675 !

Quant (QNT) is an Ethereum-based project that aims to deliver enterprise-grade interoperability through Overledger — its blockchain operating system — for the secure exchange of information and digital assets across any network, platform or protocol, at scale.

Rating: BB

Outlook: Stable

See more details on the token page👇

https://t.co/3GvNSn4pct

Stripe, Visa, Mastercard and potentially Coinbase were involved in a new stablecoin payments platform. The market initially framed this as a broad threat to both solana:Es9vMFrzaCERmJfrF4H2FYD4KCoNkY11McCe8BenwNYB and base:0x833589fcd6edb6e08f4c7c32d4f71b54bda02913 , but the impact is likely asymmetric.

This would be a more direct threat to @circle than to @tether. Tether’s core moat is offshore dollar liquidity, exchange and OTC distribution, and emerging-market remittance flows across Asia and LatAm. Those are not the main domains where Visa and Mastercard compete.

Circle’s exposure is different. USDC’s growth story is tied to regulated payments, merchant settlement and on-chain commerce, exactly the areas a payments-led stablecoin platform would target. If Coinbase and major payment networks eventually support or issue their own stablecoin, Circle’s distribution power could weaken.

The key risk is not an collapse in USDC supply, but margin pressure. Circle earns heavily from reserve income, so analyst should watch average USDC circulation, reserve yield, distribution costs and USDC’s retention in merchant payment flows.

Coinbase launched SpaceX perpetual futures shortly before $SPCX public listing. Binance and OKX have similar products live or in flight on SpaceX, OpenAI, and Anthropic.

What's actually happening: exchanges have noticed that retail demand to express views on private megacaps far exceeds the supply of legal pathways to do so (which is essentially zero outside accredited secondary markets). Perpetual futures reframe the exposure as a derivatives product with no deliverable underlying solve the legal problem and create a synthetic market.