Two products, one mission.

The Cube — our live, curated tokenization newsroom

The Office — the infinite-canvas intelligence workspace.

Read the market, then run it, from one place.

#RWA#Tokenization

@Blast adds native yield — yield baked into the L2 itself, a natural fit for tokenized treasuries and RWAs where yield-bearing assets are the whole point. Should the chain itself pay you yield?

Tokenized assets aren't just digital — they're programmable. A tokenized bond pays its coupon automatically. Tokenized property splits rent to holders instantly. Dividends distribute themselves. No transfer agent, no delay. What would you automate first?

Common question: 'if it's just a token, what backs it?' Answer: a regulated custodian holds the real asset off-chain, a smart contract verifies their holdings, and your token is a verified claim you can redeem anytime. Trust comes from the bridge between both worlds. Clearer now?

This is the clearest articulation yet of where the entire RWA thesis is heading. The mission has never wavered — you’ve just been methodically climbing the value stack exactly as Nate always mapped it out. From tokenized securities → prime brokerage & onchain derivatives → sophisticated asset management → and now the agentic & fully composable layer.

That progression isn’t incremental; it’s the only way to actually onboard the $160T+ liquid asset universe at scale.

Seeing RWA perpetuals, tokenized equity options, cross-asset automated rebalancing, and AI-native robo-advisory all living natively onchain in one cohesive system is genuinely next-level.

The fact that <0.01% of global liquid assets are onchain yet is the ultimate proof we’re still in the very first inning. This isn’t just product expansion — it’s infrastructure for the next era of capital markets. 🚀@OndoFinance

In legacy finance, who owns what lives in private databases you can't see or audit. Tokenized assets record ownership on a public ledger — provable, transparent, instant to verify. A whole category of settlement fraud just... disappears. Underrated benefit?

Tokenization's real superpower isn't speed — it's division. A $1M building becomes 1,000 tokens of $1,000 each. Markets that required institutional checks now open to anyone with $1,000. Which 'institutions-only' market would YOU finally enter?

The most underrated tokenization superpower: composability. Tokenized assets share open standards, so they snap together like legos. A tokenized treasury collateralizes a loan that funds tokenized property — all atomic, all on-chain. Legacy rails can't do this. What gets built?

Strong thesis @wasnevermarried 🔥 $INJ has been building serious institutional-grade infrastructure — CFTC-regulated futures, the Policy Institute, and those staked INJ ETF filings are exactly the kind of moves that bring real capital. Hyperliquid ($HYPE) is crushing it on perps volume right now, but Injective’s positioning in the broader onchain finance stack gives it a different kind of upside. The real alpha? **Tokenization + high-performance L1s like Injective** = the perfect rails for RWAs. When treasuries, credit, commodities, and real estate settle instantly onchain with proper regulatory wrappers, the chains that can handle both DeFi-native volume *and* institutional flows win. Injective is clearly gunning for that seat at the table. We’re watching both closely at **@tokenxonchain** — building the tokenized asset infrastructure layer that makes these ecosystems even more powerful. 26x for $INJ to match HYPE’s current MC? Ambitious… but in this cycle, nothing feels impossible when the product-market fit is this strong. What’s your target for INJ if the institutional narrative keeps playing out?

Agreed @diegoxyz— tokenization is the fastest horse in crypto right now, and the numbers only keep getting crazier. $31B+ TVL with 240%+ YoY growth and 830k+ holders is just the beginning. The real explosion comes as more real-world assets (especially treasuries, private credit, and commodities) move fully onchain with instant settlement, fractional ownership, and global access 24/7.

Illiquid assets trade at a discount — that's the 'illiquidity penalty.' Tokenization flips it: add a 24/7 secondary market and locked value becomes tradable value. Real estate, private credit, fine art all get a liquidity premium. How big is that premium?

@OndoFinance is currently the clearest winner in the RWA / tokenization space on @solana .

They’ve brought:

ethereum:0x1b19c19393e2d034d8ff31ff34c81252fcbbee92 (tokenized short-term US Treasuries) .

ethereum:0x96f6ef951840721adbf46ac996b59e0235cb985c (yield-bearing stablecoin)

200+ tokenized US stocks & ETFs

All live on Solana with deep DeFi composability (used as collateral on Kamino, Drift, Jupiter Lend, etc.).

Why @OndoFinance stands out:

Highest institutional credibility (BlackRock, Franklin Templeton, JPM partnerships + proper attestations)

Best liquidity and real utility — not just parking yield, but actual on-chain capital markets

Solana’s speed + sub-cent fees make 24/7 settlement and trading actually usable !

Exactly how real infrastructure shifts play out in crypto—not with a single "mainnet launch" or viral meme, but through relentless, compounding improvements that most people sleep on until the numbers become impossible to ignore.

Current momentum We're already seeing it in real time. Tokenized RWAs (ex-stablecoins) have climbed into the $25-36 billion range mid-2026, with strong growth from tokenized U.S. Treasuries (often the biggest slice, around $10-15B), private credit, funds like BlackRock's BUIDL (now pushing multi-billion AUM across reports), Ondo products, Franklin Templeton, and others .

This isn't hype-driven retail FOMO yet—it's mostly institutions and sophisticated capital chasing better yields, faster settlement (T+0 vs T+2/3), 24/7 liquidity, and fractional access to things that were previously gated.

The quiet compounding factors Your breakdown nails the mechanics:

Better rails: Chains like Ethereum (still dominant for institutional comfort), Solana (speed + low fees for more dynamic use), and specialized ones are getting the compliance wrappers, oracles (Chainlink's role here is underrated), and bridges sorted.

Cross-chain friction is still real (those 1-3% pricing gaps you see in reports), but it's shrinking.

More products: From tokenized Treasuries and money market funds yielding real-world rates on-chain, to private credit, real estate fractions, commodities (gold heavy), and even equities/ETFs in certain jurisdictions.

The flywheel is products that are boring-but-reliable (cash equivalents) pulling in capital that then collateralizes more complex stuff in DeFi.

Deeper liquidity: This is the key unlock. Once you have enough on-chain Treasuries and credit that can be used as collateral, borrowed against, or traded seamlessly, the effective market size multiplies. We're moving from "park money and earn yield" to actual composability. Early signs are there with protocols integrating these as margin/collateral.

Institutions paying attention: BlackRock, JPM, Franklin, Apollo, KKR, etc., aren't doing this for marketing.

They're solving real pain points in their own operations and opening distribution channels. The shift from pilots to production in 2025-2026 is evident.Why the "sudden" realization happensOne day the aggregate TVL, trading volume, and yield opportunities just cross a visibility threshold.

TradFi desks start allocating serious sleeves, DeFi users get used to 8-15% yields backed by real assets (instead of just crypto volatility), and regulators have clearer frameworks in more jurisdictions.

Then the narrative flips from "niche experiment" to "this is eating into traditional markets. "Projections vary, but $10-30T by 2030 isn't crazy if the plumbing works— that's not replacing everything, but capturing a meaningful slice of global fixed income !

RWAs wont arrive as one big overnight moment.

They compound quietly.

→Better rails.

→More products.

→Deeper liquidity.

→More institutions paying attention.

Then suddenly everyone looks around and realises tokenization has become one of the biggest markets in crypto.

Here's a capital-efficiency unlock most people miss: tokenized treasury funds like BUIDL can earn yield AND be posted as collateral simultaneously. One asset, two jobs. In legacy finance that's nearly impossible. On-chain it's default. Game-changer or risk?

The regulatory side for perps has definitely moved forward more than most people expected a couple years ago. Injective being US-built and one of the first to go hard on truly decentralized perps gives them a unique angle. The bigger question is execution — can they actually bring compliant, on-chain perps to regular US users at scale, or will it still be mostly offshore with workarounds? That part will determine if this becomes mainstream or stays niche.

Yeah, spot on. We’ve mostly been in the “get more assets on-chain” phase. The next one is about making that capital actually work harder — faster settlement, better collateral reuse, real composability, and less money sitting idle. That’s where the real efficiency gains show up.

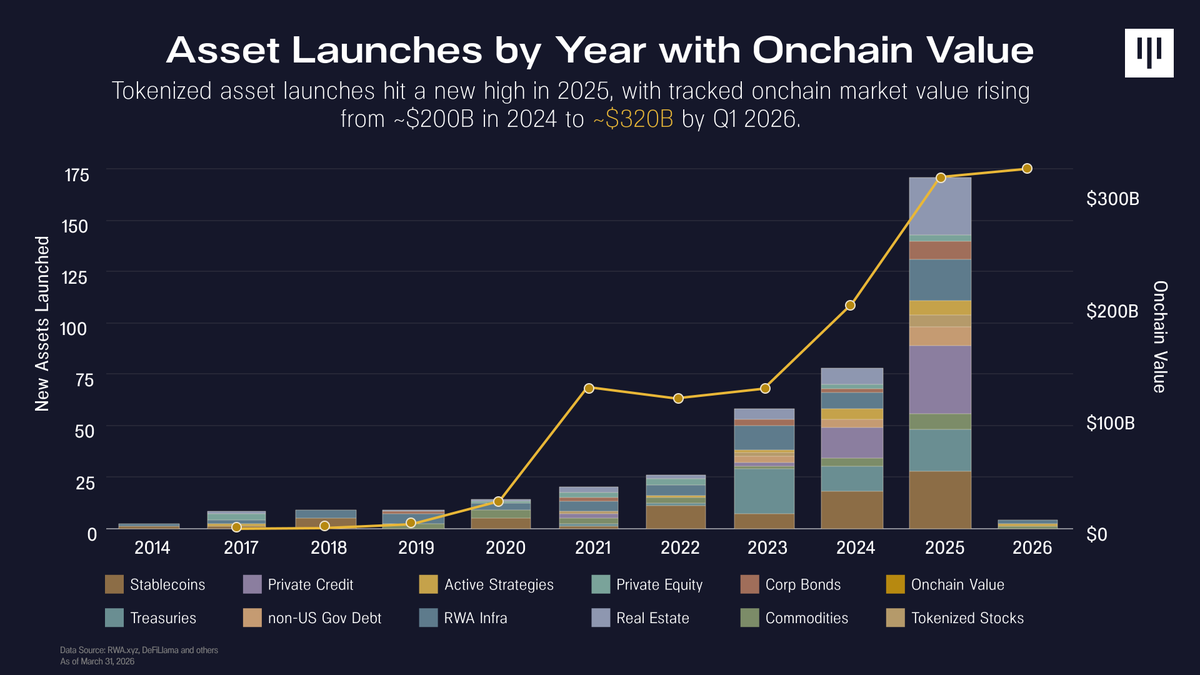

The Pantera report is solid. Growth is real — tokenized value went from ~$200B to $320B, with a record 168 new assets launched in 2025. Tokenized Treasuries and private credit are clearly the higher-quality parts of the market right now, and the composability angle is starting to show up in a few places.That said, the data also shows we're still early. Their Tokenization Progress Index averages just 2.04 out of 5, and nearly 78% of assets are basically just wrappers — digital copies of traditional stuff with limited real on-chain functionality. Stablecoins make up over 90% of the value and are still the only category with both scale and actual utility.The real signal isn't the headline number. It's whether we start seeing more native issuance, instant settlement, and actual composability instead of just putting old assets on blockchain. Right now, most of it is still representation rather than reinvention.We're building the rails, not riding them yet.

@PanteraCapital

The tokenization market is compounding with asset launches reaching a new recording in 2025.

Tokenized onchain value moved from ~$200B in 2024 to ~$320B by Q1 2026.

What stands out is the depth in asset quality, more native issuance/redemption, real-time settlement, and DeFi composability.

Read our full State of Tokenization Q1 2026 Report: https://t.co/eNKDSylULP

The U.S. Securities and Exchange Commission has registered Paxos Securities Settlement Company, LLC (PSSC) as a clearing agency under Section 17A of the Securities Exchange Act of 1934.

This makes Paxos the first and only blockchain-native firm approved to provide clearing and settlement services for eligible U.S. securities as a central securities depository — directly challenging the long-standing dominance of traditional players like the DTCC.

The approval enables Paxos to operate blockchain-based post-trade infrastructure, opening the door to faster settlement (potentially T+0), lower operational costs, reduced counterparty risk, and more efficient processing of securities transactions.This is a major milestone in bridging traditional finance and blockchain technology, particularly for tokenized securities and real-world assets (RWAs).