$MS beat consensus by 20% this morning.

If you parsed the April earnings call, you knew it was coming. The sell side didn't. Estimates never moved off $2.89. It printed $3.46.

The signals were sitting in plain sight:

Net new assets already running at $118B in Q1 Advisory revenue up 74% Earnings quality score on the call: 0.84 (recurring, diversified revenue, not a trading windfall)

That's the kind of quarter that repeats. Today it did: $148B of net new assets, records across wealth and trading.

But here's the reading nobody is repeating today.

We score the tone of every sentence executives speak. Separately for the script and for the Q&A.

Morgan Stanley's scripted remarks: 0.73 positive Under analyst questioning: 0.29 Confidence in the Q&A: slightly negative

The script is rehearsed and lawyered. The Q&A is real-time conviction, and it's much harder to fake for forty minutes than for ten pages. When the same executives who wrote an upbeat script turn cautious under questioning, and volunteer risks like tight spreads, rich asset prices, and private credit's "adolescent moment"...

The caution is the information.

Record numbers, guarded voices. That's what late cycle sounds like.

The beat was in the language three months ago.

So is the warning.

Estimates update quarterly. Language updates every time an executive speaks.

GBrain and Loop Engineering are quietly changing everything. I think they'll have a bigger impact than OpenClaw and Hermes.

The reason is that they move AI from stateless reasoning to persistent intelligence.

Connecting information across contexts and continuously iterating is what separates great decision-makers from average ones. AI is finally starting to acquire those capabilities.

Here's the part I think people are missing.

Country risk went from 2,500bps to 402. That trade is mostly done. What hasn't started is the earnings repricing. No MSCI inclusion, no passive bid, multiples frozen at half of fair.

$CEPU and $PAM are still priced like the old Argentina.

I can't state enough how undervalued these Argentine plays are once you place them in the global context.

Three names. Same business as their US peers. Half the multiple, sometimes a third.

The market partially repriced Argentina's macro risk but didn't repriced the companies in isolation.

The obvious pushback: US utilities deserve a premium for AI demand. Agreed. The fair EM comp is 10x to 14x.

$CEPU and $PAM sit at the bottom of that range too. I've run the adjustment. The discount survives it.

Love that this is happening.

If there’s one thing Argentina has, it’s a passionate culture that’s truly contagious.

More and more people will come to experience the strong sense of community and the bonds that make the country unique.

Adding $BBAR using gains from $BMA and $GGAL after their exceptionally strong six-month momentum. $BBAR remains a high-quality company and provides better diversification within the financial sector. Increasing exposure to $PAM, $VIST, and $CEPU ahead of a potential continuation of their rally, primarily funded by trimming $TXAR.

Also overweighting $MELI ahead of earnings season, as the recent surge in trading volume suggests a potential reversal of the recent downtrend.

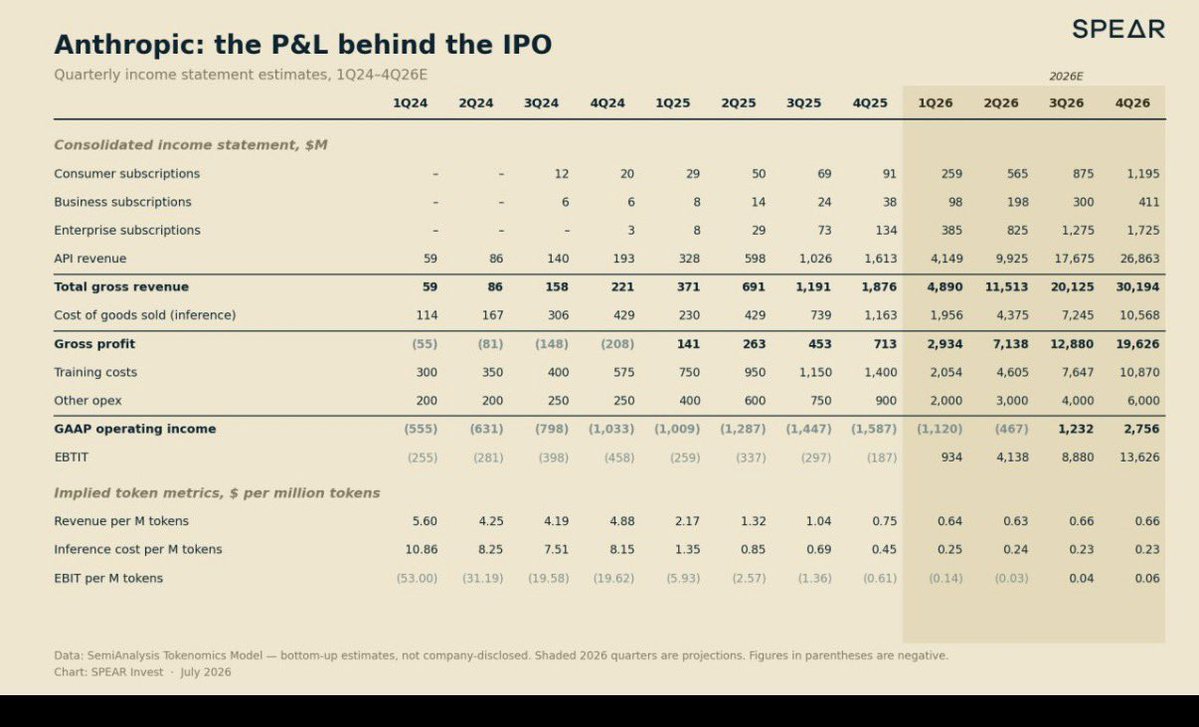

Everyone’s about to tweet “Anthropic profitable by 3Q26.”

The load-bearing number is one row down: training costs = $10.9B/quarter.

EBIT says +$13.6B. GAAP op income says +$2.8B. The gap is training.

“Profitability” here is a choice about how you expense the next model.