@Stable0752 Shouldn’t expect smooth, exponential adoption curve for these launches - not a weight loss pill. Monthly demand will increase stepwise as hospital P&T committees & formalised treatment protocols adopt. Only if Qrtly patient demand starts plateaus (ex. Seasonality) should we worry

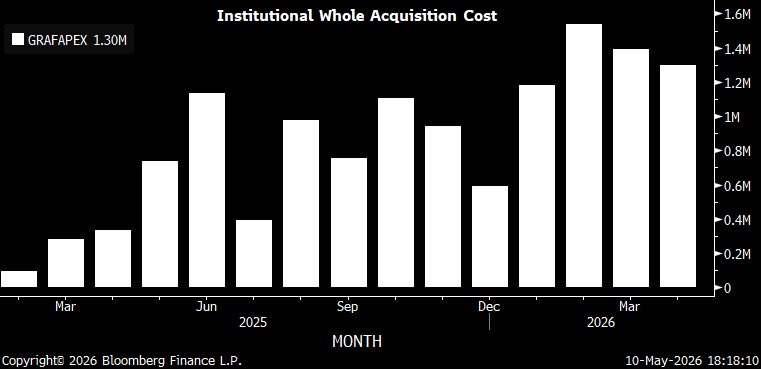

@Stable0752 1.3mn for grafa. 3.9x YoY. Also noting June was a big month last year, so will be interesting to see full Q after we know CYQ126 beat guidance.

Ixinity & Rasuvo had a solid April, too. 2.0mn & 2.9mn, respectively.

$mdp.to Medexus

Generational buying op. for $APO & $KKR. Both +20% FRE CAGR. Inflows will continue. + dry-powder mean current fears are an opp. to deploy. Sure there are weaker players w/ funkier non-sticky liabilities & opaque leverage - but it's not them. Many tourists in space rn.

$ZS (& many other cyber names) being thrown out with rest of AI-software fears. Great underwrite at these levels for a +20% ARR compounder in med. term, imo. I am a buyer & can look past sector SBC at these lvls as AI is tailwind for the biz and growth not broken.

@MrJulius007 This peak fear and capitulation if there is no real credit event coming down the pipe. Great valuation to underwrite at add imo - $112 for $15 2029/30E ANI.

@Pgrills24 Not a fan of $owl but this is an idiotic take. They’re a relatively asset light AM. Look @ balance sheet - completely different to a bank. Has gone from +20pe to ~10. Perhaps franchise and future fundraising is shot, but still have long term contractual mgmt fees worth something

@MrJulius007 @SageVeritas Same - Frustrating ST when own pnl isn’t ripping. on other hand, we’re LT owners of a wonderful biz and underwrite it at better valuation. More buybacks @ depressed px will only improve our LT CAGR. A doubled ANI by 2030 and a larger FRE mix can only be ignored so long…

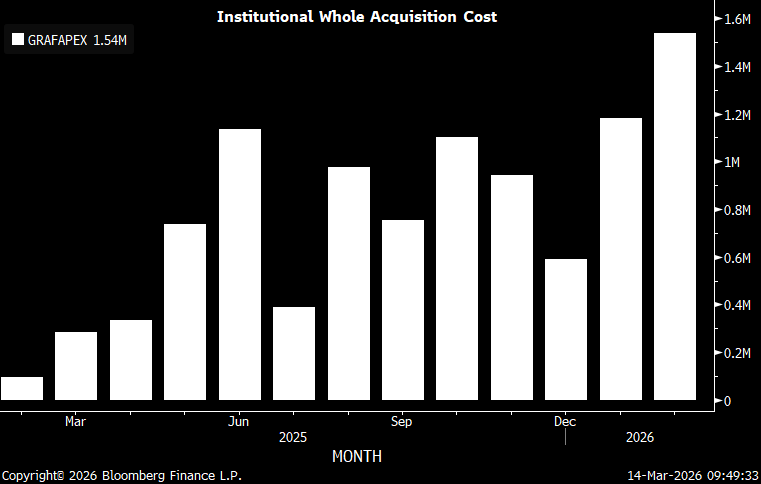

$mdp.to mkt continues to misprice Medexus as shrinking legacy biz rather than launching orphan drug platform. Fyq3 grafapex softness is technicality of rev. recog/wholesaler stocking & seasonality. Sequential patient demand +30%. & we saw unexpected stabilisation in rest of port

@MrJulius007 Where else can one get such a safe doubling of EPS within the next five yrs and for a sub 14x PE. Wonderful underwrite at this level imo. Also, think decent read across for APO earnings next week from KKR, Ares, BX, CG, OWL this week.

@Pgrills24 look at BS for the alt managers. Ares is asset light. p/b not right metric to price it. Names like APO & to a lesser extent KKR more BS intense from insurance BS. On a 27E PE Ares is c.16x vs JPM 14x - better metric to together with growth expectations etc. to eyeball things imo

@LuisVSanchez777@siyul Any thoughts on Parsons relative to BAH. Ofc at a premium to the rest of the govt defence serv. pack but keen to hear any other insights that could’ve driven BAH preference.

In the end, we have declining sales and margin profile on existing products, and increasing development risk as you look out on the cash-flows here today. Not too dissimilar to those other aforementioned names.

$Nvo reaction seems a little overdone. in the low 300s think you have a decent tactical trade here. However, I have not been enamoured by Novo for quite some time. A simple test I have for this is

That is unless you innovate and have new blockbusters that are so much better then the last one. But recall cagrisema, though better, is not much better than Eli Lilly’s and perhaps not sufficiently better to offset the premium cost. Who knows?