5) Near quarter end institutions rebalance their portfolios. I expect not just insane profit taking out of the AI winners but also billions shifting into bonds since the equity risk premium is crushed. US30Y is already building a top, previously stock tops followed right after.

4) Currently stock valuations are near all time highs, the $SPY shiller PE is in dotcom territory. What happens when people realise upcoming demand inflation isn't unlikely, 2020 debt needs to be refinanced or some stocks can't beat insane earnings expectations?

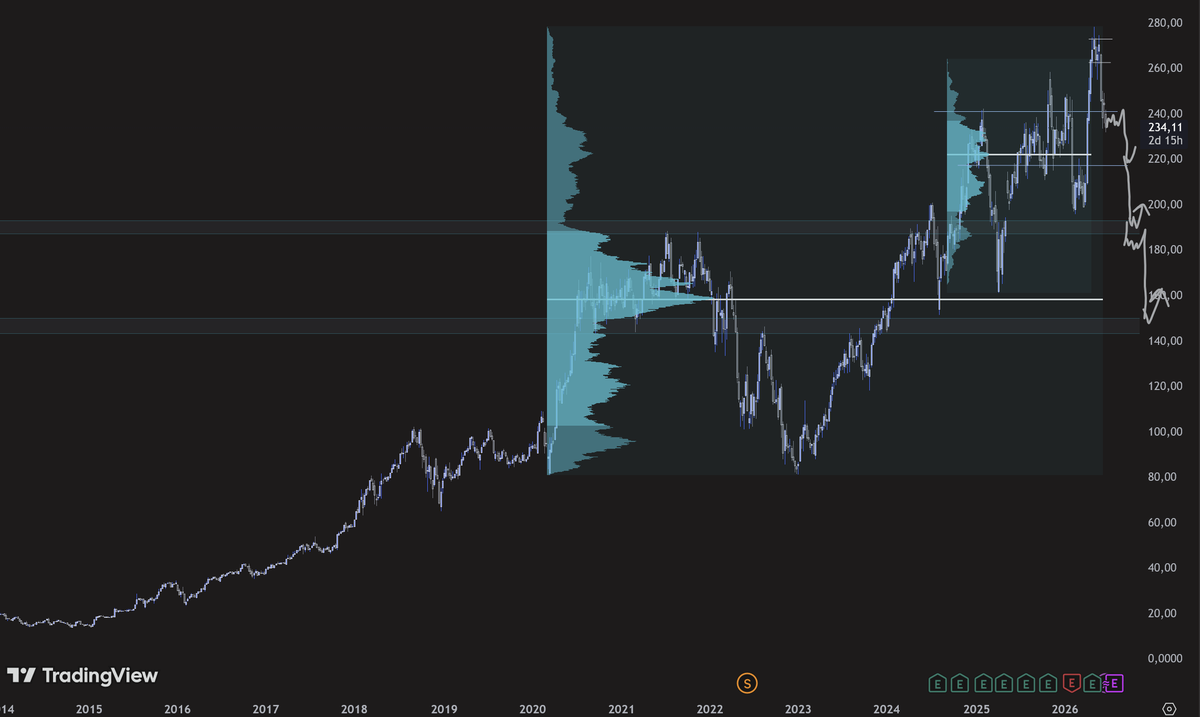

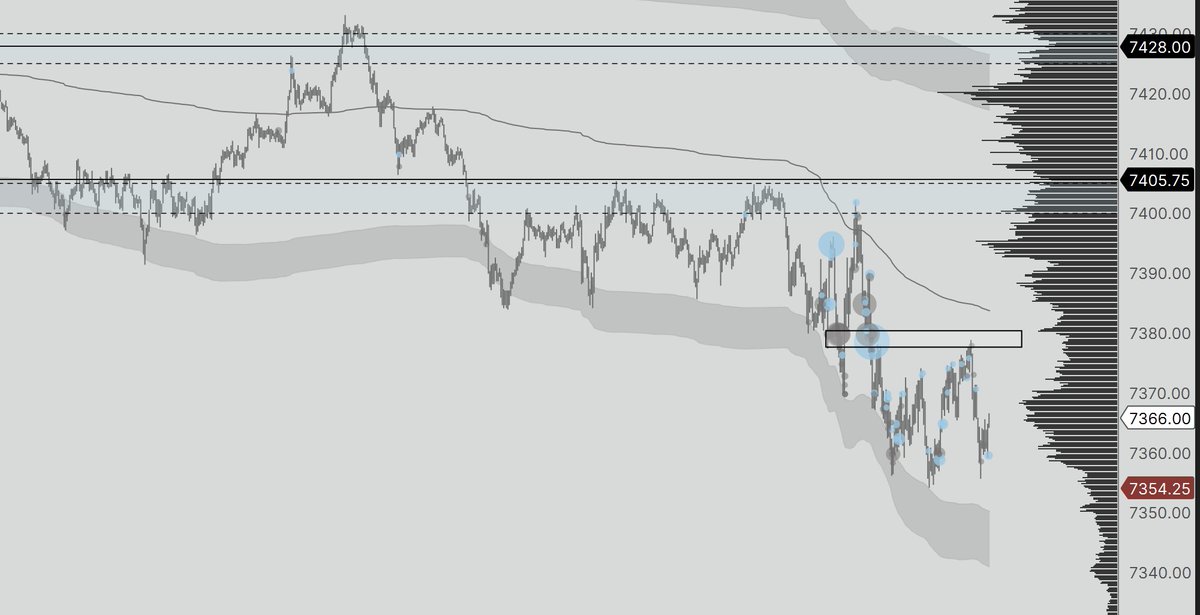

Here's an update for $MSFT. Showed a great reaction at the posted zone, if we move back below and displace through it I would be really really cautious.

🔥💯🎉TPT 50K ACCOUNT GIVEAWAY🎉💯🔥

How to enter:

1⃣Follow me

2⃣Repost and Like

3⃣Comment "50k"

(No region restriction, you'll need to be registered on TPT's website and send me your email).

Picking the winner Sunday near market open.

Good luck!

Right now, the stock market is trading at aggressive valuations because it assumes that if anything goes wrong, the Fed will step in and cut rates to save the day. Just recently I saw someone confidently explaining that the stock market can't crash anymore because everyone knows the Fed saves the market so the recovery is always priced in.

With the ISM Manufacturing PMI accelerating and input prices running hot, the Fed loses the ability to cut rates. If inflation begins to creep back up toward 4% (it does) because the economy is too hot, the market suddenly realizes that this theory is dead.

The realization that rates will remain restrictive indefinitely forces an immediate contraction in equity valuation multiples. We see forward looking growth indicators accelerating. That leads to a rally in long term bond yields like the 10Y. That will pull stocks down since it is more justifiable to invest into nearly "risk-free" assets with the high yields instead of expensive indices with less growth expectations. Additional the Treasury is forced to issue new debt at much higher yields to fund the government.

The massive supply of these high-yielding bonds actively sucks liquidity out of the private sector and equity markets.

Since inflation is a big part of this, the services PMI today will be really interesting. When services inflation hooks upward alongside manufacturing inputs (which are already at 82.1%), it proves inflation is no longer a localized supply chain issue (like oil or freight).

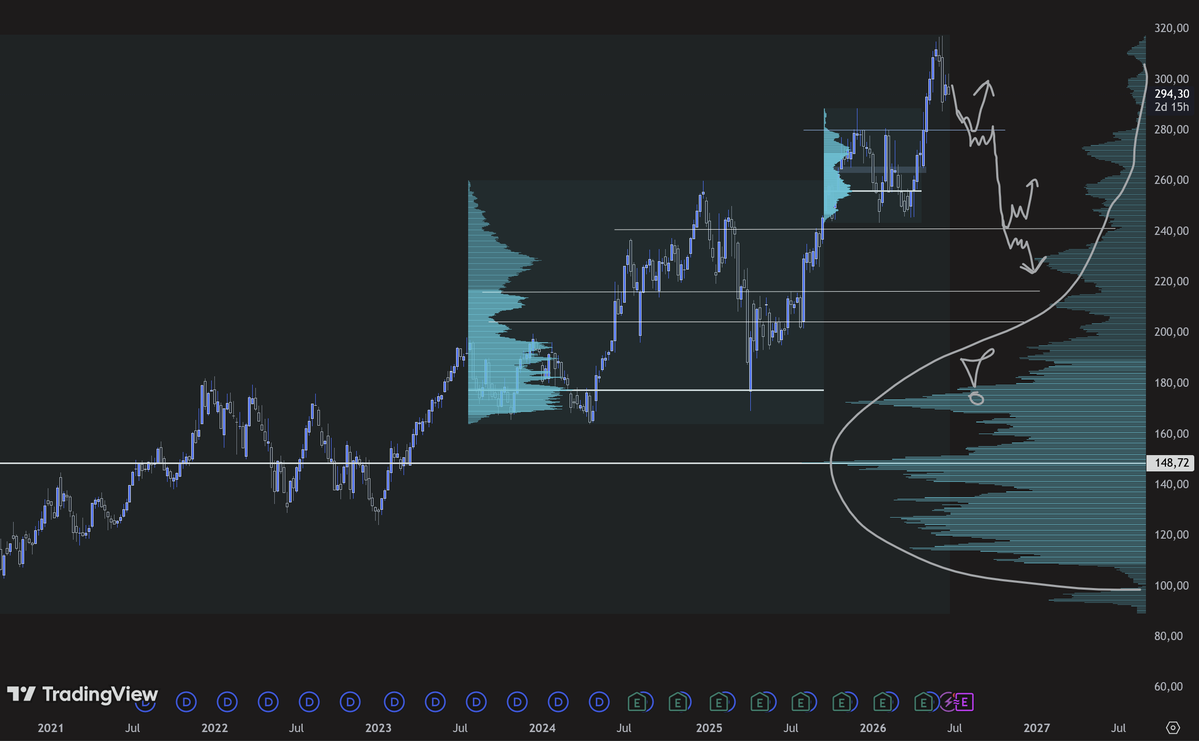

For me, there's no conformation without the chart. This doesn't need to happen now, ES could also show another rally before we crash!