AI agents are becoming the primary builders of software. The next generation of APIs will be designed for machines first, and humans second.

So we built our v2 API specifically for @claudeai & other LLMs. Just launched!

https://t.co/4C5TGjK4CR

📣 How to find out if a company isn't going to make it

☠️💀 If their software engineer interview process involves whiteboard puzzles, LeetCode tests, and trivia interviews.

This is a strong indication that the core part of their infrastructure exists in an outdated model. They are testing for irrelevant skills instead of the ability to build products, work with AI, ship code, learn quickly, and create business value.

The best builders with the highest value add will likely get filtered out before they ever get a chance to show what they can do.

@notsethbregman I didn't run a long vol fund.

What I was describing was a long vol fund, who often have a mandate to operate in. Artemis is a good example of a fund with a smart PM but had to play the tail hedge game and ultimately fail. They are not unique.

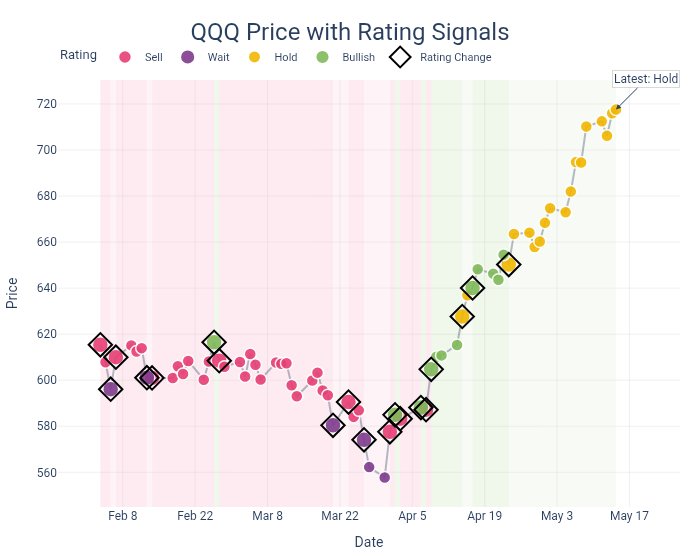

3 months of our daily $QQQ ratings below.

We have made it easy to be on the right side of market rallies.

This is perfect for people who just want to keep it simple.

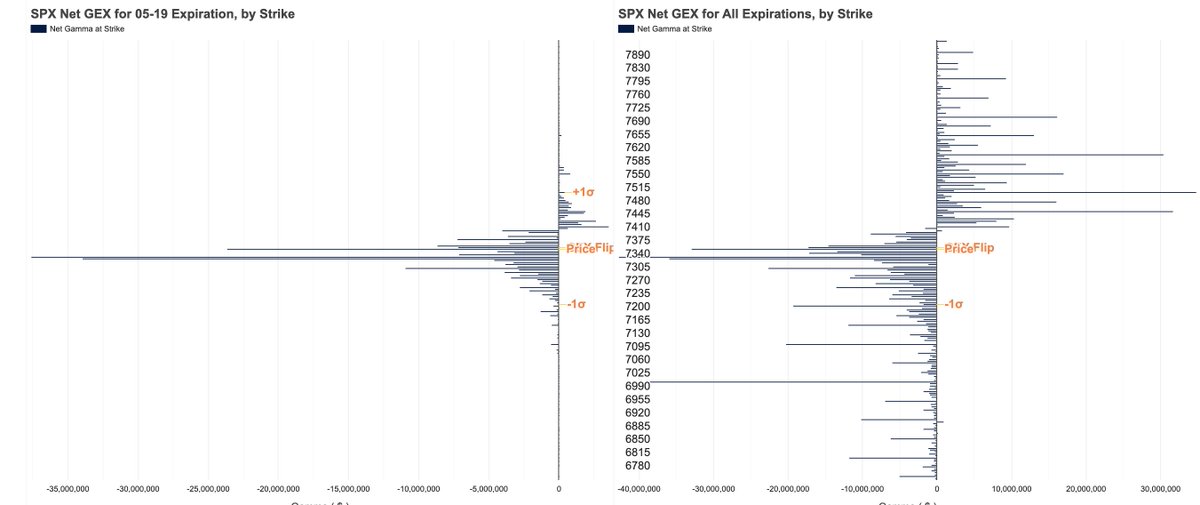

- no GEX complexity

- no sketchy trading bots

- no political / doomer bias

- no trying to call a top

https://t.co/pc0Lkt74PV

@MrBDelany Easier to own protection when it is built into a balanced portfolio because your returns will more closely track the market benchmarks (e.g. $spx ).

When hedging is done in a separate portfolio, the losses are very visible every month.

As a former PM who ran a long/short vol strategy, I’ll say the quiet part out loud so that aspiring PMs out there know:

Long Vol / hedging funds are doomed to fail because you are asking allocators to pay a visible, recurring insurance premium for an invisible benefit.

Long-vol funds sell convexity, but allocators judge linearly

The experience is down month,

down month,

down month,

down quarter,

down year,

hey we're up some,

down month,

down month,

down month,

wait why are you pulling money there is a vol spike coming.

The better structure is a balanced portfolio with a clearly defined vol / convexity sleeve.

Let the core portfolio compound.

Let the convexity sleeve protect the left tail, create liquidity in stress, and fund rebalancing when assets get cheap.

Standalone hedging is psychologically hard to own.

Embedded convexity is much easier to underwrite.

There’s always a valuable lesson and a positive takeaway in every fund collapse.

I’m no volatility expert, and I hope someone does a thorough autopsy of what happened, but here are my immediate takeaways:

1) Tail risk hedging is really, really hard. There’s a reason the classic 60/40 stock/bond portfolio remains the most popular allocation in the world: the 40% in bonds is still the simplest, most reliable positively asymmetric long-term hedge most investors can implement. It’s not perfect, but it’s “good enough” for the vast majority of people who just want durable diversification without needing to be geniuses.

2) Shorting (and short vol strategies) is also really, really hard. You’re fighting the long-term upward drift of markets, dealing with asymmetric payoffs that require big moves to pay off, and battling time decay plus carrying costs. What looks elegant on a backtest becomes brutally difficult in live markets.

At the end of the day, the clearest lesson is this: investing is hard. You don't need to make it harder.

If you decide to actively trade, time the market, or run sophisticated strategies, understand that you’re voluntarily making an already difficult game even tougher. You might capture more upside along the way, but the margin for error shrinks.

I hope everyone finds some positivity in all of this.

The 30 year treasury yield is now 5.1%

Convincing my wife to sell our house

We’d net $800k after closing

Dump all that into 30 year bonds

Collect $40k/year for 30 years

Use that money to pay rent

Never deal with the lawn or a leaky roof

And get my $800k back in 30 years 😳