The homebuilder market is in its biggest recession since 2009.

Months of supply for homes under construction is now 14.8 months. Permitted homes not yet started have surged to a record 21.3 months.

Both are similar or worse than the 2008-09 housing bust.

Suggesting that future demand for new construction is in the tank.

The one exception is completed spec homes, where the months of supply is just 3.9 months.

Builders can still sell move-in-ready inventory, especially when paired with mortgage rate buydowns and incentives.

But anything further out in the pipeline is piling up.

The result: builders are struggling to justify tomorrow's construction, and this builder recession is likely to get worse. Don't be surprised if we see a big pullback in starts at some point.

Track building permit data by county on Reventure Mobile:

https://t.co/dBXshG2eiP

@dampedspring Slowing of central bank gold buying. Its most likely a reason for what feels like persistent softness we are seeing right now. That's cause its so critical to keeping the market tight and squeezed to upside when waves of retail come in.

@Shelpid_WI3M By the way, it is the weather. Super El Nino causing drought in one area and flooding in another. Also, we are in a fourth turning. Bad all around, but markets are not free so hard to see.

@Shelpid_WI3M Glad I found you on Twitter. I am reading the book 1873 right now - railroads leading to the panic & depression. And have been a follower of Kondratiev, who I came to know thru Phil Anderson. The chart you poster, I’ve seen, but Samuel Benner & his story, I did not know.

BREAKING: Oil has officially fallen below $72 for the first time in 112 days.

Crude is now down -40% from its march peak and sitting just $4 above pre war levels.

ASWATH DAMODARAN: PRIVATE CREDIT IS THE NEXT CRISIS.

His framing starts with a question that nobody in the boom is asking. Who exactly are the lenders writing the checks to fund all these AI data centers? Shale oil companies borrowed heavily when oil was at $120 a barrel and got crushed when prices fell to $60. The same pattern is forming today in compute infrastructure, and the people putting up the capital are getting almost no scrutiny.

Damodaran does not see private credit as the sophisticated, intelligent alternative the marketing has positioned it as. He sees it as sheep. Every fund is chasing the same deals, the same sectors, and the same yield premiums that allegedly justify the structure. Intelligence in his view has been confused with confidence, and confidence in this corner of finance has compounded into something far more dangerous than the participants realize.

His broader point is that hedge funds, private equity, and private credit have all followed the same destructive arc. Each one began as a genuinely good niche business solving a real problem. Hedge funds 30 years ago produced positive alpha, beating passive investing by 3 to 5 percent annually. Today they look like expensive mutual funds, underperforming passive by roughly 1.5 percent. Private equity started as a focused, disciplined strategy for a small set of operators and has grown into a sprawling category that now struggles to deliver the returns that justified its emergence. Private credit had a legitimate original purpose, which was lending to borrowers that banks structurally could not serve.

What killed each of these businesses was the same disease. Overreach. A $200 billion niche business gets sold as a $20 trillion opportunity. When that scaling happens, sloppiness follows, bad actors enter the space, and the average quality of every participant deteriorates. The original alpha disappears not because the strategy stopped working, but because too much money chased too few good deals.

The danger with private credit is far more severe than the parallel problems in private equity and hedge funds. Equity investors take their losses and move on. Lending businesses, when they overreach, take others down with them. Banks. Pensions. Insurance companies. Sovereign wealth funds. The systemic linkages run far deeper than most participants understand, and the social costs of a real default cycle in private credit would extend well beyond the funds themselves.

Damodaran's warning is essentially that the industry is repeating the exact mistake that produced every previous credit crisis. Take a good idea, scale it past its natural capacity, attract bad actors with the promise of easy returns, and wait for the inevitable cycle that exposes how much of the underwriting was never serious in the first place.

@AswathDamodaran@FixedFloating

The big Oil Companies are not dropping their price at the pump commensurate with the sharply lower prices they are paying for Oil. Those prices are dropping like a rock! In other words, customers are being “gouged.” I have instructed the DOJ to immediately start looking into this. Gasoline prices better start going down a lot faster than what I’m seeing! President DJT

( TS: Jun 24 2026, 12:12 AM ET )

BESSENT SAID INFLATION IS EXPECTED TO RETURN TO TARGET AND ADDED THAT PRESIDENT TRUMP AND THE TREASURY UNDERSTAND THE IMPORTANCE OF THE BOND MARKET, EXPRESSING CONFIDENCE THAT FED CHAIR KEVIN WARSH WILL BALANCE ECONOMIC GROWTH WITH PRICE STABILITY.

JUST IN: GOOGLE $GOOGL IS JOINING THE DOW JONES INDUSTRIAL AVERAGE

It will replace Verizon $VZ in the index, effective before the open on June 29, per S&P Dow Jones Indices.

The Dow is the most-watched stock index in the world, and unlike the S&P 500, it holds just 30 companies. Getting added means every Dow-tracking fund now has to own the stock.

The move caps a notable stretch for Google, which dropped about 5% Monday and slipped again Tuesday on concerns about AI talent leaving the company. It joins the Dow anyway.

Honeywell will remain in the index.

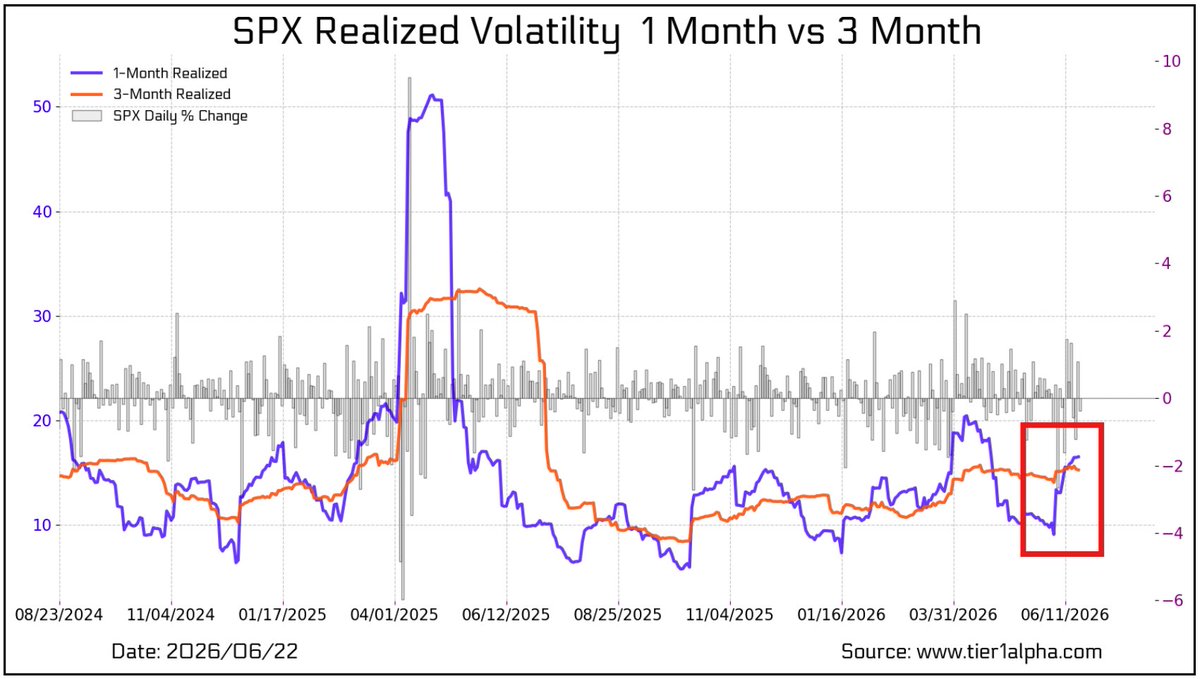

S&P 500 realized volatility:

1-month has crossed 3-month realized vol, suggesting that volatility control funds will be rebalancing toward the downside.

🚨BLACK TUESDAY in the South Korean stock market:

The Kospi index CRASHED -10% on Tuesday, its 3rd-largest single-day decline in history, also triggering a 20-minute trading halt after falling more than -8% intraday.

The Kosdaq index also plunged -8%, falling below the 900 mark for the first time this year.

Samsung and SK Hynix both dropped -12%, while Hanmi Semiconductor fell -14.4%, with every major sector closing in the red.

Meanwhile, foreign investors and institutions sold a combined ~8.6 trillion won ($5.6 billion) of Kospi shares during the session.

Sentiment turned negative after SK Hynix was reported to be slowing its HBM4 mass production expansion, while broader tech weakness in US markets overnight added to selling pressure.

Massive forced liquidations added to the pressure, with retail margin debt at a record 38.5 trillion won ($25 billion).

The world's best-performing market is turning into the worst-performing.

Is the South Korean BUBBLE BURSTING?

LIQUIDITY CONDITIONS DETERIORATE AS KEY LEADING INDICATOR TURNS NEGATIVE FOR FIRST TIME SINCE 2021

WARNING SIGNAL FLASHES: EXCESS LIQUIDITY INDICATOR FALLS BELOW ZERO