I valued SpaceX for its IPO a few weeks ago, with minimal information and a promise to revisit the valuation, when the prospectus was made public. The prospectus is public, the offering price has been set and my update is up and running. https://t.co/zRjpD1C0wv

Nicolai Tangen, CEO of Norges Bank Investment Management pressed IBM CEO Arvind Krishna directly on whether AI is a bubble (Save this).

And Krishna responded with what has become known inside financial circles as the $8 trillion math problem.

A single gigawatt of AI data center capacity filled with accelerators, liquid cooling, and power infrastructure costs roughly $60 to $80 billion to build and populate.

The industry has committed to more than 100 gigawatts of buildout globally.

That is $6 to $8 trillion in capital expenditure and because AI grade hardware depreciates on a five-year cycle, that entire sum must be effectively replaced and refreshed every five years.

To service the interest on $8 trillion in capital at a conservative 10% borrowing rate, the AI ecosystem would need to generate approximately $800 billion in annual profit, a number that currently exceeds the combined net income of every large technology company in the world.

Goldman Sachs estimates $7.6 trillion in aggregate AI CapEx between 2026 and 2031 alone, and Reuters Breakingviews has flagged that even if the capital is available, physical bottlenecks power permits, land, cooling infrastructure, and electrical grid connections mean that half of the planned data center projects are being cancelled or delayed before they ever go live.

Krishna also raised a second, structurally distinct concern that markets have largely ignored.

He argued that the largest foundation models, GPT, Gemini, Claude, Llama are converging toward commodity status.

When a product is a commodity, switching costs collapse.

When switching costs collapse, pricing power evaporates and margins compress regardless of how much capital was spent building the capability.

Morningstar's equity research team conducted a review of 132 technology companies in 2026 and found that AI had caused moat rating downgrades across roughly 40 major stocks concentrated in enterprise software, IT services, and SaaS with Adobe, Salesforce, Workday, and ADP among the companies whose competitive moats have materially weakened.

The implication is that the companies spending the most on AI model development may be building an asset that is simultaneously the most expensive to produce and the most difficult to monetize with durable margins.

This bear case is serious but it is also incomplete and that is what makes Krishna's framing so important to understand precisely.

When pressed further, Krishna explicitly said he does not believe there is an AI bubble in the technology itself only in a subset of the infrastructure capital that is being deployed against speculative assumptions rather than proven demand.

He draws the same analogy, the fiber optic overbuild of the late 1990s. Dozens of companies went bankrupt laying cable that nobody was using.

And yet that exact "wasted" infrastructure became the physical backbone of every cloud company, every streaming service, every mobile network, and every modern AI training cluster that followed.

The builders lost, the infrastructure won.

And the companies that were built on top of it, Amazon, Google, Netflix, Salesforce compounded for two decades.

The question, as Krishna framed it, is not whether AI is real.

It is which capital deployment earns a return versus which gets stranded and crucially, whether you own the stranded assets or the companies built on top of them.

On winners, Krishna was direct that distribution is the moat on the consumer side, and enterprise is wide open.

The data supports this, Meta with 3.3 billion daily active users across Facebook, Instagram, and WhatsApp is building AI into a distribution network that no startup can replicate at any cost.

Meanwhile, the productivity evidence arriving in real time is beginning to challenge the bear case's revenue projections.

Jensen Huang just showed on stage at Computex that GitHub commits, the universal measure of global software output nearly tripled in the first months of 2026, effectively converting $3 trillion in developer salaries into $9 trillion in productive output.

That is measurable, real time economic value already flowing through the system and it feeds directly back into token demand in a compounding loop that Krishna's static CapEx math does not fully capture.

This is unsustainable: personal spending growth is surging while income growth is collapsing, resulting in an extremely rapid drain of personal savings

@LaBulll I mars 2000 var jag på ett investerarmöte med Sycamore Networks (fiberoptik) på St Regis i NYC. NY Fire Dept avslutade mötet pga att vi var för många i lokalen.

The real surprise today was the downward revision to first-quarter real GDP growth to a +1.6% annual rate from the initial estimate of +2.0%. If you recall, there was a time in the middle of the quarter when the ballyhooed Atlanta Fed Nowcast model was predicting a number well north of +3.0%. For some perspective, AI capex zoomed ahead at an unprecedented +23% annual rate, while the rest of business capex dipped -7.9% (after a -13.1% drubbing in Q4) and industrial/commercial construction tanked -5.4% QoQ, riding a nine-quarter losing streak. Tack on the fact that the residential sector contracted at a -6.3% annual rate, printing negatives in each of the past five quarters. When you look beyond the AI binge, the federal government reopening effect, the impact from the further savings drawdown (equity wealth effect at the high end and financial distress at the low end), and the inventory swing, the economy actually contracted at a -1.1% annual rate in Q1! You don’t need to have the world’s best optometrist to see the lack of overall vitality in this economy beyond the tech sector.

The real surprise today was the downward revision to first-quarter real GDP growth to a +1.6% annual rate from the initial estimate of +2.0%. If you recall, there was a time in the middle of the quarter when the ballyhooed Atlanta Fed Nowcast model was predicting a number well north of +3.0%. For some perspective, AI capex zoomed ahead at an unprecedented +23% annual rate, while the rest of business capex dipped -7.9% (after a -13.1% drubbing in Q4) and industrial/commercial construction tanked -5.4% QoQ, riding a nine-quarter losing streak. Tack on the fact that the residential sector contracted at a -6.3% annual rate, printing negatives in each of the past five quarters. When you look beyond the AI binge, the federal government reopening effect, the impact from the further savings drawdown (equity wealth effect at the high end and financial distress at the low end), and the inventory swing, the economy actually contracted at a -1.1% annual rate in Q1! You don’t need to have the world’s best optometrist to see the lack of overall vitality in this economy beyond the tech sector.

Thanks @tomkeene. So why did Rockefeller stop vertically integrating at the gas pump and never build the car? I knew you would come back on this...

Rockefeller followed one rule: never put a dollar where you're a price-taker. Only own the bottleneck where you set the price. It's the same rule the hyperscalers are breaking.

He stopped integrating beyond the pump, as owning Detroit would have meant pouring capital into a competitive, capital-intensive, price-taking manufacturing business. Gasoline and cars are complements, not substitutes, and you want your complement industry fragmented and competitive. Cheap, abundant cars from Ford and GM meant more fuel sold at higher margin.

The artificial muscle (AM) revolution was ultimately about oil, not the cars planes and trucks that did the heavy lifting. Decades ago, Buffet called them the worst kinds of businesses: ones that grow fast, devour capital and earn little on it. He said if he would have been at Kitty Hawk he would have shot Orville down because "Karl Marx couldn't have done as much damage to capitalists as Orville did." This is exactly the charge now being levelled at the hyperscalers: rapid growth, insatiable demand for capital, and returns that don't clear the cost of it.

But the key here is that Rockefeller wanted the cheap abundant trains, planes and automobiles as he controlled the choke point. The ability to turn crude into gasoline, diesel and aviation fuels.

Similarly, the AI revolution will likely be about atoms, not bits, as that’s where the choke point ultimately is. Chips, turbines, transformers – hence critical minerals. In the new AI race the actual chokepoint has moved off bits entirely, onto atoms: silicon, where Nvidia sets the price, and the commodity complex underneath it: copper, steel, gas, uranium, the metals and molecules.

With the exception Google’s TPU, they own very little of this. Think of Google with its TPU as the Gulf Oil/Mellons that became Chevron.

So who is the Standard Oil of the AI story: Its Nvidia. Both with c.85% market share. I am sure Jensen keeps a copy of Dan Yergin's The Prize for nighttime reading as he has played it to the tee.

But unlike Standard Oil, Nvidia doesn’t control its crude supply. It has TSMC and ASML to contend with. So what does the AM revolution tell you about what could happen to Nvidia, TSMC and ASML in the AI revolution?

"Professor, don't you find it curious that a new US-Iran peace deal leaks almost every time the 10y UST yield breaks 4.4% on the upside?"

"Actually, if I think about it, I don't find it curious at all."

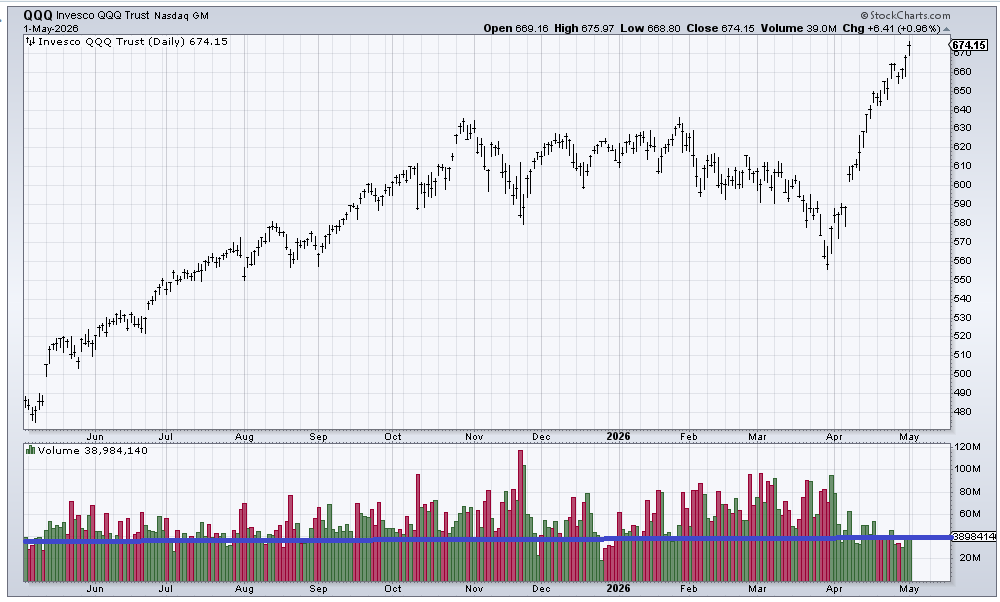

I typically could care less about volume. Stocks can and do rally on low volume. But I am struck by the consistent low volume rally in the QQQs. Just fell off a cliff as we came off the low.

We thought we were getting a TACO

"Trump Always Chickens Out"

But so far we are getting a NACHO

"Not A Chance Hormuz Opens"

(With appreciation to the trader who told me)

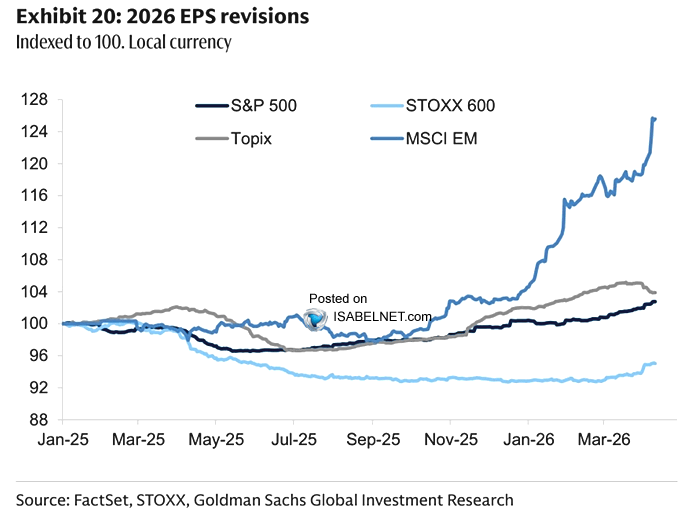

📌 EPS

Upward EPS revisions across the S&P 500, the STOXX 600, and particularly MSCI EM, point to rising confidence in 2026 earnings, with momentum still leaning toward strength

👉 https://t.co/blMxcoFA78

@GoldmanSachs#earnings#EPS $spx #spx#stocks#stoxx#topix

This 1-hour Yale lecture will teach you more about options trading than most people learn in an entire Wall Street career.

Most people skip it.

It comes from Robert J. Shiller at Yale University and instead of surface-level tips, it breaks down the exact thinking and models hedge funds rely on.

Watching it feels like unlocking a different level.

You start to see that options aren’t just trades they’re structured bets on probability, time, and behavior. The real edge isn’t guessing direction, it’s understanding how risk is priced and where others are wrong.

He also makes one thing clear: complexity isn’t the advantage clarity is. The people who win aren’t the ones using the most complicated strategies, but the ones who truly understand what they’re doing.

That’s why this lecture stands out.

Because while most people are chasing quick profits…

Very few actually understand the game they’re playing.

Bookmark this and watch it, no matter what. It might be the most productive start to your week.

$EWZ

Why aren't you bullish on Brazil?

Brazil is no longer just a cyclical commodity play. Instead, it's capturing far more value from the AI buildout than many realize.

Think of it this way...

AI is not just a software revolution - it's a mineral intensive industrial transformation:

-> GPUs

-> Cooling systems

-> Humanoids

-> Precision motors

They all need huge levels of critical minerals of which most are held in China.

Brazil holds the world's second-largest rare-earth reserve and it's no longer just an exporter of raw materials.

Every hyperscaler needs a NON-CHINESE rare earth hedge, and so far, that is turning out to be Brazil.

And this is only a small piece of the thesis. Add in:

1. Whilst the US and Europe wait years to connect a data center to the grid...Brazil is authorizing multi-gigawatt AI campuses powered by surplus renewables.

2. Real rates are falling as the dollar weakness. That should re-rate long-duration AI infrastructure assets and this is where Brazil is strong.

Long Brazil.

What are your top Brazilian stocks?