We owe those who serve the UK the kit to do the job and the loyalty to stand by them when it's done. We are failing on both.

I’ve spent my whole time in government making that case. Number 10 will not listen, so I am resigning as Minister for the Armed Forces.

Letter to the PM below.🫡🫡🫡⬇️⬇️

Impossible to overstate the scale of China's transformation into an automotive export machine. Monthly exports of vehicles, annualized, were 12m in May; annualized exports of passenger cars were 10m in May

1/

Oil exports bypassing the Strait of Hormuz have risen by 1.5 mb/d to nearly 8 mb/d, led by Saudi Arabia & the UAE. Despite this, flows remain far below pre-war levels.

At the same time, Iran's exports via the Strait have been curtailed by a US blockade: https://t.co/hQNZ0TtjuZ

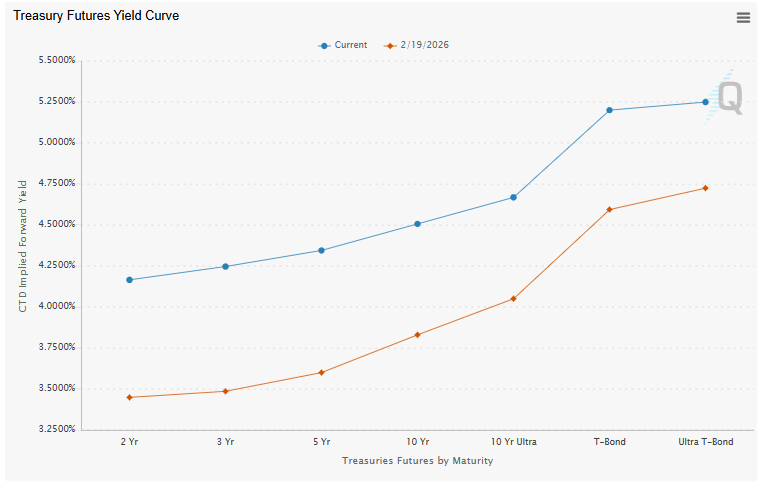

Contrary to what many may believe, I think the bond market has been extremely benign in the US. Imagine an economy that

1. runs perpetually high deficits, irrespective of the level of unemployment

2. has had inflation running above the central bank target for five years

3. pursues foreign policies that push every other major economy to issue more debt

Now add

4. Supply shock (oil/fertilizers) on the heels of a tariff shock it had barely recovered from, which is inflationary in itself and also forces foreign countries to defend their own FX

5. Newly appointed central bank chair that is perceived to be *unusually* dovish on the policy rate while being hawkish on the Balance Sheet.

In this context, do bonds seem oversold? I don't think so. For bonds to be cheap, we need

A. War to end (or genuine confidence that the war will end soon and flows resume from SoH, not just jawboning)

B. Unemployment rate to spike (given the falling labor force, this will probably require firms to lay people off)

C. Chair Warsh to lean hawkish on policy rates (counterintuitive, but this would be useful for the long end, not short... but the short end is going to react to data anyway, so better over promise to under deliver)

D. The rise in term premia cracks broader risk markets and risk parity returns (circular logic, and may not always work - recall 2022).

Either way, my point is - this was the most obvious and completely expected outcome if the war continued as long as it has.

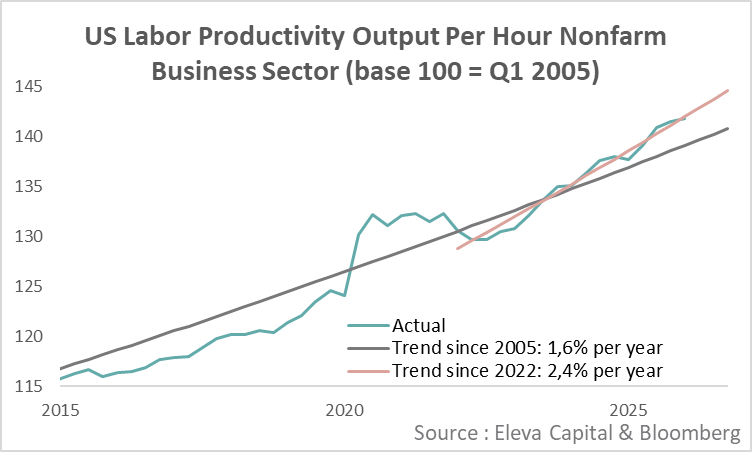

US nonfarm productivity rose +0.8% in Q1 this year.

What’s striking is that the productivity trend since 2022 appears noticeably stronger than before. First signs of an AI-driven productivity boost?

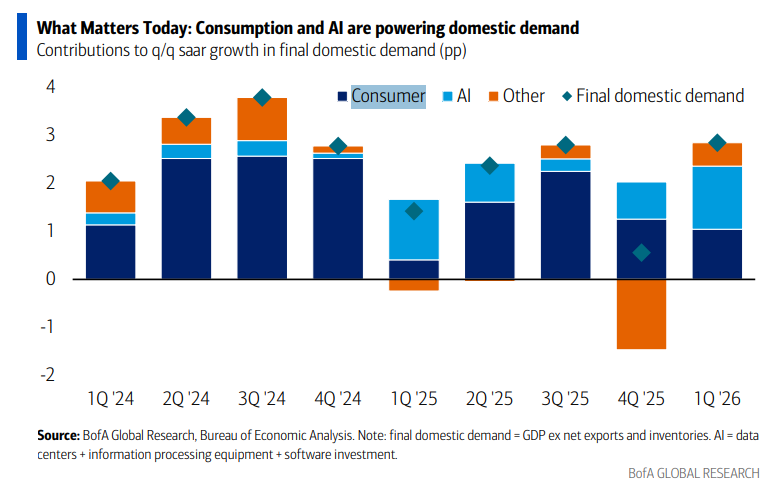

BofA: Consumer spending and AI are responsible for the entirety of domestic demand growth since the beginning of last year.

While our base case is sanguine, the Iran war poses key downside risks to both of these pillars

Endorse.

The standard conception of economic power has shifted from influence over rules and norms to control over choke points and the political ability to use a choke point

Tis a huge change

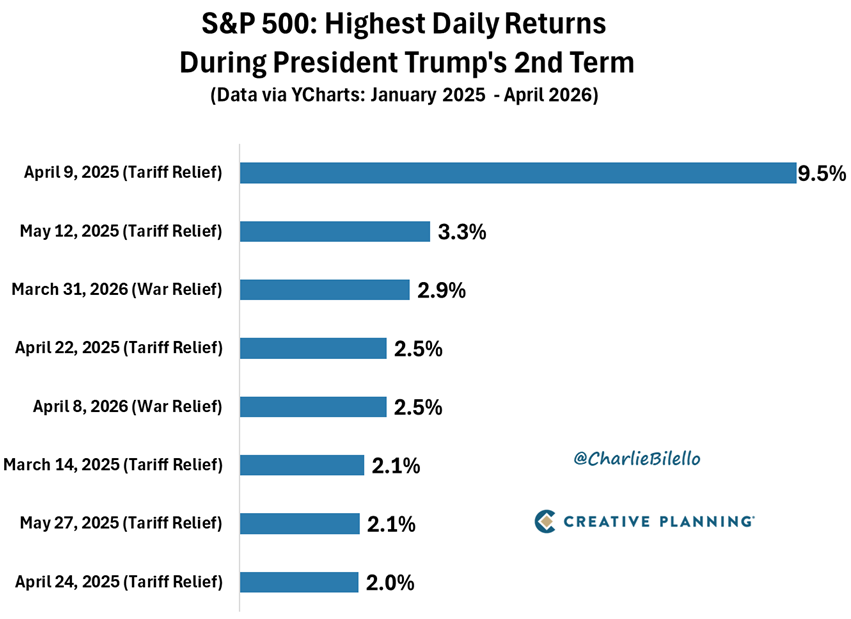

The 8 best days for the S&P 500 during President Trump's second term were all “TACO trade" rallies, with sharp reversals from the president on Tariffs driving the biggest gains in 2025 and reversals on the Iran War driving gains in 2026. $SPX

Video: https://t.co/Zx4irhzfL7