People don’t realize how much chaos is coming for Bitcoin in the next few months.

Bitcoin mining has entered its most unprofitable stretch in a decade. It currently costs a whopping $112K to mine a single Bitcoin, that’s now only worth $86K and falling fast.

It’s only a matter of time before miners shut down, the network shrinks, and a cascading crash follows.

BREAKING: The $610 Billion AI Ponzi Scheme Just Collapsed

Last night at 4pm EST, something unprecedented happened. Nvidia stock rallied 5% on earnings, then crashed into negative territory within 18 hours. Wall Street algorithms detected what humans couldn’t: the numbers don’t add up.

Here’s what they found.

Nvidia reported $33.4 billion in unpaid bills, up 89% in one year. Customers who bought chips haven’t paid for them yet. The average wait time for payment stretched from 46 days to 53 days. That extra week represents $10.4 billion that may never arrive.

Meanwhile, Nvidia stockpiled $19.8 billion in unsold chips, up 32% in three months. But management claims demand is insane and supply is constrained. Both cannot be true. Either customers aren’t buying or they’re buying without cash.

The cash flow tells the real story. Nvidia generated $14.5 billion in actual cash but reported $19.3 billion in profit. The gap is $4.8 billion. Healthy chip companies like TSMC and AMD convert over 95% of profits to cash. Nvidia converts 75%. That’s distress level.

Here’s where it gets criminal.

Nvidia gave $2 billion to xAI. xAI borrowed $12.5 billion to buy Nvidia chips. Microsoft gave OpenAI $13 billion. OpenAI committed $50 billion to buy Microsoft cloud. Microsoft ordered $100 billion in Nvidia chips for that cloud. Oracle gave OpenAI $300 billion in cloud credits. OpenAI ordered Nvidia chips for Oracle data centers.

The same dollars circle through different companies and get counted as revenue multiple times. Nvidia books sales, but nobody actually pays. The bills age. The inventory piles up. The cash never comes.

AI company CEOs admitted it themselves last week. Airbnb’s CEO called it vibe revenue. OpenAI burns $9.3 billion per year but makes $3.7 billion. That’s a $5.6 billion annual loss. The $157 billion valuation requires $3.1 trillion in future profits that MIT research shows 95% of AI projects will never generate.

Peter Thiel sold $100 million in Nvidia on November 9. SoftBank dumped $5.8 billion on November 11. Michael Burry bought put options betting Nvidia crashes to $140 by March 2026.

Bitcoin, which tracks AI speculation, dropped from $126,000 in October to $89,567 today. That’s a 29% crash. AI startups hold $26.8 billion in Bitcoin as collateral for loans. When Nvidia falls another 40%, those loans default, forcing $23 billion in Bitcoin sales, crashing crypto to $52,000.

The timeline is now certain. February 2026, Nvidia reports fourth quarter and reveals how many bills aged past 60 days. March 2026, credit agencies downgrade. April 2026, the first restatement. The fraud that took 18 months to build unwinds in 90 days.

Fair value for Nvidia: $71 per share. Current price: $186. The math is simple.

This is the fastest moving financial fraud in history because algorithms detected it in real time. Human investors are 90 days behind.

Read the full data driven deep dive article here - https://t.co/sDEf5Mdrtc

🔥 If you own $TSLA, stop scrolling and watch this.Long-term, Tesla still targets $700–$800...

but the weekly BX just flipped red and we could see a pullback to $350–$360 first.

This is the exact roadmap I’m using and it could save you a ton of pain.

🎥 Full $TSLA breakdown 👇

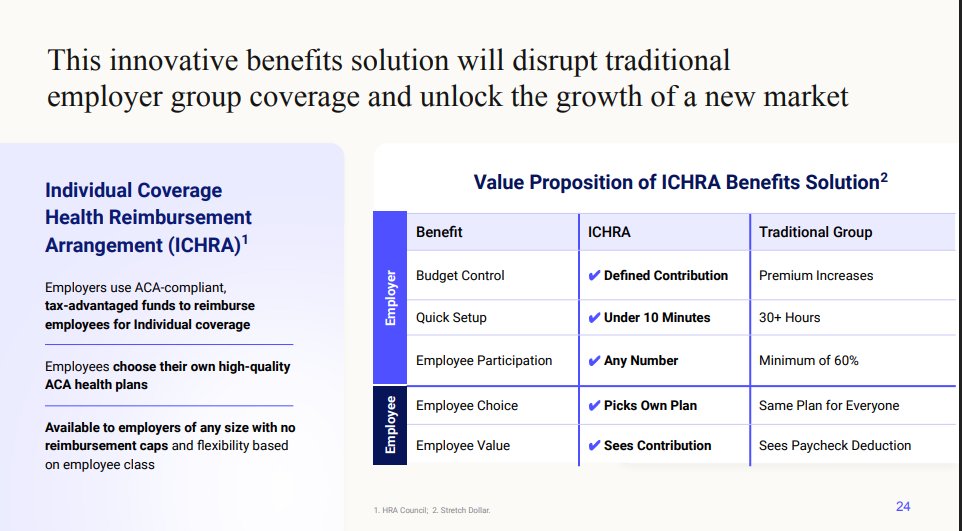

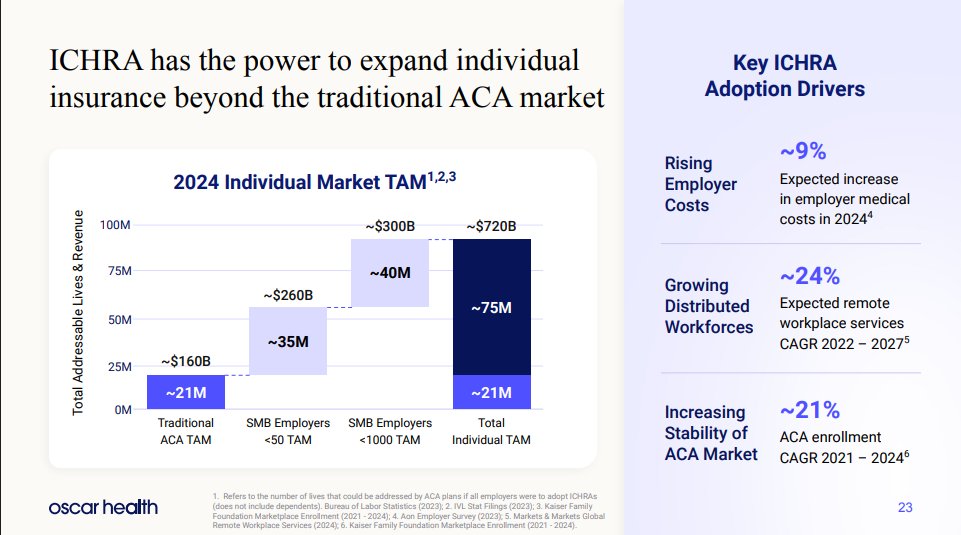

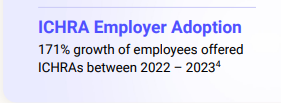

$OSCR - This will be a $100B company. We are witnessing the next $PLTR and $HOOD right before our eyes. Oscar's TAM could very like 3-4x over the next two years with the ICHRA push. There was a 171% growth of employees offered ICHRAs between 2022-2023. Just wait until it goes mainstream. It's better for the employer & the employee - it's a no brainer better wait to do healthcare. Now, legislation is very slow moving and these things take time but the path we are going on is clear. With 20% of US GDP spent on healthcare and a clear problem with Debt/GDP a solution isn't just ideal it's essential for the solvency of US debt.

Lets break a few key things down:

ICHRA = the payment mechanism (employer allowance)

ACA = the actual insurance marketplace providing the plans

Employees use the ICHRA funds to go shop for ACA marketplace plans.

Old model (traditional group insurance):

Employer → Buys group plan → Employees stuck with that plan.

New model

Employer → Gives $$ to employee → Employee → Buys an ACA individual plan

So the employee ends up in the ACA market, which is Oscar’s stronghold.

If ICHRA adoption grows, millions of employees move off group plans into ACA plans, increasing: ACA enrollment, Quality risk pools, Oscar’s revenue + margins.

Oscar tends to be: Price-competitive, Lower premium than legacy carriers, Attractive UI + member support, & Solid provider access.

----------------------------------------------------

In the ACA market, Risk Adjustment (RA) = the difference between making money or losing money.

Oscar’s entire stack is engineered around RA:

-predicting risk

-identifying missing codes

-guiding care

-stratifying members

-closing gaps automatically

When the massive shift happens when employers get off of group plans (Think Pensions to 401ks) - Anthem, United, Cigna, & Others will need to compete. (They will be nowhere near as successful). Oscar is a Tesla and the rest of the market is a 95 Honda Civic.

If RA becomes increasingly tech-driven (it is), Oscar has a long-term moat.

Other insurers will NEED Oscar's tech stack - but they won't build it. Why? Building a new core system = multi billion dollar death march. You can't just buy "Oscar's stack" - Oscar build in house. This is why +Oscar is a major future revenue stream that could turn this into an AI Healthcare Software Company. They can sell claims automation, risk adjustment engines, member engagement tools, care navigation models. Essentially becoming the shopify of insurance ops.

bUt whAt aBouT the sUbSidies???

Thanks for listening.

$HIMS is a marketing company with no moat

$DUOL too

$IREN execs might be the dumbest I've seen

$CRWV is risking it all

$META is cheap

$ORCL will be again soon

$UBER the top is in

$ADBE don't buy a falling knife

$SOFI just wait

$PYPL lol

I believe…

… $JD is in the early days where $AMZN was in 2022

… $GOOGL will win the AI race — if there ever was a real race

… in probably one month, $HIMS will be a generational buy

… $XPEV is in the early days where $TSLA was in 2022

… $XYZ is one of the most underrated stocks

… $PLTR is in the early days where $AMD was in late 2021

… $IONQ is a generational buy

… $UNH will fall below $300 before pumping

… $PYPL will fall below $50 — but is also a generational buy

Your thoughts? 👇

Current situation:

1. The US is preparing $2,000 stimulus checks

2. Japan is preparing a $110 billion stimulus package

3. China has approved a $1.4 trillion stimulus package

4. The Fed is officially ending QT on December 1st

5. The US is issuing~$1.9 trillion in treasures per year

6. Canada is restarting its Quantitative Easing program

7. Global M2 money supply is at a record $137 trillion

8. Global rate cuts are at 320+ over the last 24 months

In what world is another wave of inflation not on its way?

JAPAN JUST KILLED THE GLOBAL MONEY PRINTER AND NOBODY NOTICED

The most dangerous number in finance right now is 1.71%.

That’s Japan’s 10-year bond yield. Highest since 2008. Here’s why your retirement just got obliterated:

For 30 years, Japan printed infinity money at 0% rates and exported it worldwide. $3.4 trillion flowed into US Treasuries, European debt, emerging markets. This invisible bid kept YOUR mortgage cheap, YOUR stocks inflated, YOUR government solvent.

November 10th, 2025: The bid disappeared.

Japan’s yield hit 1.71%. They’re pumping $110 billion stimulus into their economy while debt sits at 263% of GDP. The math just became impossible. At 1.7% rates, Japan pays $27 billion MORE in interest. Every. Single. Year.

Here’s the extinction event nobody sees coming:

Japanese pension funds are pulling $1.1 trillion OUT of US Treasuries right now because keeping money in America LOSES them money after hedging costs. The largest foreign buyer of American debt is becoming a seller.

When Japan stops buying, interest rates don’t stay flat. They explode. US 10-year yields will jump 40 basis points minimum from flow dynamics alone. Your 7% mortgage becomes 8%. Corporate debt refinancing costs spike 60%. Zombie companies holding $3 trillion in junk bonds start defaulting in waves.

The yen carry trade just reversed. $1.2 trillion in borrowed yen funding crypto, stocks, emerging markets must unwind. Every hedge fund, every momentum trade, every leveraged bet built on free Japanese money is getting margin called simultaneously.

This breaks in three places:

Stock valuations were built for 2% bond yields forever. At 3.5% yields, the S&P 500 fair value drops 35%. Emerging market currencies collapse without Japanese capital inflows. Europe’s debt crisis returns because Italy and Spain lose their silent buyer.

December 18th the Bank of Japan meets. 50% chance they hike again. If they do, sell everything not nailed down.

Your 401k doesn’t price this in yet. The Fed can’t stop this. No central bank can.

The world’s biggest piggy bank just cracked open and the money is flowing backwards.

Position accordingly or get destroyed.

Full article here - https://t.co/NAuONH2jlj