On GGDC – Some Thoughts from the Founder

Many people ask me, what exactly is GGDC trying to achieve?

Every time I answer that, it feels like telling a very long story. And that story doesn't begin with a whitepaper or a mint price. It begins with a single thought:

Can we find a completely new way for people around the world to take part in climate action together?

This is not a short-term project. We are a group of long-termists.

The Asymmetric Climate Perpetual Bond

Almost every climate finance product out there has a benchmark, a template, a path laid out by those who came before. But GGDC's "asymmetric climate perpetual bond" has none of that.

It is something entirely new.

And precisely because there's no benchmark, it is incredibly difficult to explain. You have to walk someone through: why these NFTs are not about speculation, why distribution is not about returns, why governance is not an empty promise, and why the funds go not into anyone's pocket but into real climate assets.

Every sentence has to be repeated. Every person takes time to understand.

The cost of education is high. The cycle of education is long.

We've only just begun.

One or Two Years, or a Lifetime?

I've said on social media before: the GGDC Founder NFT project we are now launching looks like a one-to-two-year plan in the short term. But anyone who knows us well understands that behind this lies a lifelong mission spanning decades, even a century.

Climate problems are never solved overnight. The restoration of the Aral Sea takes twenty years. Protecting the Congo rainforest requires two generations. Growing a carbon sink forest takes half a century.

If we only wanted to do a short-term project, we would never touch these hardest, heaviest, least sexy things.

It's precisely because we want to do this for a lifetime that we choose the most difficult road.

For the World, One Step at a Time

Through global social media, online communities, and digital ecosystem platforms, we are promoting GGDC across the world. There are no shortcuts – just talking to people one by one, engaging communities one by one.

We hope that in Africa, Southeast Asia, Latin America, Europe, North America – people from all walks of life will care about the climate and about this financial tool that can help the planet.

Maybe only dozens of people will join today. Maybe only dozens tomorrow. That's fine.

Long-termism is not a slogan. It's a daily commitment.

Finally

If you ask me: can GGDC succeed?

I don't know what "succeed" means. If success means pumping the price tomorrow, listing on an exchange the day after, and getting rich next week – sorry, we can't do that.

But if by success you mean –

That ten years from now, a certain carbon sink forest is thriving because of everyone's support back then;

That twenty years from now, a place once plagued by drought and salt dust sees green again;

That fifty years from now, someone looks back and says, "So there were people already working on this back then" –

Then I think we are already on our way.

Slowly, but faster than you think.

— Don Waugh

Written at 5 AM, May 2, 2025

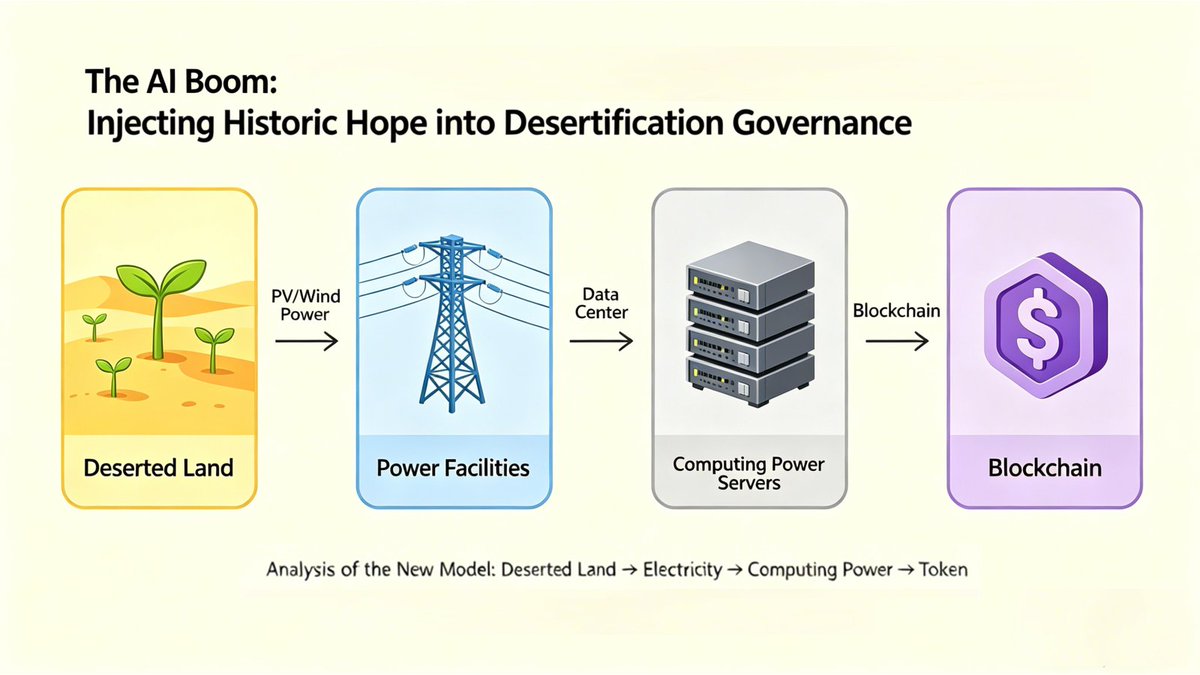

The AI Boom Injects Historic Hope into Desertification Control

Today, thanks to the explosion of AI, we have found the key to treating desertification on a large scale: the value chain of "Degraded land → Electricity → Computing power → Token."

Degraded Land Restoration: A Conversion Path to Strategic Energy Assets | United Carbon Sink Fund

Under the triple pressures of intensifying global desertification, energy security crises, and the explosive growth in demand for artificial intelligence computing power, a new paradigm is emerging: transforming degraded land that is losing its ecological functions into renewable, strategic energy assets through the combination of high‑efficiency energy plant cultivation and biomass energy technology. This is not merely an ecological compensation measure, but a comprehensive pathway that simultaneously addresses land degradation, energy shortages, and economic development challenges. Taking the sub‑Saharan Sahel region as an example, this paper explores how degraded land restoration can achieve a value jump from "ecological burden" to "energy asset."

I. Degraded Land: A Vast, Underestimated Silent Asset

Approximately 2 billion hectares of land worldwide are affected by varying degrees of degradation caused by human activities or climate change, with Africa being the hardest hit. The Sahel region—the semi‑arid transitional zone along the southern edge of the Sahara Desert—suffers particularly severe land degradation. In Nigeria, about 70% of arable land is threatened by the southward advance of the Sahara, with over 100,000 hectares of arable land lost annually. On these lands, soil organic matter has been lost, vegetation cover has sharply declined, wind and water erosion alternate, agricultural production has nearly stagnated, and local communities are trapped in a cycle of poverty and ecological deterioration.

However, when re‑examined from an asset conversion perspective, these degraded lands actually possess unique "energy endowments": abundant sunlight, flat terrain, relatively concentrated land rights, and distance from high‑value agricultural zones. Their "low opportunity cost" makes them highly suitable for large‑scale energy plant cultivation—they do not compete with food cropland, do not trigger land conflicts, and, through revegetation, actually achieve ecological restoration and climate goals. In other words, these lands are not worthless; rather, the form in which their value is realized requires an entirely new conversion tool.

II. Energy Plants: Bridging Ecological Restoration and Energy Production

Traditional degraded land restoration relies mainly on ecological measures such as planting trees and shrubs or closing hillsides for afforestation, which are slow to show results and have long economic payback periods, making it difficult to attract private capital. The emergence of high‑efficiency energy plants has changed this situation. C4 plants such as super giant reed (Arundo donax) and giant juncao grass (Pennisetum giganteum) grow rapidly, produce large biomass, tolerate drought and poor soils, and can be harvested annually for many years. On degraded land, they can achieve a dry‑basis yield of 3–5 tons per hectare per year. Taking super giant reed as an example, its calorific value can reach 4,500 kcal/kg, with a cellulose content of 57.71%. At the same time, it provides ecological functions such as carbon sequestration, soil improvement, and erosion control.

The core value of such plants lies in the following: during growth, they absorb carbon dioxide, stabilize the soil, and restore organic matter, thereby achieving ecological restoration; after harvest, the biomass can be used as fuel for power generation, gas production, or alcohol conversion, realizing energy transformation; the residual ash can be made into biochar and returned to the soil, forming a closed‑loop carbon sequestration system. This means that for every hectare planted with energy plants, one simultaneously obtains an ecological restoration insurance policy and a miniature energy mine. It is precisely this dual‑output nature of "ecology + energy" that transforms degraded land from a purely input‑intensive restoration target into a productive energy asset.

III. From Biomass to Electricity and Computing Power: Three‑Stage Value Leap

Converting biomass into strategic energy assets requires three stages of value leap:

First stage: Biomass feedstock as an asset. Through large‑scale cultivation, degraded land yields a continuous, predictable stream of biomass feedstock. Based on an estimate of 100,000 hectares of cultivation, annual dry‑basis output can reach 4.5–6 million tons, sufficient to support a biomass supply chain of hundreds of thousands of tons. This is a physical form of energy reserve that can be stored long‑term and is not affected by seasonal or weather fluctuations.

Second stage: Biomass power as an asset. Distributed or centralized biomass power plants convert the feedstock into uninterrupted green electricity. Unlike photovoltaic and wind power, biomass power can achieve continuous, stable output 24 hours a day, with annual operating hours exceeding 7,000 hours and a capacity factor of 70%–90%. For the grid, this is dispatchable, predictable baseload power that can effectively replace coal‑fired generation. For regions with weak grid infrastructure, such as parts of Africa, biomass power plants can also operate as independent micro‑grid power sources, running off‑grid to directly supply industrial facilities and communities.

Third stage: Computing power as an asset. This is the highest level of value conversion. A portion of the electricity generated by the biomass power plant is directly supplied to a co‑located computing center (data center), and the computing power is sold externally using a designated digital currency (e.g., GGDC). In the context of a global AI computing power shortage, green, stable, low‑cost computing power is itself a hard currency. Through the "electricity‑computing‑coin" closed loop, the value of biomass electricity is no longer limited to the feed‑in tariff, but is magnified several‑fold to tens‑fold through the premium of the computing power market. Under this model, a 1.5 GW biomass power cluster supported by 100,000 hectares of degraded land can drive a computing center with total capacity exceeding 500 MW, outputting tens of thousands of AI training hours, with annual output value far exceeding that of traditional agriculture or a simple power sales model.

IV. The Nigerian Sahel Case: From Desert to Energy Asset in Practice

The Sahel belt in northern Nigeria covers 11 frontline "Great Green Wall" states and includes over 1 million hectares of degraded land awaiting restoration. The country also faces a severe electricity shortage (45% of the population lacks access to power) and rapidly growing computing power demand. In this context, a demonstration project for 100,000 hectares of high‑efficiency energy plant cultivation is under way. The first phase plans 10,000 hectares supporting a 150 MW biomass power plant, of which 100 MW will be directly supplied to a computing center and 50 MW sold to the grid. When fully built out to 100,000 hectares, the project will form a 1.5 GW power generation cluster.

The project restores degraded land by planting super giant reed and giant juncao grass, while simultaneously building a digital management platform and a GGDC payment system. Total investment is estimated at approximately US$4 billion. It is expected to create 50,000 jobs, generate 10.5 billion kWh of electricity annually, and deliver computing power on the order of several exaFLOPS. More importantly, the project's carbon reduction capacity (displacing fossil fuel combustion + biochar soil carbon sequestration) will achieve negative carbon emissions. This ecological value is tokenized through GGDC, enabling global individuals and institutions to engage in voluntary emissions reductions and fulfill their voluntary carbon reduction commitments.

This case demonstrates that degraded land is not an irreversible ecological burden. By selecting appropriate energy plants, matching them with advanced power generation and computing infrastructure, and innovatively introducing a digital currency as a value medium, degraded land can be transformed into a highly liquid, appreciable strategic energy asset.

V. Policy and Financial Innovation: Supporting the Asset Conversion

For the conversion from degraded land to energy assets to be realized, the technical level is already feasible, but institutional and financial breakthroughs are still needed. First, land tenure and the duration of use rights are fundamental prerequisites. Energy plants require 15–20 years of continuous operation to generate stable returns; host countries need to provide land lease or concession rights of no less than 30 years, along with a stable policy environment. Second, biomass feed‑in tariffs (PPAs) and permits for direct electricity supply must be clearly stipulated; otherwise, the electricity‑computing‑coin closed loop cannot be implemented. Third, for models relying on crypto‑assets, host countries need to establish a clear regulatory framework for virtual assets and issue VASP licenses to project entities.

Innovations in financial instruments are equally critical. Traditional climate funds (such as the Green Climate Fund or World Bank) can provide long‑term concessional loans. Carbon credit issuance (e.g., CCC NFTs) can monetize future carbon reduction benefits in advance. Climate perpetual bonds can issue GGDC based on the project’s future cash flows to raise funds on crypto markets. These three layers of financial structure together address the maturity mismatch between large upfront investment and long‑term returns.

VI. Prospects and Challenges

Elevating degraded land restoration projects into the construction of strategic energy assets has the potential to reshape the development logic of the Sahel region and even arid and semi‑arid areas worldwide. It no longer treats ecological restoration as a drain on fiscal expenditure, but as a new industry capable of generating positive cash flow. With the exponential growth in global demand for AI computing power, stable green electricity becomes increasingly valuable, and integrated solutions that simultaneously provide electricity, computing power, ecological restoration, and jobs will see their strategic importance further magnified. At the Cambridge Energy Week conference in 2026, a highly significant message emerged: the explosion of AI has triggered unprecedented "energy anxiety." AI data centers are extremely hungry for electricity, and some large technology companies, in order to solve the power shortage, have even begun investing directly in small modular nuclear reactors and nuclear fusion technology. The relationship between technology and energy is being reshaped.

However, challenges remain: large‑scale cultivation of energy plants must overcome constraints of water and soil resources; the fuel supply chain management for biomass power is highly complex; volatility in digital currencies may affect project cash flow stability; host country policy risks need to be mitigated through multilateral guarantees and stability clauses. Yet clear technical, management, and financial responses exist for each of these issues..

Conclusion

Degraded land is not nature's punishment of humanity, but a treasure chest for which we have not yet found the right key. Through the three‑stage conversion of high‑efficiency energy plant cultivation, biomass power generation, and computing power output, these seemingly wasted lands can gain a new lease on life—they will deliver stable electricity, scarce computing power, and tradable carbon assets, while restoring ecological functions, creating jobs, and reducing poverty. The ongoing practice in Nigeria’s Sahel region is proving that investment in restoring degraded land need not be a cost center; it can be a strategic gateway to future energy sovereignty and digital sovereignty. This is a pathway worthy of attention and adoption by all countries threatened by desertification around the world.

(The author is a researcher at the United Carbon Sink Fund)

Climate Perpetual Bond – The "Unique Expertise" of Climate Public Company (Part 7)

The Climate Perpetual Bond and the Climate Public Company form a perfect closed loop. The former provides a continuous stream of long-term capital support to the latter, while the latter uses this capital to develop and produce carbon assets with both economic value and emission reduction capabilities, achieving the dual goals of returns and climate commitments. When global bubbles burst and the drawbacks of Modern Monetary Theory become apparent, GGDC—backed by real climate projects—will gain substantial credibility. This is not just financial innovation; it is an institutional revolution that brings strategic ecological assets onto corporate balance sheets.

The Climate Perpetual Bond is the "unique expertise" of the Climate Public Company in supporting the UN's 2050 net-zero emissions goal and achieving global climate control targets by the end of this century.

Climate Perpetual Bond – The "Unique Expertise" of Climate Public Company (Part 6)

As of 2025, the total global debt has reached $348 trillion, with over 80% coming from advanced economies and a debt-to-GDP ratio of 333%. The ability of sovereign governments to increase public sector investment to regulate the economy has hit its limit. The climate perpetual bond system, however, takes a different path. By adopting a cryptocurrency-denominated approach, it overcomes the drawbacks of traditional fiat debt—such as geopolitical maneuvering, bureaucracy, complexity, and high risk—while promoting the "socialization of assets, perpetualization of debt, and sustained returns" in the public sector. It transforms perpetual bonds from instruments serving only the financial industry into a mechanism that, through its unique asymmetric structure and the model of issuing currency as financing (integrating bond and currency), flows on a large scale into public sectors such as climate and environmental governance, healthcare, and education.

Climate Perpetual Bond – The "Unique Expertise" of Climate Public Company (Part 5)

The issuance system of GGDC was approved and registered by the government of the U.S. state of Colorado in 2020. The system consists of four organizations: the Global Climate Cryptocurrency Action Committee (GCCC), which advocates for climate ideology and is headquartered in Washington, D.C., USA; the United Carbon Sink Fund (UCSF), which identifies qualified climate projects and is headquartered in Ethiopia; the United Bank of Kinetics (UBK), which issues GGDC and is headquartered in New York, USA; and the Green Digital Currency Alliance (GGDA), responsible for operational supervision and headquartered in Singapore. These four organizations operate independently, working together to advance the construction of global narrow climate finance infrastructure and promote global climate development.

Climate Perpetual Bond – The "Unique Expertise" of Climate Public Company (Part 4)

The green digital currency GGDC is not an ordinary cryptocurrency; it features a triple value-enhancing flywheel.

The first flywheel: Interest paid by climate projects is injected into smart contracts to repurchase and burn GGDC.

The second flywheel: 15% of project profits are also injected into smart contracts, accelerating the repurchase and burning of GGDC.

The third flywheel: Upon project maturity, the redemption of Climate Perpetual Bonds creates a phase of strong deflationary pressure.

As the circulating supply of GGDC continues to decrease while project output keeps growing, the price index of GGDC relative to sovereign currencies rises steadily over the long term. This is an unprecedented, self-reinforcing system of stable value appreciation.

Climate Perpetual Bond – The “Unique Expertise” of Climate Public Company (3)

The asymmetric structure of the Climate Perpetual Bond is ingeniously designed. There is no concept of creditors in the system; instead, investors exchange and hold a counter-cyclical crypto asset, GGDC. The interest paid by debtors, along with the 15% of returns reserved for the “climate,” are all injected into smart contracts and used to buy back and burn GGDC in the open market, creating a powerful built-in deflation mechanism. The interest rate design of the Climate Perpetual Bond is as follows: 2.90% for the first five years, rising to 3.50% from the fifth year onward, with no further increases after 20 years (capping at 4.86%). The 30-year annualized average interest rate does not exceed 4.0%. After 30 years, the obligation to pay interest is eliminated, leaving only the 15% profit distribution right. According to international financial standards, the Climate Perpetual Bond will add long-term capital, not debt, to the balance sheet of the Climate Public Company.

Climate Perpetual Bond—The "Unique Specialty" of Climate-Public Companies (2)

What are Climate Perpetual Bonds? They are not traditional bonds and do not require regulatory approval. Climate Perpetual Bonds are established by climate-public companies (climate projects) and represent a debt commitment with no fixed maturity, denominated in the green digital currency, GGDC. The United Reserve Bank (UBK) issues GGDC to purchase this debt commitment, and climate projects utilize GGDC to promote the construction and development of public sectors such as desertification control, renewable energy, adaptive agriculture, and healthcare and education. In essence, Climate Perpetual Bonds are innovative financing tools tailored for the global public sector.

Climate Perpetual bonds—The Unique Advantage of Climate-Public Companies (1)

Perpetual bonds are not a new invention. In 1648, Dutch water management authorities issued the world’s first perpetual bond, dating back more than 370 years. By 2023, the global perpetual bond market had reached $647.1 billion, with banks and non-bank financial institutions accounting for 88% of the total. However, this financial instrument, which originated in the public sector of urban water supply, has been "occupied by the dove in the magpie's nest" for centuries, rarely being used for public sectors such as climate and environment, education, and healthcare. The emergence of climate perpetual bonds aims to correct this historical deviation and return perpetual bonds to their original purpose of serving public welfare.

#Climate# Perpetual# bonds#

@UNEP This message deserves a wider audience. Degradation → vulnerability → disasters — this chain is worth a pause for everyone who cares about the future. Protecting ecosystems means protecting ourselves.