S&P held Indonesia at BBB stable. Worth saying clearly: that's the one agency of three that did NOT go to negative, after Moody's and Fitch both did. Relative win.

S&P named Indonesia the most vulnerable ASEAN economy if regional conflict persists. The mechanism is energy: rising subsidy spending and a deficit widening on higher oil imports. Two of their three key risks are oil.

This inverts the old thesis. For years the line was "commodity exporter, high energy prices are net positive." Not for oil anymore. Crude exports gone, fuel imports surging, so expensive oil now inflates the subsidy bill and widens the import gap. World Bank already cut 2026 growth to 4.78% on exactly this.

The nuance S&P keeps is that Indonesia can still partially offset. Coal, LNG, CPO revenue is a real hedge. But it's now a partial hedge against a vulnerability it used to fully cover. Oil is the leak. The other commodities are the pump. Net depends on which moves faster.

After the quarter we just had, we'll take it. Breathe a little.

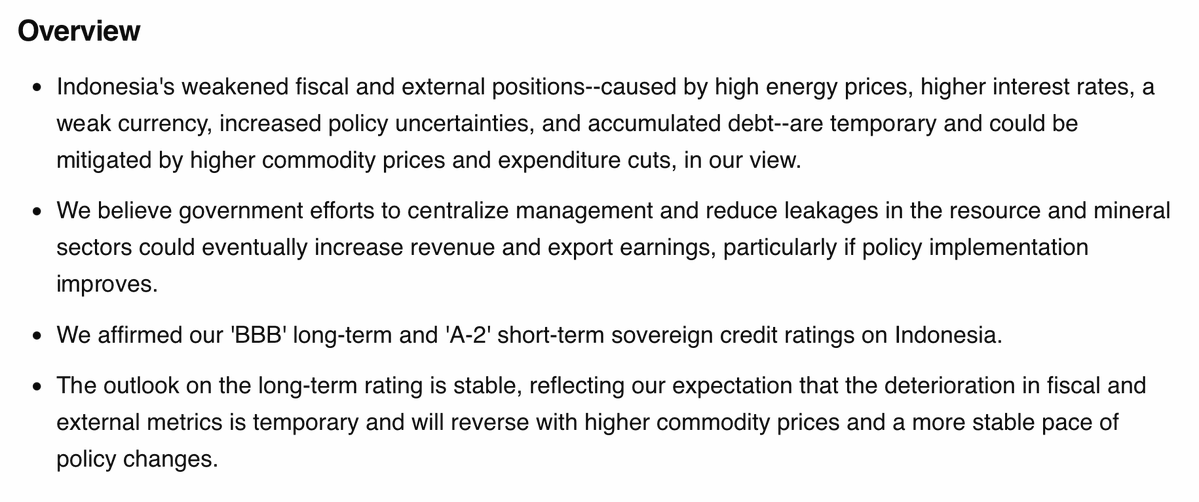

Bloomberg: S&P Pertahankan Rating Indonesia

- Lembaga sovereign credit rating, S&P, mempertahankan rating Indonesia pada level 'BBB/A-2'

- Outlook juga dipertahankan pada level 'Stable'

[Sumber: Bloomberg]

![Stockbit's tweet photo. Bloomberg: S&P Pertahankan Rating Indonesia

- Lembaga sovereign credit rating, S&P, mempertahankan rating Indonesia pada level 'BBB/A-2'

- Outlook juga dipertahankan pada level 'Stable'

[Sumber: Bloomberg] https://t.co/xmPP2etD6S](https://pbs.twimg.com/media/HNGJR9UagAIjF7R.jpg)